Models II: Univariate Regression with statsmodels#

Learning Goals#

In the previous notebook we calculated a GLM by-hand by implementing the OLS solution using numpy.

In this notebook we’re going to meet statsmodels a new Python library that allows us to much more easily estimate, evaluate, and compare models to each other.

We won’t be covering the full functionality of statsmodels as it’s vast and beyond the scope of this course.

Instead we’ll be focusing on estimating regression models using OLS in statsmodels which behaves very similarily to lm()in R.

Estimating a univariate regression using OLS with

statsmodelsEvaluating and inspecting model assumptions and predictions

Testing simple hypotheses using model comparison

Interpeting estimated model parameters

Understanding parameter inference

Slides for reference#

Modeling Data I (slides)

Modeling Data II (slides)

Modeling Data II 1/2 (slides)

Univariate Regression#

Let’s learn how to fit a univariate regression model using statsmodels.

We’ll be using a dataset of credit-card scores that contains observations from 400 different people with the following columns:

Variable |

Description |

|---|---|

Income |

in thousand dollars |

Limit |

credit limit |

Rating |

credit rating |

Cads |

number of credit cards |

Age |

in years |

Education |

years of education |

Gender |

male or female |

Student |

student or not |

Married |

married or not |

Ethnicity |

African American, Asian, Caucasian |

Balance |

average credit card debt |

import numpy as np

import polars as pl

from polars import col

import seaborn as sns

import matplotlib.pyplot as plt

df = pl.read_csv('./data/credit.csv')

df

| Index | Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance |

|---|---|---|---|---|---|---|---|---|---|---|---|

| i64 | f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 |

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | "Male" | "No" | "Yes" | "Caucasian" | 333 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | "Female" | "Yes" | "Yes" | "Asian" | 903 |

| 3 | 104.593 | 7075 | 514 | 4 | 71 | 11 | "Male" | "No" | "No" | "Asian" | 580 |

| 4 | 148.924 | 9504 | 681 | 3 | 36 | 11 | "Female" | "No" | "No" | "Asian" | 964 |

| 5 | 55.882 | 4897 | 357 | 2 | 68 | 16 | "Male" | "No" | "Yes" | "Caucasian" | 331 |

| … | … | … | … | … | … | … | … | … | … | … | … |

| 396 | 12.096 | 4100 | 307 | 3 | 32 | 13 | "Male" | "No" | "Yes" | "Caucasian" | 560 |

| 397 | 13.364 | 3838 | 296 | 5 | 65 | 17 | "Male" | "No" | "No" | "African American" | 480 |

| 398 | 57.872 | 4171 | 321 | 5 | 67 | 12 | "Female" | "No" | "Yes" | "Caucasian" | 138 |

| 399 | 37.728 | 2525 | 192 | 1 | 44 | 13 | "Male" | "No" | "Yes" | "Caucasian" | 0 |

| 400 | 18.701 | 5524 | 415 | 5 | 64 | 7 | "Female" | "No" | "No" | "Asian" | 966 |

The primary question we’re interested in answering is:

Is there a relationship between Income (how much a person makes) and their Balance (average credit card debt)?

Remember univariate regression is just a “flavor” of the GLM where we only have a single predictor variable \(X\) being used to model an outcome variable \(y\).

Let’s get started!

0. Data Exploration#

Before you build any model you should always plot your data first. This will give you better idea of what your data looks like any any modeling choices you might make.

Let’s use seaborn to plot our data:

import seaborn as sns

import matplotlib.pyplot as plt # for customization

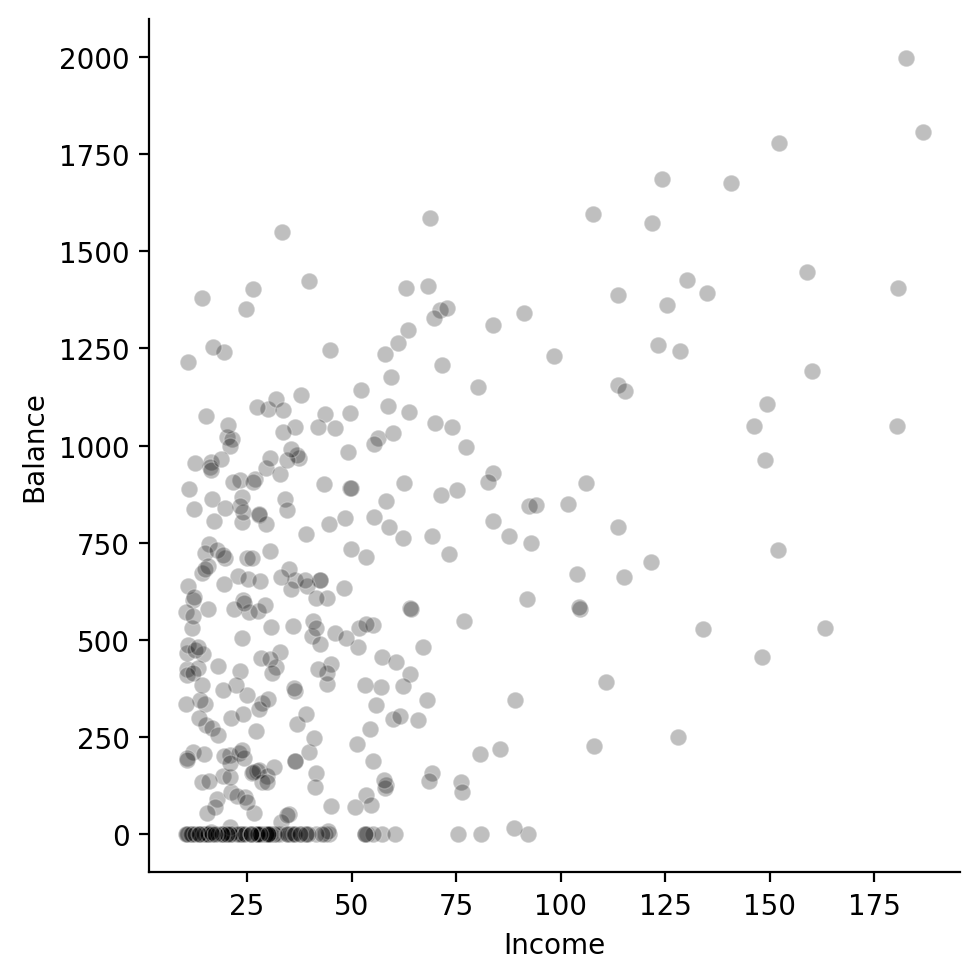

sns.relplot(

data=df,

x='Income',

y='Balance',

color='black',

alpha=.25,

)

<seaborn.axisgrid.FacetGrid at 0x123c31950>

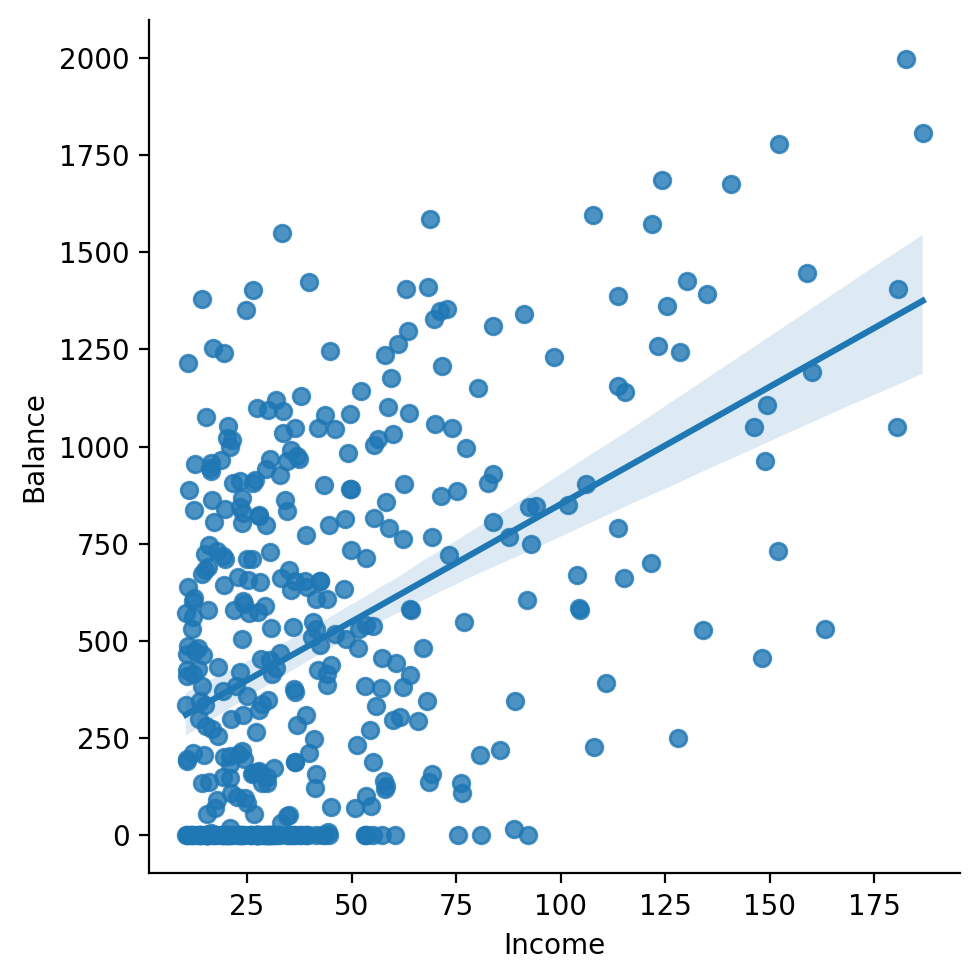

We can see there does seem to be some kind of relationship: as income increases so does balance.

There’s also some interesting observations at the lower end of income let’s zoom into those.

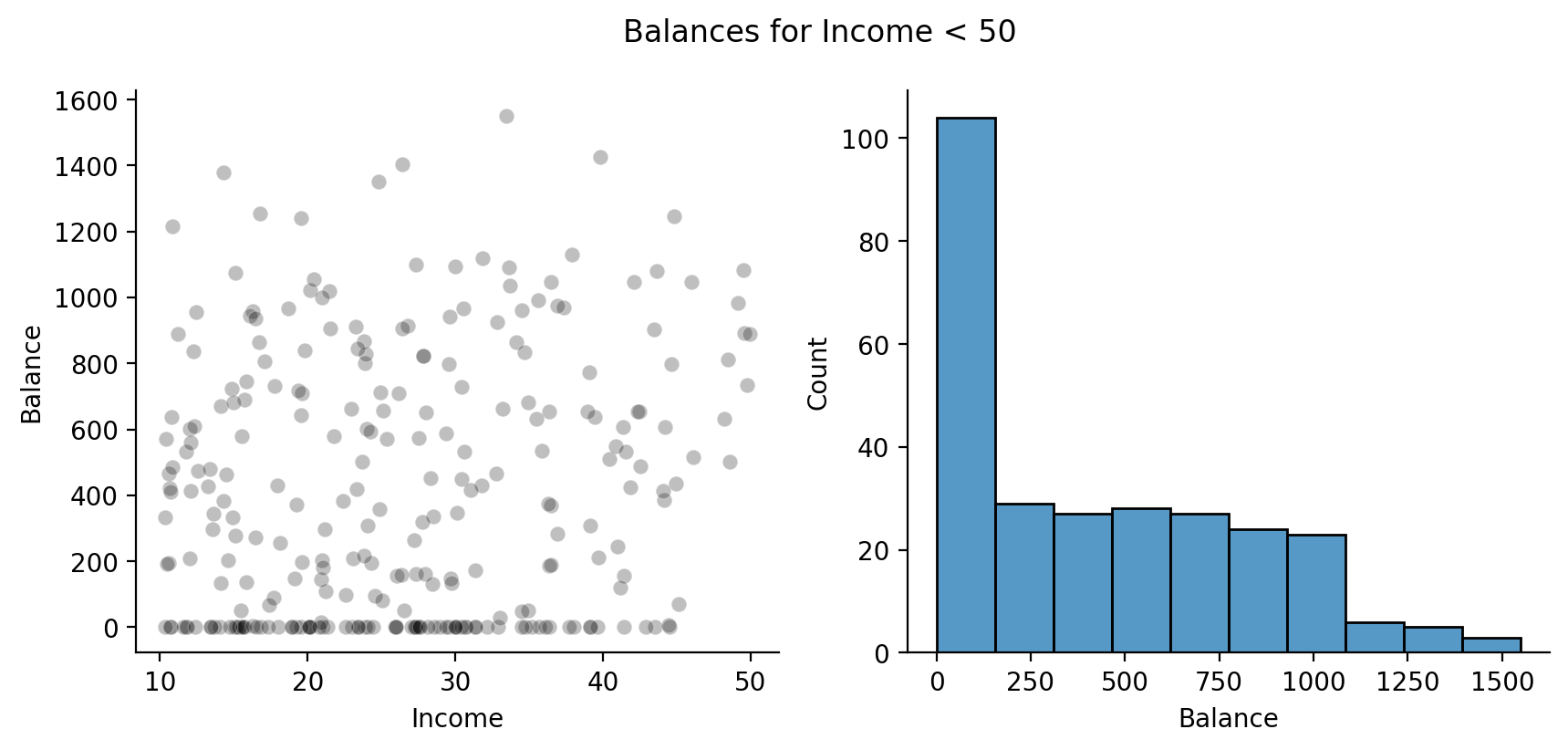

I’ll first filter the data to Incomes < 50 and then create another scatter plot + a histogram

# Filter rows and only select 3 columns

df_lt_50 = df.filter(col('Income') < 50).select(['Index', 'Income','Balance'])

# Create 1 x 2 figure

f, axs = plt.subplots(1,2, figsize=(10,4))

# Left

sns.scatterplot(

data=df_lt_50,

x='Income',

y='Balance',

color='black',

alpha =.25,

ax=axs[0]

)

# Right

sns.histplot(df_lt_50, x='Balance', ax=axs[1]);

# Remove top and right spines

sns.despine();

# Add overall title

f.suptitle('Balances for Income < 50');

Ah, we can see that for a large number of people with Incomes below this threshold they carry a Balance of $0!

Let’s keep this mind as we fit our model and interpret the results.

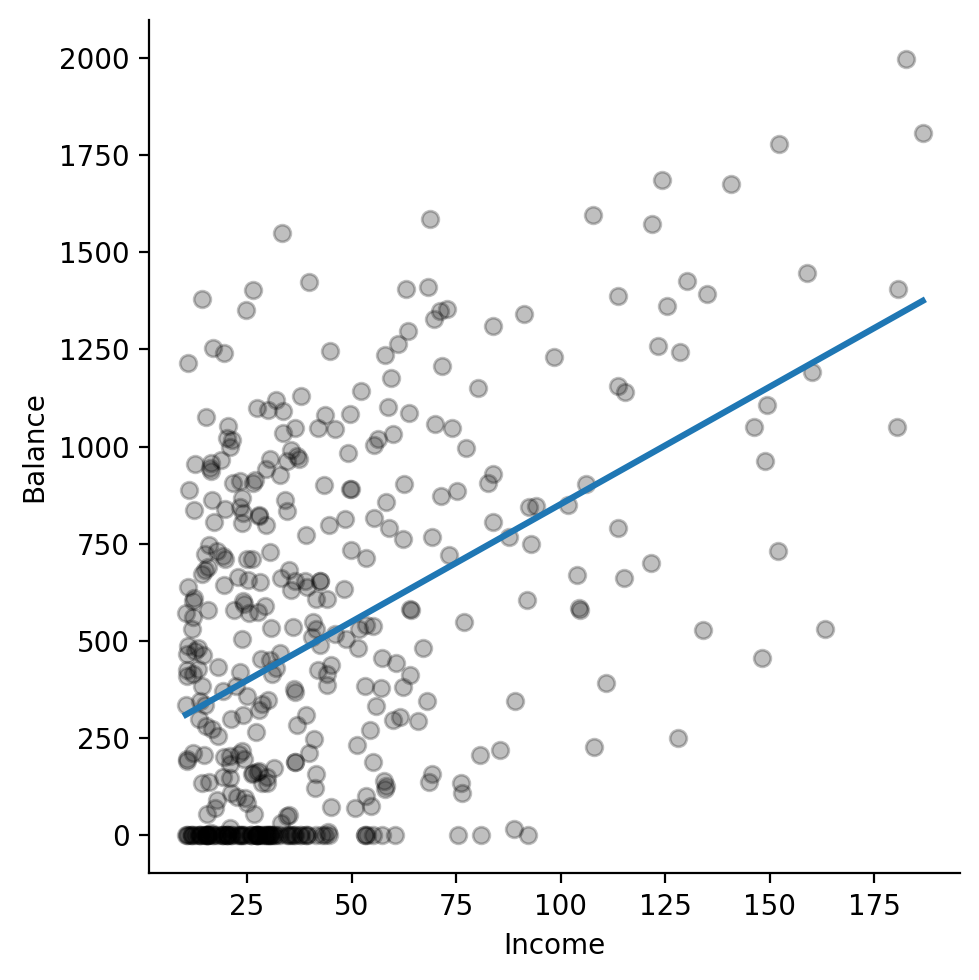

Next let’s ask seaborn to add in a regression line using the original data.

This gives us an indication of how well our model will do before we use statsmodels.

In fact, seaborn uses statsmodels under-the-hood to do regression!

sns.lmplot(

data=df, # original data

x='Income',

y='Balance',

fit_reg=True,

ci=None, # no confidence intervals

scatter_kws={'color':'black', 'alpha':.25}, # match color scatterplots

)

<seaborn.axisgrid.FacetGrid at 0x147d2fad0>

Ok this is promising and verifies out visual intuitions about an increasing linear relationship. Let’s go ahead and estimate a model ourselves!

1. Model estimation#

We can start by importing the ols function from statsmodels:

from statsmodels.formula.api import ols

This function takes 2 arguments:

formula: a Python string that specifies the model using formula-syntax similar to R’slm()functiondata: a Pandas DataFrame that contains the data; we can convert ourpolarsDataFrame to a Pandas DataFrame using.to_pandas()

A note on using model “formulas”#

Wilkinson Notation, i.e. “formula syntax” was popularized by R and provides a succinct way to specify models.

statsmodels supports mostly the same syntax but there are a few differences you should be aware of in-case you’re trying to translate things 1-to-1

We’ll try to add any formula quirks to the course-website, but for now this reference should get you going:

Formula |

Description |

|---|---|

|

intercept only |

|

intercept and x1 |

|

only x1 without intercept |

|

intercept and log-transformed x1 |

|

intercept and mean-centered x1 |

|

intercept and z-scored x1 |

|

intercept, x1, and x2 |

|

intercept, x1, x2, and their interaction |

|

short-hand for previous |

|

intercept, x1, and x2 squared |

Let’s use this syntax to define our model. statsmodels works best with Pandas dataframes so make to call .to_pandas() on your dataframe before passing it to ols:

model = ols('Balance ~ Income', data=df.to_pandas())

Remember that whenever we use formula syntax, both R and Python will automatically add an intercept term for us. In other words, the following formulas are equivalent:

Balance ~ 1 + IncomeBalance ~ Income

Key model attributes#

The model variable we created is a statsmodels OLS model that has 2 key attributes you’ll want to know how to access:

model.exog: the \(X\) design matrix of the modelmodel.endog: the \(y\) vector of observations of the dependent variable

Note statsmodels was developed in an econometrics tradition where \(X\) is referred to as the “exogenous” variable and \(y\) is referred to as the “endogenous” variable.

We can see that our design matrix contains a column for the intercept \(\beta_0\) and column for our single predictor \(\beta_1\) Income:

# First 3 rows of design matrix

model.exog[:3, :]

array([[ 1. , 14.891],

[ 1. , 106.025],

[ 1. , 104.593]])

And that our \(y\) vector is just the column of our dependent variable values

# Numpy function to compare two arrays each element at a time

np.allclose(

model.endog,

df['Balance'].to_numpy()

)

True

Fitting the model#

To actually estimate our model, we can use its .fit() method and save the output to a new variable

results = model.fit()

results

<statsmodels.regression.linear_model.RegressionResultsWrapper at 0x147dc1bd0>

Key Estimation Attributes#

The output of .fit() is a RegressionResults object that has lots of methods and attributes referenced in the linked documentation.

For now let’s just focus on a few of you’re most likely to use:

results.params: the estimated \(\hat{\beta}\) coefficientsresults.fittedvalues: the predicted values \(\hat{y}_i\)results.resid: the residuals \(y_i - \hat{y}_i\)results.ssr: the sum of the squared residuals \(\sum_{i=1}^n (y_i - \hat{y}_i)^2\)

Let’s look at the parameter estimates

# Betas - estimated coefficients

results.params

Intercept 246.514751

Income 6.048363

dtype: float64

We can get each one by name by slicing

results.params['Intercept']

np.float64(246.51475059140336)

results.params['Income']

np.float64(6.048363408531563)

And the model’s predictions of our dependent variable (\(\hat{y}\)), in this case \(\hat{Balance}\).

# Predicted values of Balance

results.fittedvalues

0 336.580930

1 887.792481

2 879.131225

3 1147.261223

4 584.509395

...

395 319.675754

396 327.345079

397 596.545638

398 474.707405

399 359.625195

Length: 400, dtype: float64

This is a Pandas Series (single DataFrame column) by default so it can be helpful to convert it to a numpy array for future operations:

yhats = results.fittedvalues.to_numpy()

And we can also get the model residuals or differennce between the observed and predicted values:

results.resid

0 -3.580930

1 15.207519

2 -299.131225

3 -183.261223

4 -253.509395

...

395 240.324246

396 152.654921

397 -458.545638

398 -474.707405

399 606.374805

Length: 400, dtype: float64

Which is the same thing as:

df['Balance'].to_numpy() - results.fittedvalues

0 -3.580930

1 15.207519

2 -299.131225

3 -183.261223

4 -253.509395

...

395 240.324246

396 152.654921

397 -458.545638

398 -474.707405

399 606.374805

Length: 400, dtype: float64

We can similarily convert this DataFrame column to a numpy array:

residuals = results.resid.to_numpy()

statsmodels also gives us the SSE of the model, which it calls the sum-of-the-squared-residuals (SSR):

# Sum of squared residuals

results.ssr

np.float64(66208744.51078422)

Which we can manually verify ourselves:

np.sum(results.resid ** 2)

np.float64(66208744.51078422)

2. Interpreting Parameter Estimates#

Let’s take a look at the estimated \(\beta\) values and try to understand what they mean

results.params

Intercept 246.514751

Income 6.048363

dtype: float64

Let’s take a look back at the plot we made earlier to understand exactly what these estimates refer to

In natural language we would state:

“For each additional thousand dollars of income, a person’s average credit card debt is expected to increased b $6.05”

Wait a minute I thought the Intercept was always the mean of \(y\), what gives?

What parameters mean#

The key lesson to remember when interpeting parameter estimates from any GLM is:

The expected change in \(y\) for 1-unit of change in \(x_i\) when all other model parameters are fixed at 0, this is when \(x_{not\ i} = 0\).

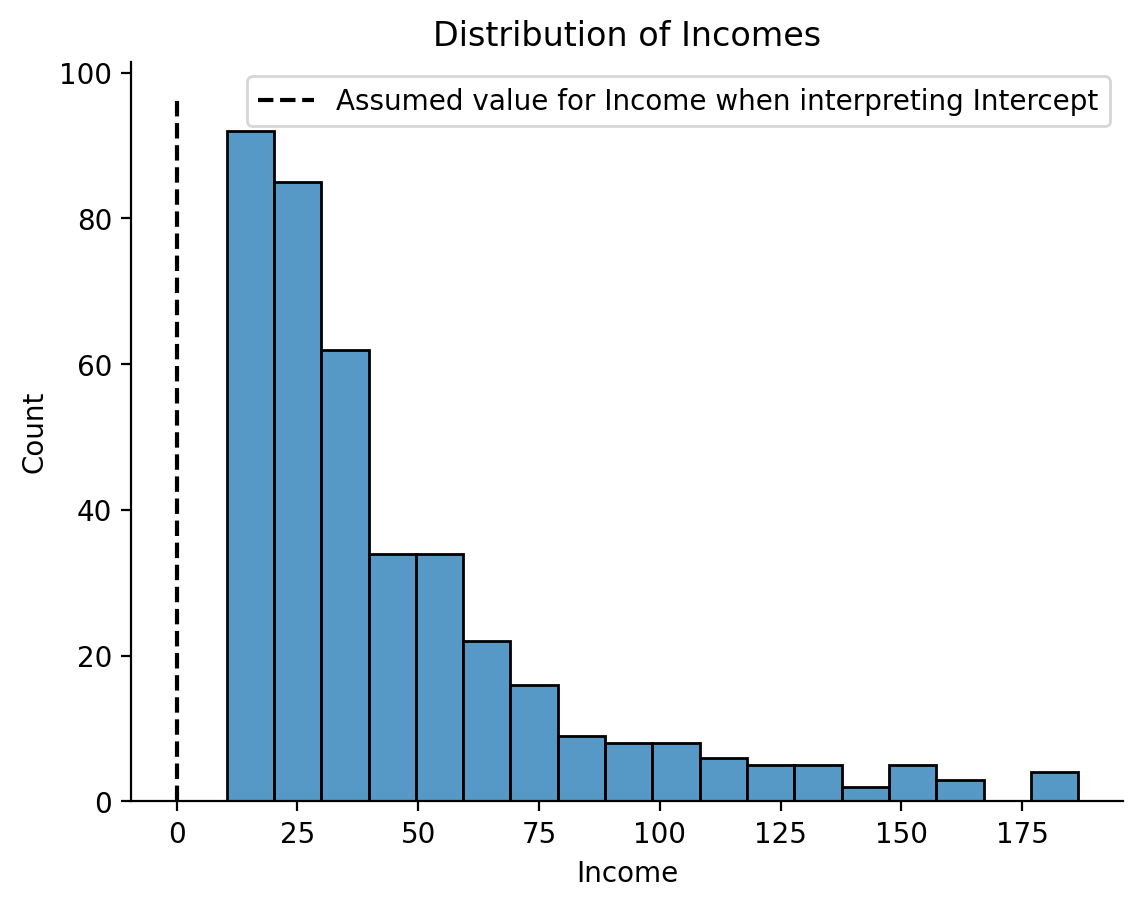

In other words, our Intercept value of \(246.5\) is our prediction for \(\hat{Balance}\) when \(Income = 0\) !

Does this make sense for an estimate we want? More importantly is this even in the range of the observed data?

ax = sns.histplot(df['Income']);

ax.vlines(x=0, ymin=0, ymax=ax.get_ylim()[-1], ls='--', color='k', label='Assumed value for Income when interpreting Intercept');

ax.set(xlabel='Income', title='Distribution of Incomes')

plt.legend();

sns.despine();

In this case, interpreting our Intercept parameter is essentially meaningless because we never actually observed an individual with an Income of 0!

The take-away here is the models will happily make predictions outside the range of your data but often times this isn’t what you want!

Improving interpretations with centering#

What we really want is for our model to estimate an Intercept that assumes Income is fixed at some reasonable value that we measured. How can we do this?

Easy! We can just center our predictor around some meaningful value by subtracting it from each data-point.

Most commonly, you’ll want to mean-center your predictors - which makes the Intercept more interpretable!

Let’s try it out and see what happens. Let’s add a mean-centered Income column to our dataframe:

df = df.with_columns(

Income_centered = col('Income') - col('Income').mean(),

)

df

| Index | Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | Income_centered |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| i64 | f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 | f64 |

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | "Male" | "No" | "Yes" | "Caucasian" | 333 | -30.327885 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | "Female" | "Yes" | "Yes" | "Asian" | 903 | 60.806115 |

| 3 | 104.593 | 7075 | 514 | 4 | 71 | 11 | "Male" | "No" | "No" | "Asian" | 580 | 59.374115 |

| 4 | 148.924 | 9504 | 681 | 3 | 36 | 11 | "Female" | "No" | "No" | "Asian" | 964 | 103.705115 |

| 5 | 55.882 | 4897 | 357 | 2 | 68 | 16 | "Male" | "No" | "Yes" | "Caucasian" | 331 | 10.663115 |

| … | … | … | … | … | … | … | … | … | … | … | … | … |

| 396 | 12.096 | 4100 | 307 | 3 | 32 | 13 | "Male" | "No" | "Yes" | "Caucasian" | 560 | -33.122885 |

| 397 | 13.364 | 3838 | 296 | 5 | 65 | 17 | "Male" | "No" | "No" | "African American" | 480 | -31.854885 |

| 398 | 57.872 | 4171 | 321 | 5 | 67 | 12 | "Female" | "No" | "Yes" | "Caucasian" | 138 | 12.653115 |

| 399 | 37.728 | 2525 | 192 | 1 | 44 | 13 | "Male" | "No" | "Yes" | "Caucasian" | 0 | -7.490885 |

| 400 | 18.701 | 5524 | 415 | 5 | 64 | 7 | "Female" | "No" | "No" | "Asian" | 966 | -26.517885 |

Then let’s estimate a new model with this column and look at its parameter estimates:

model_centered = ols('Balance ~ Income_centered', data=df.to_pandas())

results_centered = model_centered.fit()

results_centered.params

Intercept 520.015000

Income_centered 6.048363

dtype: float64

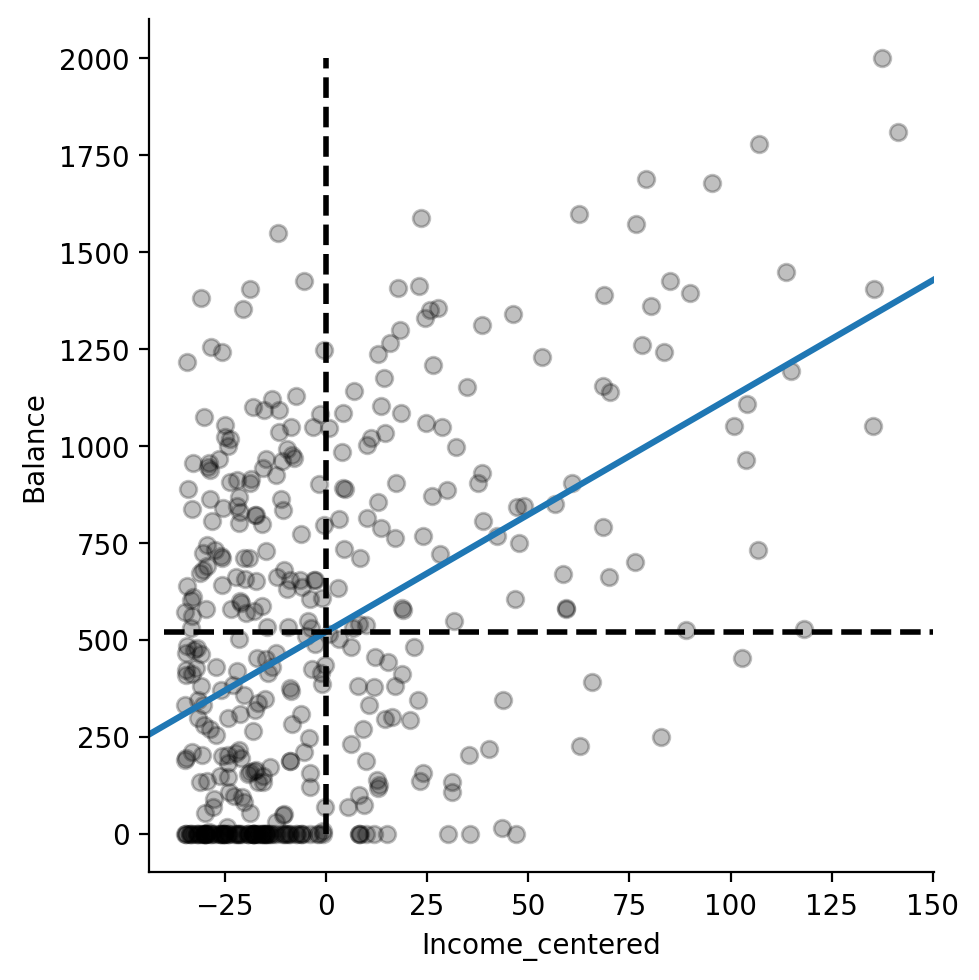

Wow the Intercept changed! What’s going on? How about a visual inspection with seaborn?

grid = sns.lmplot(

data=df,

x='Income_centered',

y='Balance',

fit_reg=True,

ci=None,

scatter_kws={'color':'black', 'alpha':.25},

truncate=False

)

grid.ax.vlines(0, 0, 2000, linestyle='--', color='black', lw=2)

grid.ax.hlines(520, -40, 150, linestyle='--', color='black', lw=2)

<matplotlib.collections.LineCollection at 0x1547f2dd0>

<matplotlib.collections.LineCollection at 0x15496de10>

I’ve added dashed black lines to the figure to illustrate the effect of centering Income.

From the perspective of the model, \(\beta_0\) is now the estimate of the Intercept when Income is held constant at its mean value.

If we draw a vertical line at the new mean of Income_centered, i.e. 0 we can see where it intercepts the regression line.

This is our new estimated \(\beta_0 = 520.015\) !

And just to verify that this is indeed the mean of \(y\), let’s just calculate it:

df.select(

col('Balance', 'Income', 'Income_centered').mean()

)

| Balance | Income | Income_centered |

|---|---|---|

| f64 | f64 | f64 |

| 520.015 | 45.218885 | -7.1054e-17 |

Easy centering with statsmodels formulas#

We can actually do this very easily in statsmodels without having to create a DataFrame column by using center inside our formula.

This is a special operation statsmodels understands that saves us time. Below I’m not saving any outputs or the model itself but just printing the estimated parameters so you can see that they’re the same as before:

ols('Balance ~ center(Income)', data=df.to_pandas()).fit().params

Intercept 520.015000

center(Income) 6.048363

dtype: float64

Take aways about centering#

We’ll discuss centering more when we look at multiple regression in a later notebook, but for now here are some key take-aways:

Centering is a way to fix a parameter estimate at some value (e.g. mean) to aid in the interpretation of other parameter estimates

Centering never changes the parameter estimate of the variable being centered

It only changes the value of other parameter estimates

You should almost always consider centering your continuous variable unless a value of 0 is of theoretical interest!

Centering is incredibly important in multiple regression with interactions, but we’ll cover this in the future

3. Model Evaluation#

statsmodels has made it pretty easy to estimate a model, but before we make strong conclusions about our parameter estimates, we should always at least visually inspect that we’re not violating the course assumptions of the GLM: independent and identitically distributed (iid) errors.

We can do this by inspecting the residuals from our model and looking for any structure in the errors that our model makes.

Let’s do this in 3 ways:

We’ll start by looking at the distribution of residuals using a historgram and QQplot and checking they’re approximately normal (they should be)

We’ll plot the residuals against the predictor variable Income looking for any structure in how the errors vary with the predictor (they shouldn’t)

We’ll look at the residuals against the true value of Balance looking for any values our dependent variable that are particulary mis-predicted by our model

Let’s start by adding columns that contain the residuals to our DataFrame to make plotting easier

df = df.with_columns(

residuals = results.resid.to_numpy(),

residuals_centered = results_centered.resid.to_numpy(),

)

df.head()

| Index | Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | Income_centered | residuals | residuals_centered |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| i64 | f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 | f64 | f64 | f64 |

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | "Male" | "No" | "Yes" | "Caucasian" | 333 | -30.327885 | -3.58093 | -3.58093 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | "Female" | "Yes" | "Yes" | "Asian" | 903 | 60.806115 | 15.207519 | 15.207519 |

| 3 | 104.593 | 7075 | 514 | 4 | 71 | 11 | "Male" | "No" | "No" | "Asian" | 580 | 59.374115 | -299.131225 | -299.131225 |

| 4 | 148.924 | 9504 | 681 | 3 | 36 | 11 | "Female" | "No" | "No" | "Asian" | 964 | 103.705115 | -183.261223 | -183.261223 |

| 5 | 55.882 | 4897 | 357 | 2 | 68 | 16 | "Male" | "No" | "Yes" | "Caucasian" | 331 | 10.663115 | -253.509395 | -253.509395 |

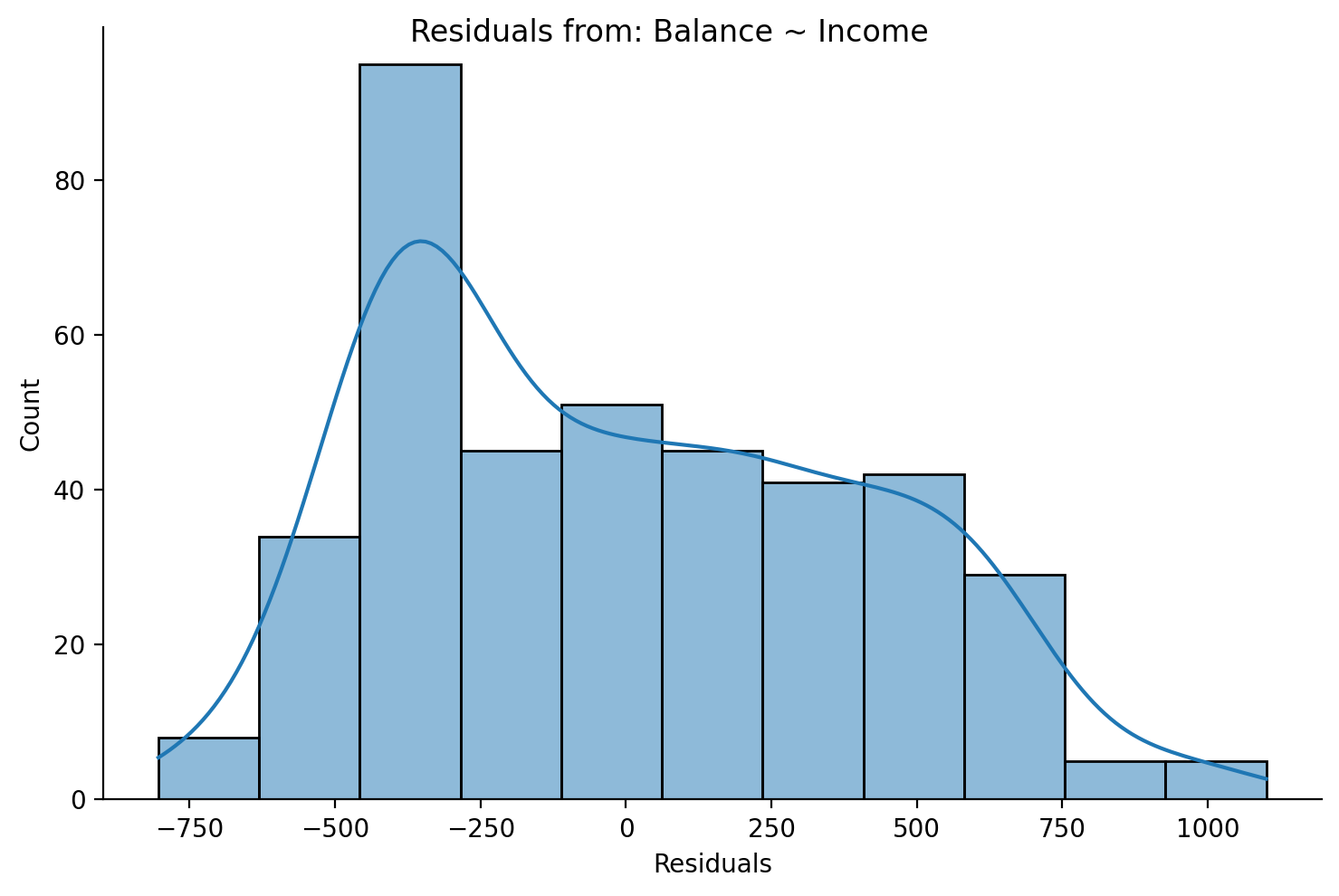

Distrubtion of Residuals#

Residual Histograms#

We can see that the residuals are approximately normal, but there’s a peak between -500 and -250.

grid = sns.displot(data=df,x='residuals',height=5,aspect=1.5, kde=True)

grid.set_axis_labels('Residuals','Count');

grid.figure.suptitle('Residuals from: Balance ~ Income');

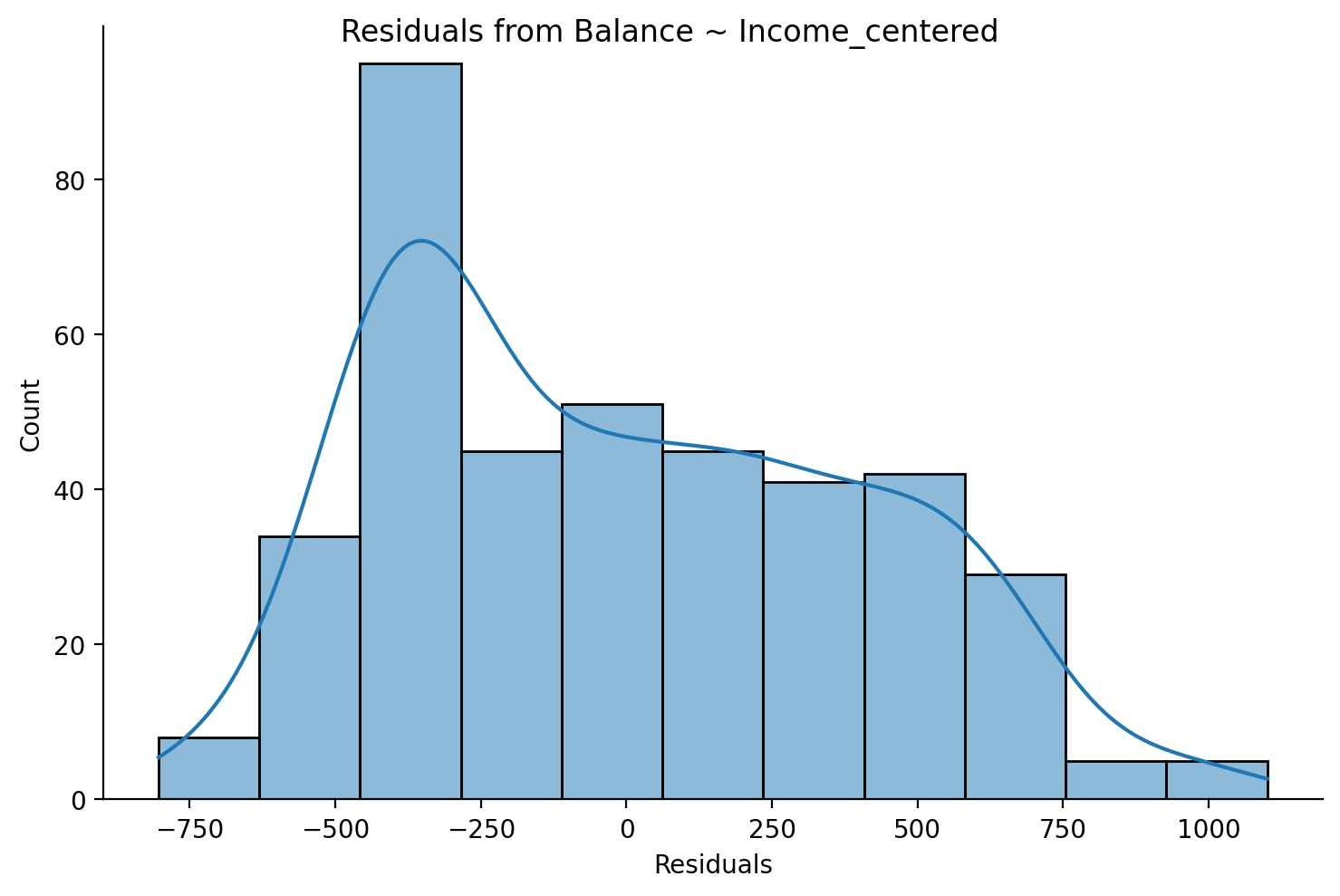

This is also true if we plot the residuals from our centered model because centering doesn’t change the prediction accuracy of a model!

grid = sns.displot(data=df,x='residuals_centered',height=5,aspect=1.5, kde=True)

grid.set_axis_labels('Residuals','Count');

grid.figure.suptitle('Residuals from Balance ~ Income_centered');

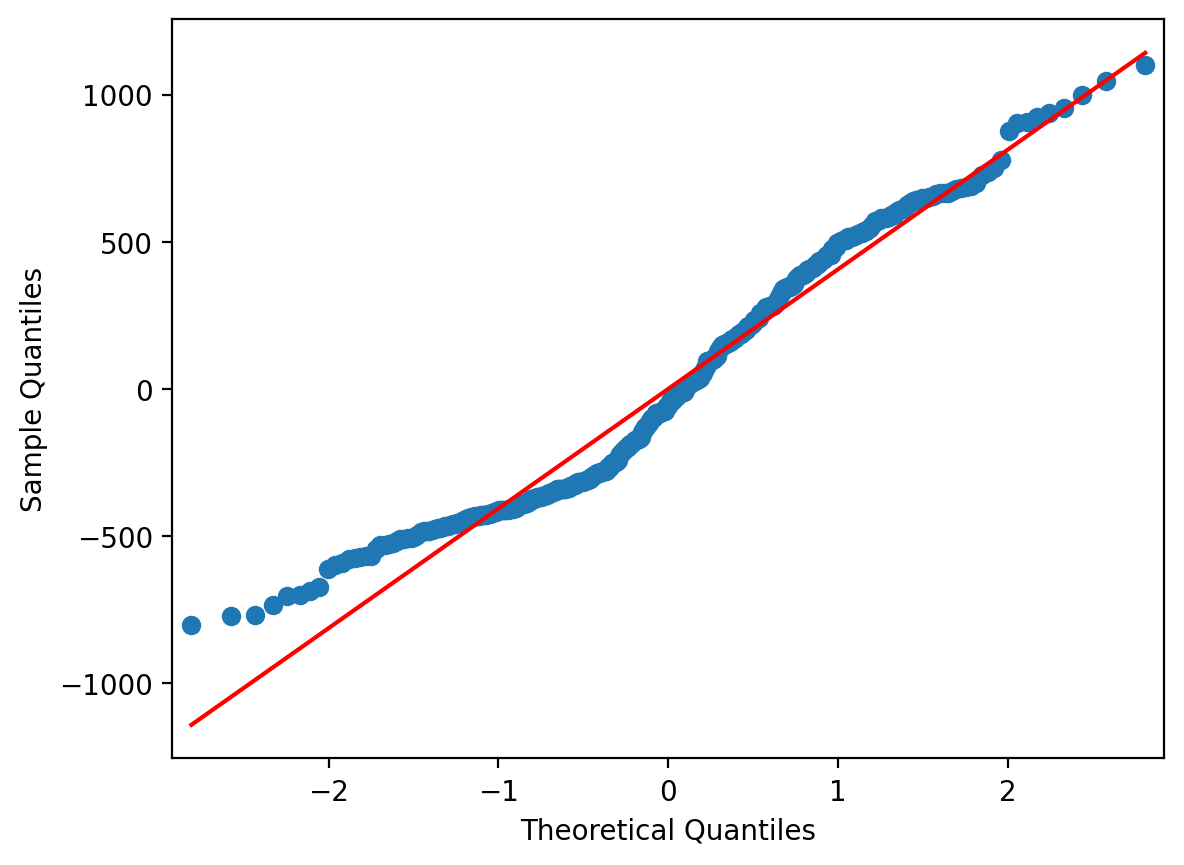

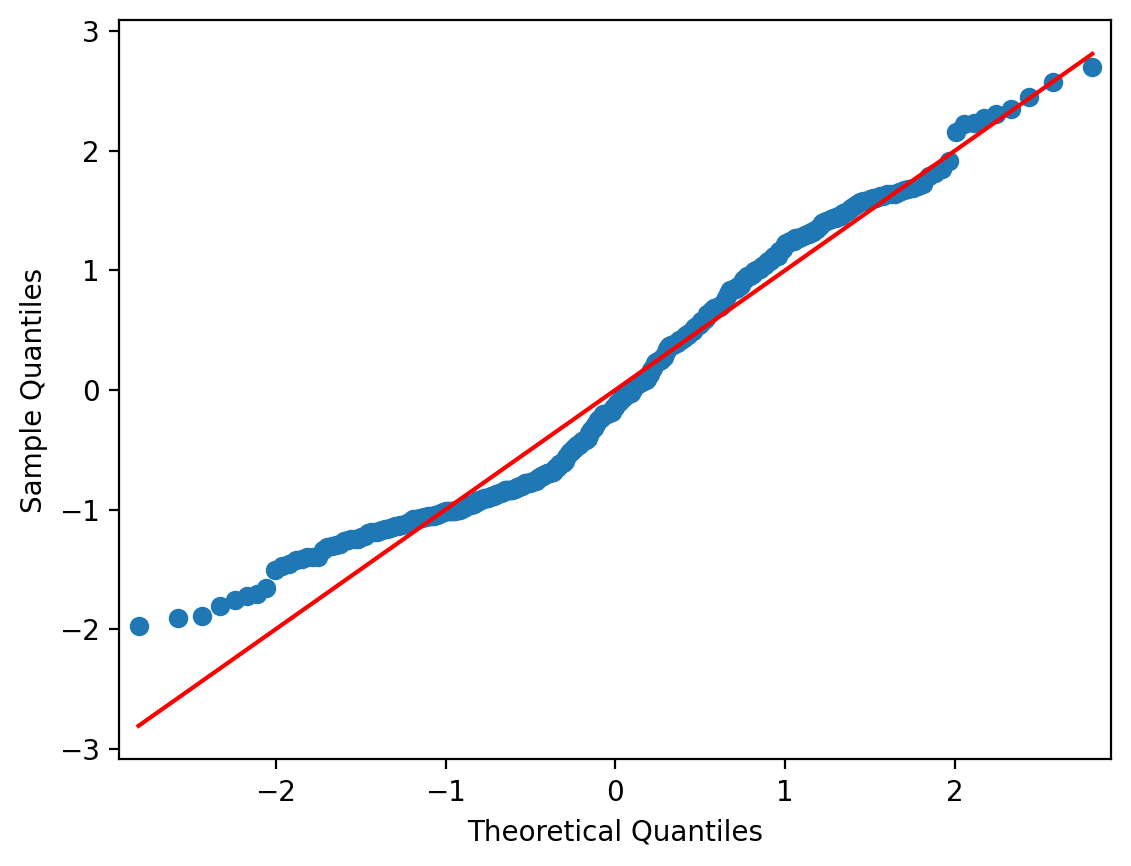

Residual QQPlots#

Another useful way to examine the distribution of your residuals that can supplement a histogram is a QQ plot.

This is a plot of the quantiles of the residuals against the theoretical quantiles of a standard normal distribution.

We can do this using the qqplot function from statsmodels which takes DataFrame column or array of residuals as input. The line = s tells qqplot to add in a red identity line across standard normal quantiles.

If our residuals were perfectly normally distributed, then they would lie right on the red identity line.

Deviations above or below the line tell you how far away from normality the residuals are.

Overall, this QQplot looks pretty good. But we can see that towards the low end of data values, it veers upwards - similar to the spike we saw in the histogram.

# Import it

from statsmodels.graphics.gofplots import qqplot

# Pass it the column that contains the residuals

qqplot(df['residuals'], line = 's');

Sometimes it’s helpful to see the standardized residuals instead, especially if you wanted to compare QQplots with different scales.

To do so we can use the results from our model.fit() and call the .get_influence() method on it. This returns a few different things, but we care about .resid_studentized, which converts our residuals to an approximately standard-deviation scale.

In this case the QQplot looks pretty much the same, but notice how the y-axis is now in units of standard-deviation instead of raw data:

# Standardized are sometimes easier to compare across models

qqplot(results.get_influence().resid_studentized, line = 's');

Residuals and Predictors#

Residual Scatterplots#

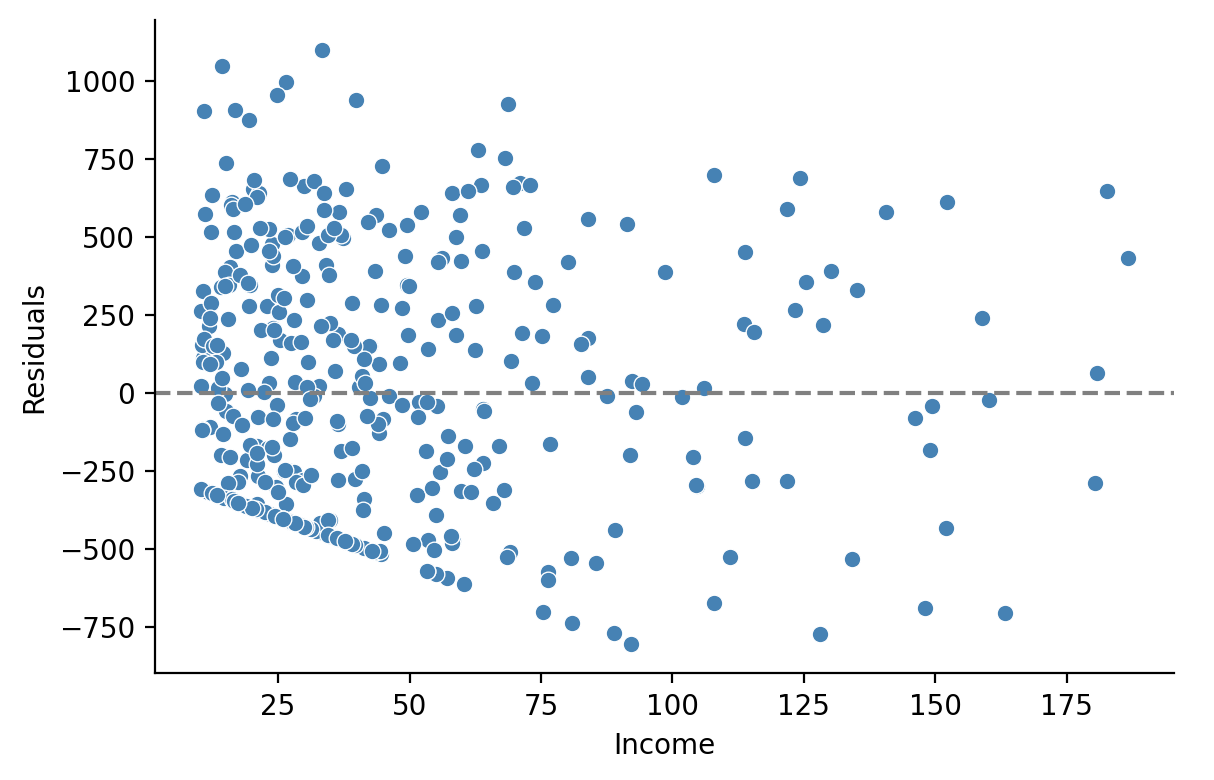

Let’s see if we can figure out what that peak is. It might help to plot the residuals against the predictor \(X\) Income

grid = sns.FacetGrid(data=df, height=4,aspect=1.5)

# Residuals vs Income

grid.map(sns.scatterplot, 'Income', 'residuals', color='steelblue');

# Horizontal line at 0

grid.map(plt.axhline, y=0, color='gray', linestyle='--');

# Labels and legend

grid.set_axis_labels('Income', 'Residuals');

grid.add_legend();

Indeed we can see that most of the error in our model is coming from the mis-predicted observations from people with an \(Income < 50\)

Since so many people below this threshold carry a Balance of \(0, there's no *variance* in the \)y$ values our model observes and therefore it can’t incorporate this into the parameter estimates!

Our errors are therefore due to a lack of variance in that region of the data itself!

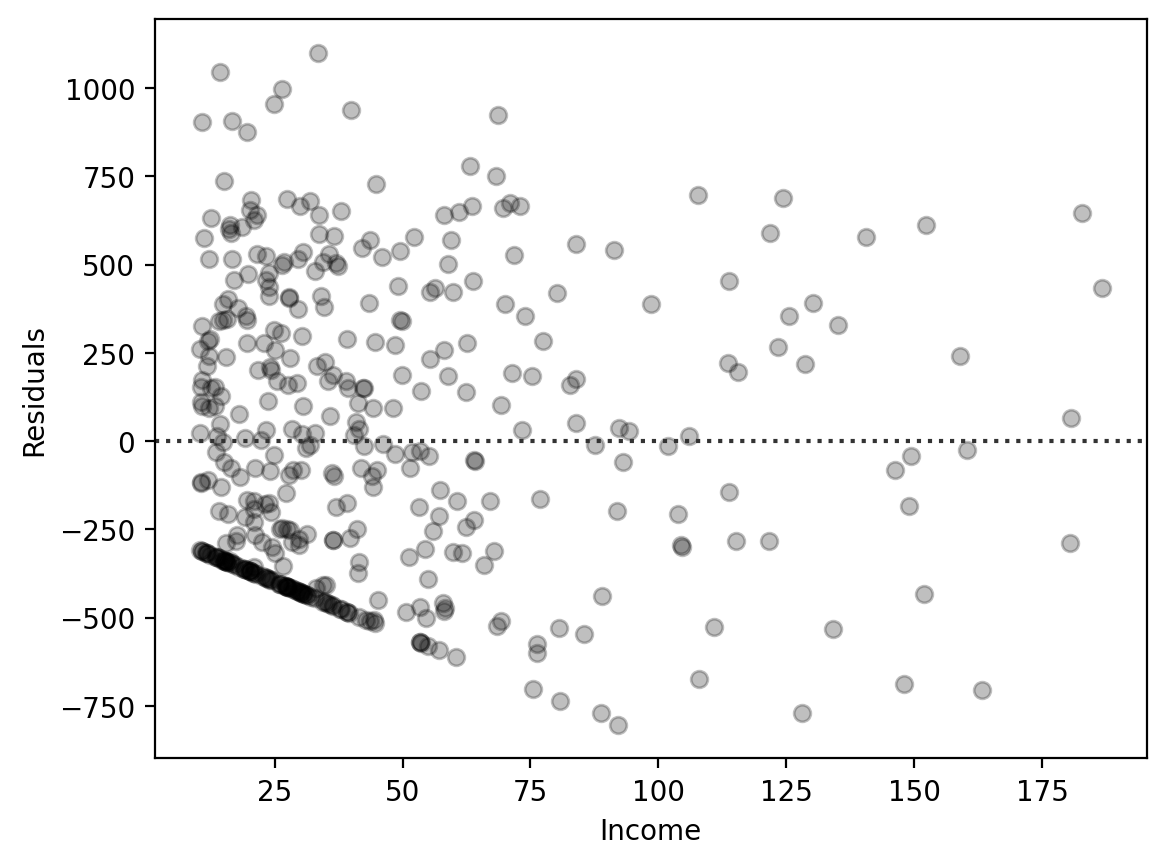

Note on sns.residplot#

seaborn offers a handy axis-level function called sns.residplot that can be used to plot residuals even before you’ve fitted a model.

It can be handy for exploring simple univariate regression models because seaborn will automatically estimate an ols model and calculate the residuals for you give the column that corresponds to your \(X\) variable and a column that corresponds to your \(y\) variable.

ax = sns.residplot(

data=df,

x='Income',

y='Balance', # Give it the column of the DV directly!

scatter_kws={'color':'black', 'alpha':.25},

)

ax.set(xlabel='Income', ylabel='Residuals');

In general thought, I find sns.residplot a bit in-flexible and prefer to create my own figures using other seaborn functions by adding columns to my DataFrame and plotting those like we did before.

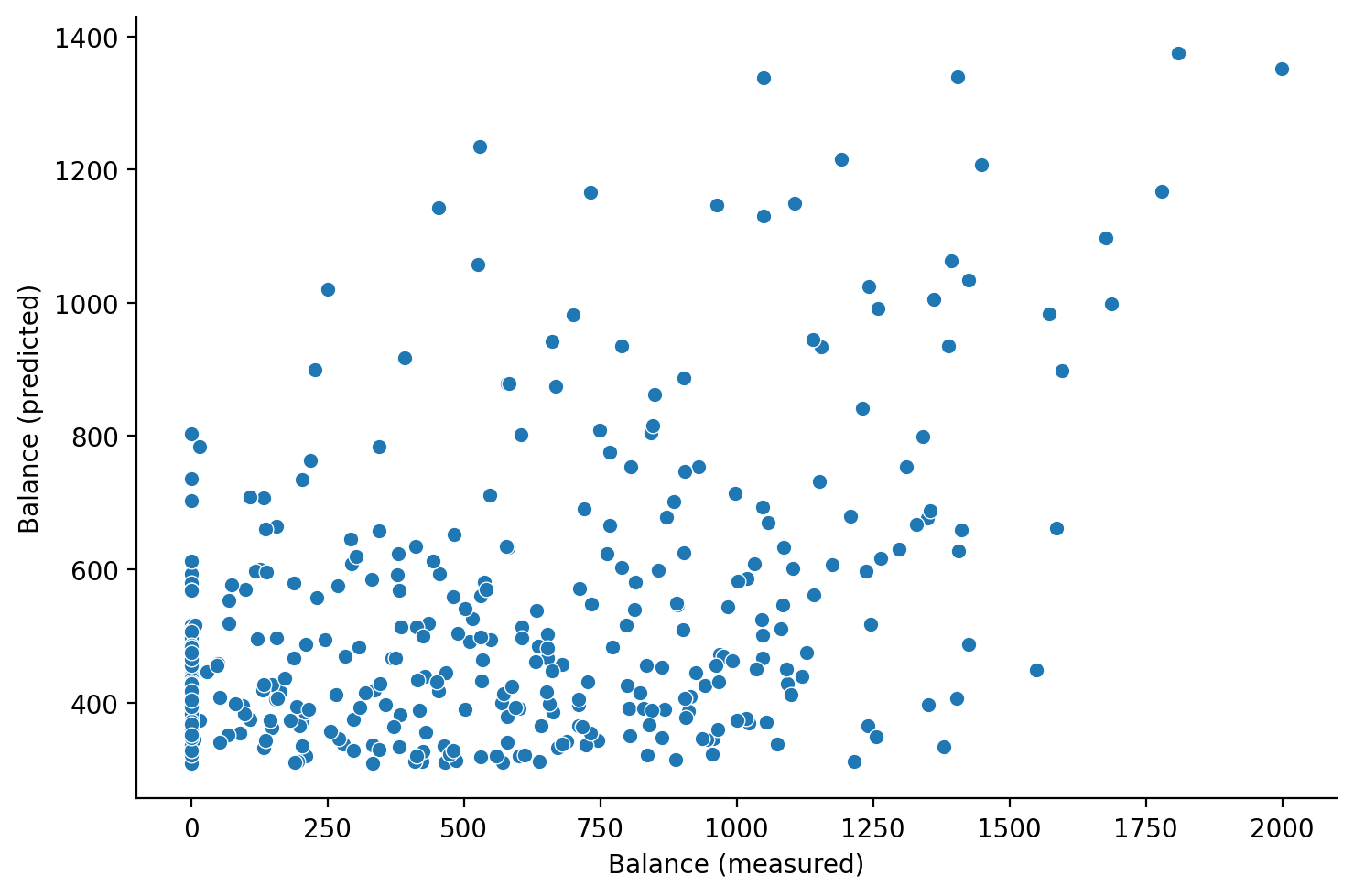

Residuals and Outcomes#

Inspecting Model Predictions#

Finally it’s always a good idea to plot the predictions of our model \(\hat{Balance}\) against our observed values of \(Balance\).

Let’s add a column to our DataFrame and visualize the relationship

df = df.with_columns(

Balance_predictions = results.fittedvalues.to_numpy()

)

df.head()

| Index | Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | Income_centered | residuals | residuals_centered | Balance_predictions |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| i64 | f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 | f64 | f64 | f64 | f64 |

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | "Male" | "No" | "Yes" | "Caucasian" | 333 | -30.327885 | -3.58093 | -3.58093 | 336.58093 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | "Female" | "Yes" | "Yes" | "Asian" | 903 | 60.806115 | 15.207519 | 15.207519 | 887.792481 |

| 3 | 104.593 | 7075 | 514 | 4 | 71 | 11 | "Male" | "No" | "No" | "Asian" | 580 | 59.374115 | -299.131225 | -299.131225 | 879.131225 |

| 4 | 148.924 | 9504 | 681 | 3 | 36 | 11 | "Female" | "No" | "No" | "Asian" | 964 | 103.705115 | -183.261223 | -183.261223 | 1147.261223 |

| 5 | 55.882 | 4897 | 357 | 2 | 68 | 16 | "Male" | "No" | "Yes" | "Caucasian" | 331 | 10.663115 | -253.509395 | -253.509395 | 584.509395 |

grid = sns.relplot(

data=df,

x="Balance",

y="Balance_predictions",

kind='scatter',

height=5,

aspect=1.5,

)

# Labels and legend

grid.set_axis_labels('Balance (measured)', 'Balance (predicted)');

Coefficient of Determination (\(R^2\))#

We can quantify the quality of our predictions by calculating the coefficient of determination.

The coefficient of determination, often denoted as \(R^2\), measures the proportion of variance in the dependent variable that is predictable from the independent variable(s).

Where:

\(SS_{\text{res}}\) is the residual sum of squares, \(e^Te\).

\(SS_{\text{tot}}\) is the total sum of squares, adjusting for the mean, \((y-\bar{y})^T(y-\bar{y})\).

A value of \(R^2\) close to 1 suggests that a large proportion of the variability in the outcome has been explained by the regression model.

A value close to 0 indicates the model is missing a large amount of variability in the outcome

A value below 0 indicates the model is systematically mis-predicting in some way

We can use the handy r2_score function from the sklearn library to calculate this for us. We haven’t discussed this library yet, but we’ll come back to it later.

r2_score takes in two arguments:

y_true: the true values of the dependent variabley_pred: the predicted values of the dependent variable

from sklearn.metrics import r2_score

r2_score(df['Balance'].to_numpy(), df['Balance_predictions'].to_numpy())

0.21497731013240484

And in fact we can see that this matches the output that statsmodels gives us in its .rsquared attribute:

results.rsquared

np.float64(0.21497731013240484)

Challenge: Inspect models of Anscombe’s Quartet#

In the following cell we’ve loaded Anscombe’s quarted for you into a DataFrame.

anscombe = pl.DataFrame(sns.load_dataset('anscombe'))

anscombe

| dataset | x | y |

|---|---|---|

| str | f64 | f64 |

| "I" | 10.0 | 8.04 |

| "I" | 8.0 | 6.95 |

| "I" | 13.0 | 7.58 |

| "I" | 9.0 | 8.81 |

| "I" | 11.0 | 8.33 |

| … | … | … |

| "IV" | 8.0 | 5.25 |

| "IV" | 19.0 | 12.5 |

| "IV" | 8.0 | 5.56 |

| "IV" | 8.0 | 7.91 |

| "IV" | 8.0 | 6.89 |

Using

.filter()in polars, create 4 new dataframes, one per dataset, and fit 4 separateolsmodels

# Your code here

df1 = anscombe.filter(col('dataset') == "I")

df2 = anscombe.filter(col('dataset') == "II")

df3 = anscombe.filter(col('dataset') == "III")

df4 = anscombe.filter(col('dataset') == "IV")

# Your code here

m1 = ols('y ~ x', data=df1.to_pandas())

m1r = m1.fit()

m2 = ols('y ~ x', data=df2.to_pandas())

m2r = m2.fit()

m3 = ols('y ~ x', data=df3.to_pandas())

m3r = m3.fit()

m4 = ols('y ~ x', data=df4.to_pandas())

m4r = m4.fit()

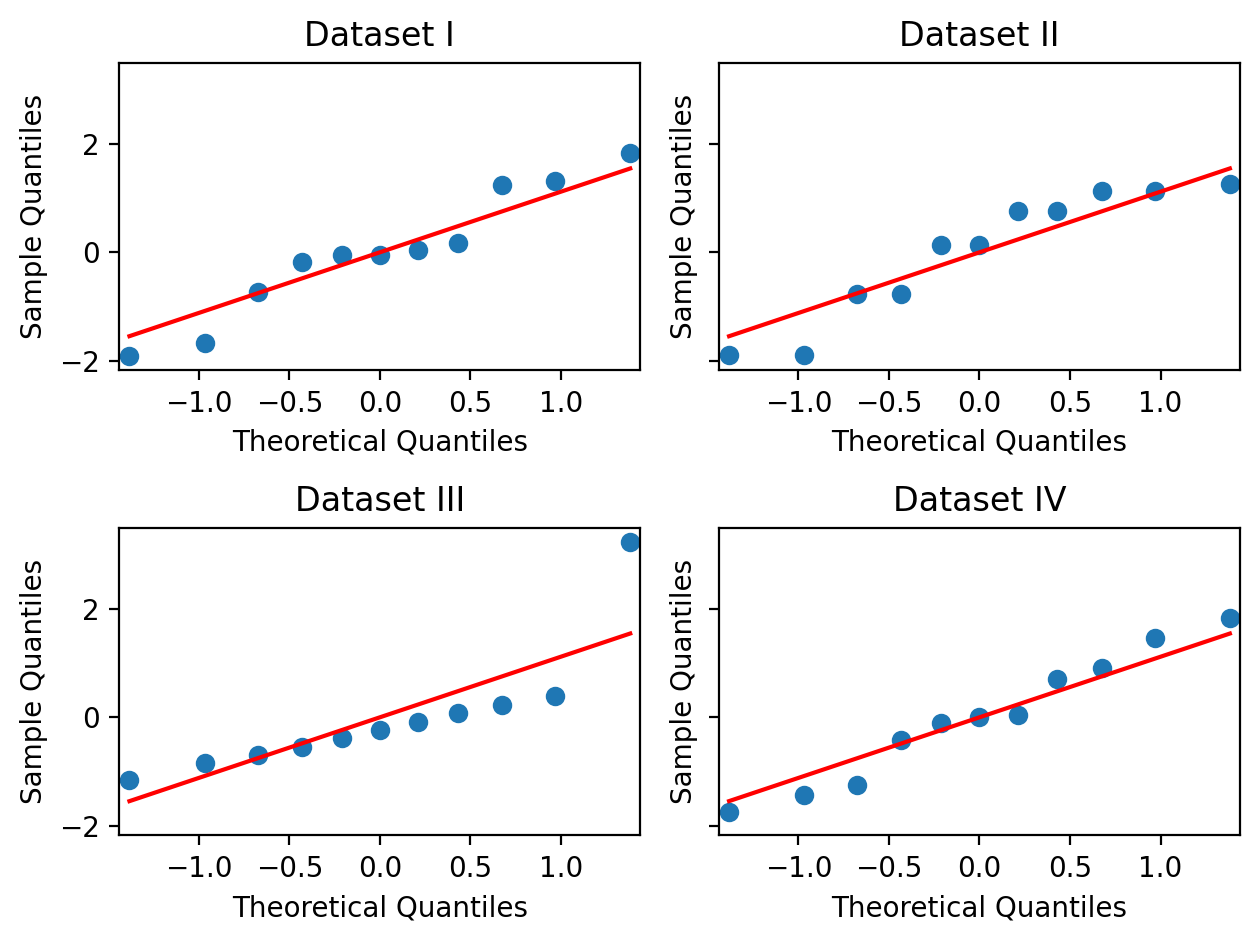

Visualize the residuals of each model using a

qqplotHow do these compare to plots of the original data?

# Your code here

f, axs = plt.subplots(2,2, sharey=True, sharex=False)

# Assign to throw-away variable _ to prevent double plotting

_ = qqplot(m1r.resid, line='s',ax=axs[0,0]);

axs[0,0].set_title('Dataset I');

_ = qqplot(m2r.resid, line='s',ax=axs[0,1]);

axs[0,1].set_title('Dataset II');

_ = qqplot(m3r.resid, line='s',ax=axs[1,0]);

axs[1,0].set_title('Dataset III');

_ = qqplot(m4r.resid, line='s',ax=axs[1,1]);

axs[1,1].set_title('Dataset IV');

# Make sure stuff doesn't overlap!

plt.tight_layout();

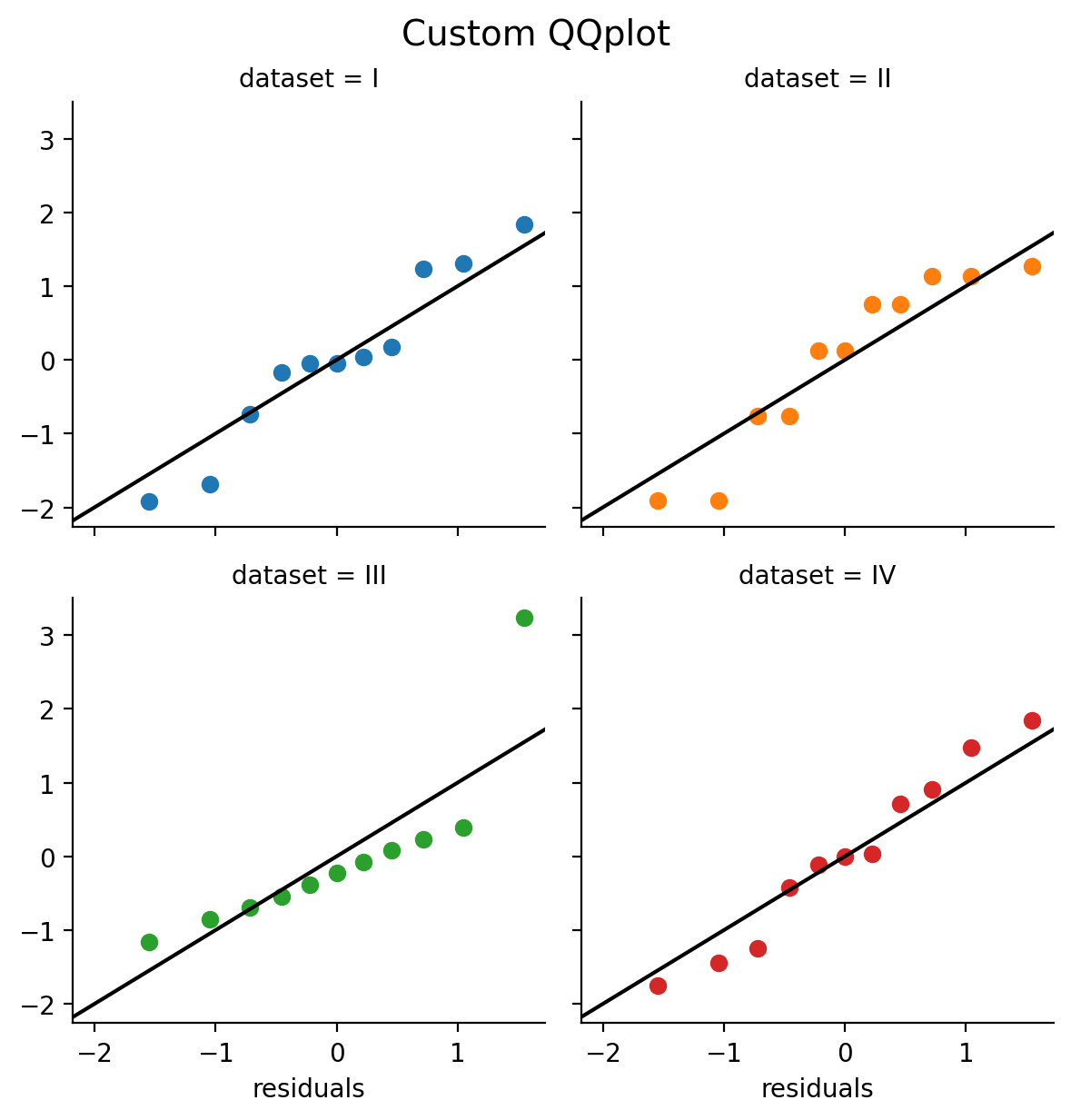

Here’s a way we can do this using FacetGrid and a custom qqplot_custom based on this example from the seaborn website.

# First we define a custom function to make a qqplot

def qqplot_custom(x, **kwargs):

from scipy import stats

# Calculate quantiles using probplot

quantiles, xr = stats.probplot(x, fit=False)

# Make a scatterplot

plt.scatter(quantiles, xr, **kwargs)

# Plot the unity line

plt.axline((-2,-2), slope=1., color='k');

Then let’s concatenate all our models’ residuals into a numpy array and save it as a new column our original DataFrame:

anscombe = anscombe.with_columns(

residuals = np.concatenate([

m1r.resid,

m2r.resid,

m3r.resid,

m4r.resid])

)

anscombe

| dataset | x | y | residuals |

|---|---|---|---|

| str | f64 | f64 | f64 |

| "I" | 10.0 | 8.04 | 0.039 |

| "I" | 8.0 | 6.95 | -0.050818 |

| "I" | 13.0 | 7.58 | -1.921273 |

| "I" | 9.0 | 8.81 | 1.309091 |

| "I" | 11.0 | 8.33 | -0.171091 |

| … | … | … | … |

| "IV" | 8.0 | 5.25 | -1.751 |

| "IV" | 19.0 | 12.5 | -5.3291e-15 |

| "IV" | 8.0 | 5.56 | -1.441 |

| "IV" | 8.0 | 7.91 | 0.909 |

| "IV" | 8.0 | 6.89 | -0.111 |

# Then we create a facet grid

grid = sns.FacetGrid(data=anscombe.to_pandas(), col='dataset', hue='dataset', col_wrap=2);

# And ap our custom function to each facet and pass the residuals column to x

grid.map(qqplot_custom,'residuals');

grid.figure.suptitle("Custom QQplot", y=1.02, fontsize=14);

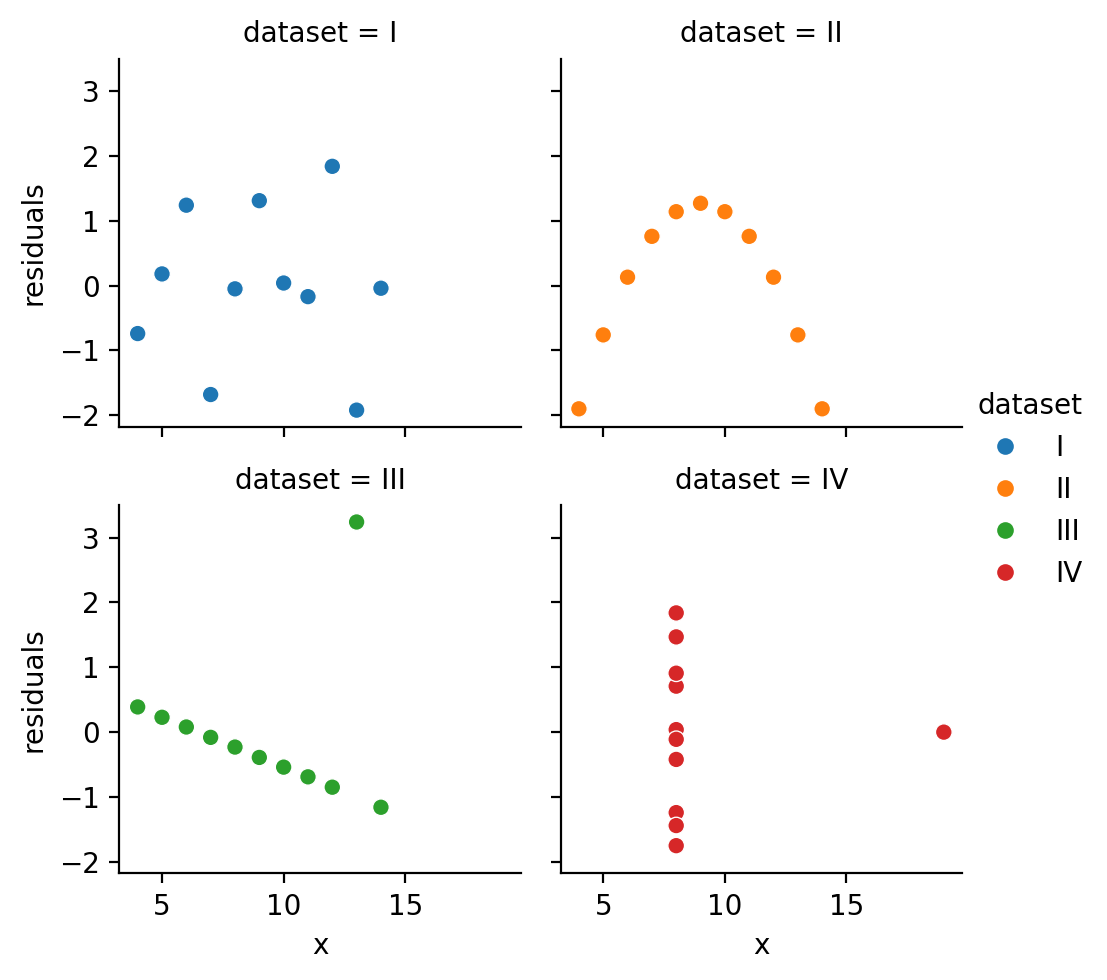

It also might be nice to see a regular residual plot

sns.relplot(

data=anscombe,

kind='scatter',

x='x',y='residuals',

col='dataset', hue='dataset',

col_wrap=2,

height=2.5,

)

<seaborn.axisgrid.FacetGrid at 0x304ec4710>

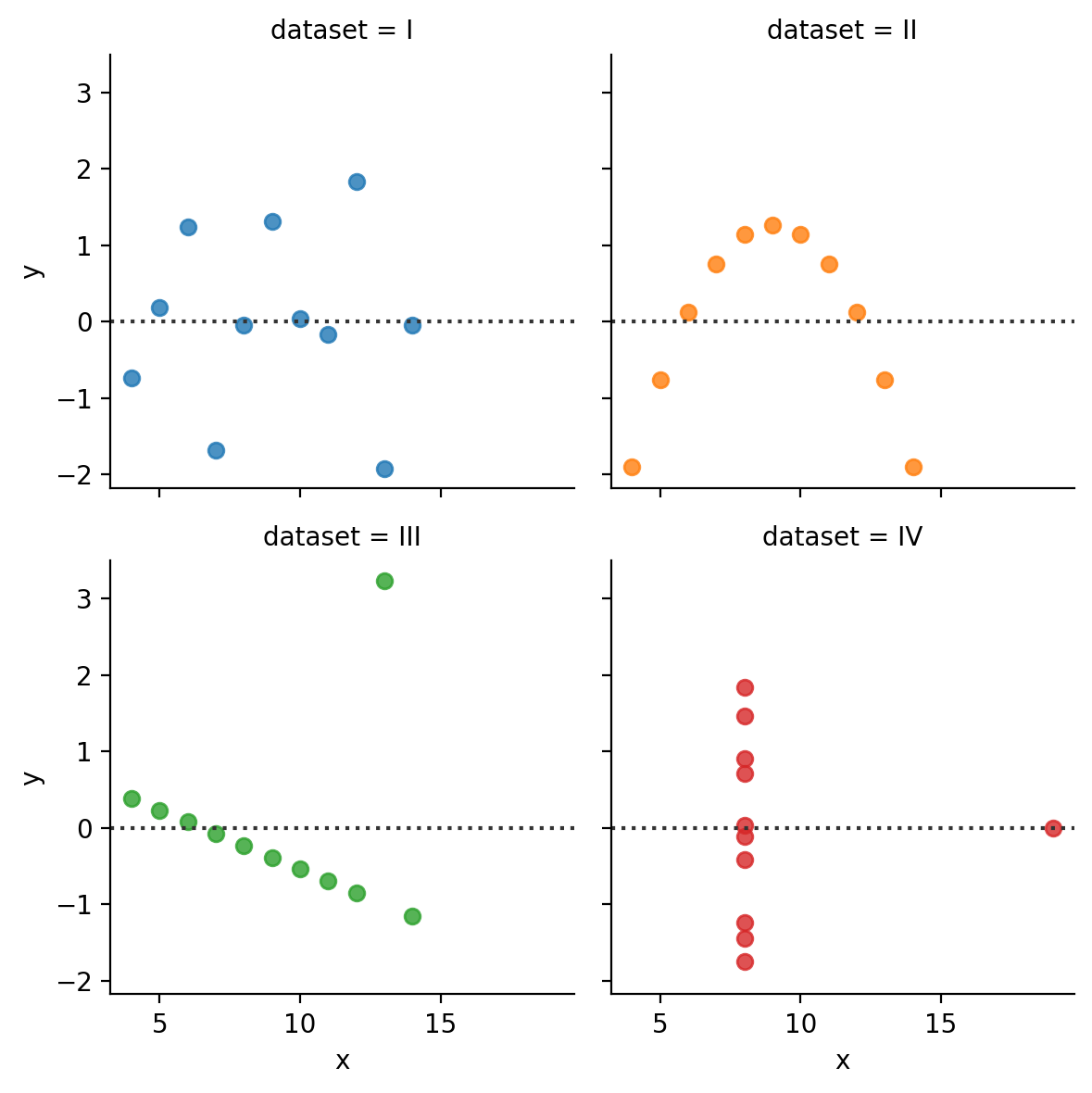

We can achieve the same thing by using a FacetGrid and mapping sns.residplot to each facet.

But this doesn’t give us a lot of control over the residuals themselves. seaborn will calculate the ols in the background but we can’t access them or modify the model:

grid = sns.FacetGrid(data=anscombe.to_pandas(), col='dataset', hue='dataset', col_wrap=2);

grid.map(sns.residplot, 'x', 'y')

<seaborn.axisgrid.FacetGrid at 0x16a74c650>

4. Model Comparison#

Now that we’ve seen how to estimate a model using ols how do we know whether the slope we’re observing between Income and Balance is meaningful?

In class we learned that we can formulate our hypotheses as model comparisons, i.e. comparing a compact model to an augmented model and asking whether the trade-off between adding more parameters and the proportional reduction in error (PRE) is worth it.

The Manual Way: Building Intuitions#

Let’s see how to implement this using statsmodels ourselves. We already have our augmented model that includes Income as predictor. So let’s create and fit a compact model that doesn’t:

# Model with only an intercept term - i.e. mean of Balance

compact_model = ols("Balance ~ 1", data=df.to_pandas())

compact_results = compact_model.fit()

# Same as our model above, just redefining it here for clarity

# 2 parameters: Intercept + Slope of Income

augmented_model = ols("Balance ~ Income", data=df.to_pandas())

augmented_results = augmented_model.fit()

Now let’s calculate our PRE using the SSE of each model. Remember we can access this using the .ssr attribute of a model’s results object:

error_c = compact_results.ssr

error_a = augmented_results.ssr

PRE = (error_c - error_a) / error_c

print(f"Proportional Reduction in Error: {PRE:.2f}")

Proportional Reduction in Error: 0.21

This tells us that adding Income as a predictor reduces our SSE in predicting Balance by about 21%.

This estimate is the same as our coefficient of variation (\(R^2\)) from earlier!

It turns out for univariate regression only, the PRE is identical to the coefficient of variation!

That seems good, but is it worth it?

To answer this question we need to know the sampling distribution of PRE - i.e. how uncertain we are about this single PRE we calculated. Had we collected another dataset, our PRE could be a bit different…

We could use what we learned about resampling to calculate this distribution, but we’ll explore that later…

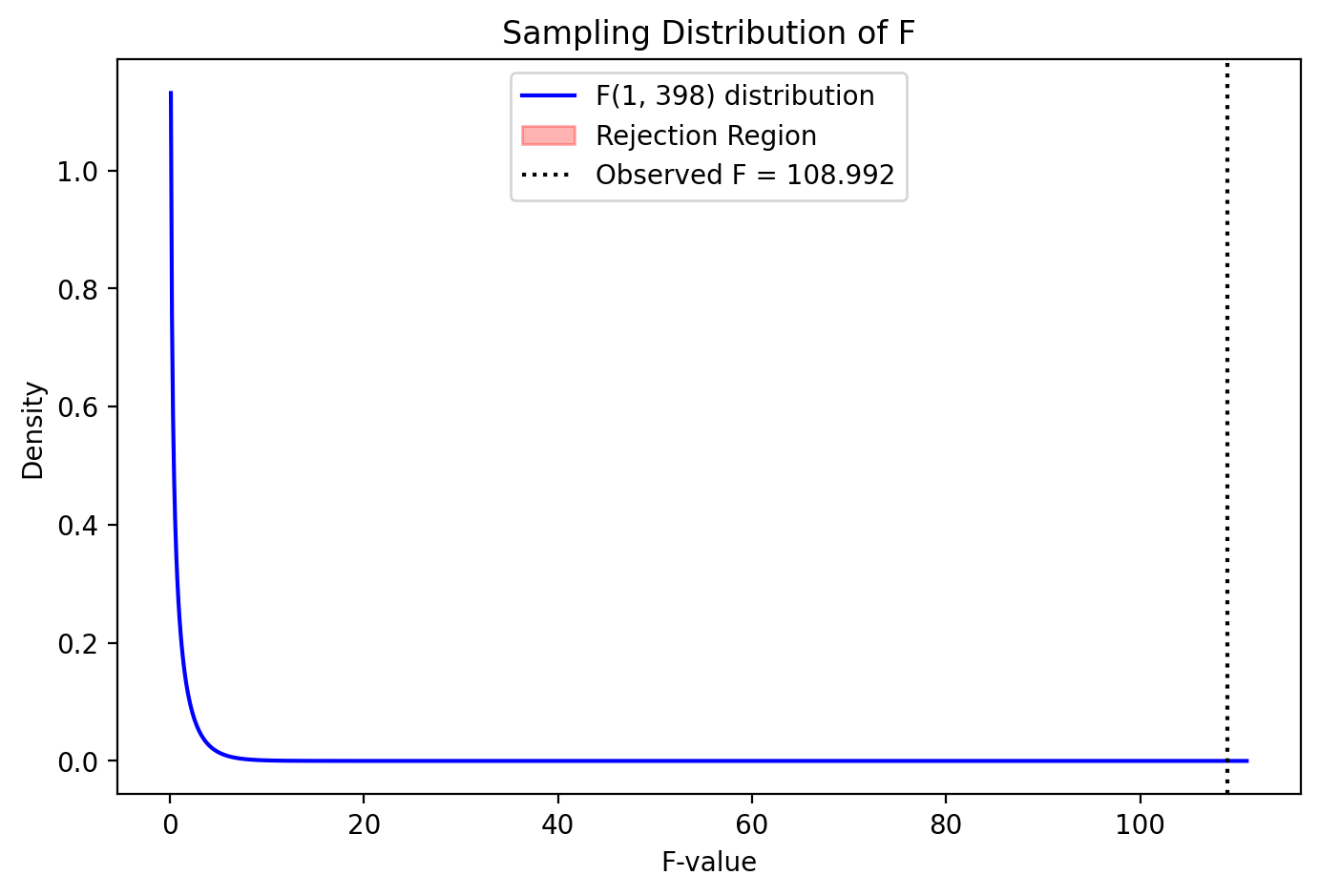

For now, a shortcut we can exploit is that the sampling distribution of PRE is awfully similar to the sampling distribution of the F-statistic (see above image).

In fact we can convert between the two, and get the analytic sampling distribution as follows:

Let’s calculate that now:

pa = 2 # intercept + slope

pc = 1 # intercept only

n = df.height

F = (PRE / (pa - pc)) / ((1 - PRE) / (n - pa))

print(f"PRE to F: {PRE:.2f} to {F:.2f}")

PRE to F: 0.21 to 108.99

To look up the analytic sampling distribution and calculate a p-value we can use scipy which contains many different types of distributions. We’ll import the F distribution and look for proportion of values equal to greater than our observed F-statistic.

We can use the cumulative distribution function of the F-statistic as our sampling distribution - this is a distribution of probabilities that F will take on some value given some “degrees of freedom.”

from scipy.stats import f

# Difference in number of model degrees of freedom = difference in number of parameters

model_df = pa - pc

# Error df = number of observations - number of model parameters in augmented model

error_df = df.height - pa

pval = 1 - f.cdf(F, model_df, error_df)

print(f"Proportion Reduction of Error: = {PRE:3f}, F = {F:3f}, p = {pval:.4f}")

Proportion Reduction of Error: = 0.214977, F = 108.991715, p = 0.0000

To visualize this sampling distribution we can use the following helper function provided by your instructors.

But with such a large F-statistic the rejection region is off the plot - it’s very worth it to add this additional parameter!

from helpers import plot_F_sampling_distribution

plot_F_sampling_distribution(PRE, F, pval, pa, pc, n)

Proportion Reduction of Error: 0.215, F = 108.992, p = 0.0000

Aside on degrees of freedom#

Ok let’s take a second to try to understand degrees of freedom (df) a little better. DF is the number of dimensions along which a quantity can vary. For example, let’s say we have the following data points for a variable \(x: [3, 5, 7, 9, 11]\), and estimate the sample mean which is \(7\). With this estimate in hand, we can recover any single value if it were missing.

For example, let’s say we didn’t know what the first value was: \(x: [nan, 5, 7, 9, 11]\)

Using the mean we estimated, \(7\), we know that this value must be \(3\). It’s value is “fixed” and thus determined by the rest of the values and the mean we calculated. Why? Because the mean of \(7\) implies that the sum of all of the values is \(7 * n = 35\). And \(35 - (5 + 7 + 9 + 11) = 3\).

When you think/read about “losing” or “consuming” a degree of freedom, it means that there is an observation who’s value that is no longer free to vary after estimating a parameter. This is why we often “correct” for degrees of freedom in sample statistics, like the sample variance by dividing by \(n-1\):

Because the sample variance \(\sigma_x^2\) is a function of the sample mean \(\bar{x}\), we have 1 data-point who’s value is fixed based upon is this particular sample mean. Hence the true number of independent observations we have is \(n-1\)

Degrees of freedom in GLM#

In the GLM, degrees-of-freedom are associated with both the independent parameters (model df) and independent errors (error df).

Model df (or “numerator df”) is generally equal to the number of parameters \(p\), assuming none of the predictors in X are redundant. For our compact model, \(p = 1\) because we’re only estimating 1 parameter, the intercept.

Likewise, for our augmented model \(p = 2\) because we’re estimating both an intercept and a slope.

Error df (or “denominator df”), assuming the errors are independent, is the number of observations (\(n\)) minus the number of model parameters estimated (\(p\)). For our compact model this is \(400 - 1\) and for our augmented model it is \(400 - 2\).

Using these values we can using the f.cdf function like we did above to calculate the p-value associated with our calculated F-statistic!

The Easier Way: What you’ll do in practice#

Fortunately statsmodels has a built-in function to automate this process for us: anova_lm(). This function takes 1 or more results from fitted ols models and compares them in the same way we just did:

# Due to a quirk of how statsmodels was made, we need to import and use anova_lm() like this

import statsmodels.api as sm

sm.stats.anova_lm(compact_results, augmented_results)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 399.0 | 8.433991e+07 | 0.0 | NaN | NaN | NaN |

| 1 | 398.0 | 6.620874e+07 | 1.0 | 1.813117e+07 | 108.991715 | 1.030886e-22 |

Notice we get the same F-statistic and p-value as before!

Parameter Inference: Meet .summary()#

Up until now we’ve been manually accessing the various attributed of the results from a fitted model, e.g. results.ssr.

Of course, like R statsmodels can provide all these values plus additional information in a handy summary.

We can use the .summary() method on a results object to get all of these statistics plus more in a single line of code:

# Note: I find it a bit easier to read the summary table if you put it inside a print() function

print(augmented_results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.215

Model: OLS Adj. R-squared: 0.213

Method: Least Squares F-statistic: 109.0

Date: Wed, 12 Feb 2025 Prob (F-statistic): 1.03e-22

Time: 16:47:16 Log-Likelihood: -2970.9

No. Observations: 400 AIC: 5946.

Df Residuals: 398 BIC: 5954.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 246.5148 33.199 7.425 0.000 181.247 311.783

Income 6.0484 0.579 10.440 0.000 4.909 7.187

==============================================================================

Omnibus: 42.505 Durbin-Watson: 1.951

Prob(Omnibus): 0.000 Jarque-Bera (JB): 20.975

Skew: 0.384 Prob(JB): 2.79e-05

Kurtosis: 2.182 Cond. No. 93.3

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

This website has a comprehensive breakdown of this output.

But let’s highlight the key statistics that we’ve been focusing on so far and remind ourselves what they mean:

\(F\ statistic\): the

Fvalue we calculated using the PRE\(DF\ Residuals\): number of observations (400) minus the number of parameters (2) we estimated

\(Prob\ (F\ statistic)\): the

pvalvalue we calculated using analytic sampling distribution ofF\(\beta_0\): the

coefvalue of theIntercept\(\beta_1\): the

coefvalue of theIncome

Parameter Inference as nested model comparison#

We haven’t talked about what the \(t\) or \(std err\) of each parameter means yet, but you might notice that for Income, the statistic \(t\) is equal to \(\sqrt{F}\), i.e. \(10.44 = \sqrt{108.99}\)

np.sqrt(results.fvalue)

np.float64(10.439909730990184)

results.tvalues['Income']

np.float64(10.439909730990186)

This tells us that when we talk about performing statistical inference on a parameter estimate, it’s proportional to performing a comparison between 2 nested models:

a compact model with some parameters

an augmented model with all the same parameters plus a new one we want to make an inference about, e.g. \(Income\)

In other words, testing the hypothesis that the slope of Income in predicting Balance is different that 0:

is equivalent to testing whether the proporational reduction in error (PRE), between two models, that differ only in that parameter, is worth it:

In a later notebook we’ll talk about how to perform parameter inference using the uncertainty of each \(\hat{\beta}\) estimate (i.e. it’s standard-error), but the interpretation doesn’t really change!

5. Wrap-up#

Reporting Results#

Putting it all together we might write up our results like this:

We observed, a significant relationship between a person’s income and the average balance on their credit cards F(1, 389) = 108.99, p < .001, r = .463.

With each additional \(1000 of income, a person's average balance is predicted to increase by \)6.05 [4.91 7.19]

sns.lmplot(data=df, x='Income', y='Balance')

<seaborn.axisgrid.FacetGrid at 0x302945110>

Summary#

In this notebook we met statsmodels which allowed us to much more easily estimate univariate regression models using ols.

We also learned how to evaluation a model by inspecting its residuals and fitted values using seaborn.

Finally we demonstrated how we can test hypotheses by comparing modes to each other.

And how parameter inference (whether or not a parameter is statistically different from 0) is equivalent to comparing 2 models with and without the parameter.

Here’s a list of basic steps you may want to keep in mind as we move forward with multiple regression and categorical predictors later this week:

Define a model using

ols()and a formulaEstimate a model

.fit()and save the results to a variableInspect attributes of the saved results and use

seabornto plot them and evaluate model assumptionsFormulate hypotheses as nested-model comparisons between a compact and augmented model and use

anova_lm()to compare themInspect parameter inferences after model selection using

.summary()

Challenge#

Use the same DataFrame of credit-card scores to estimate and interpret the relationship between a person’s Age and their Balance.

We’ve reloaded it for you below:

df = pl.read_csv('./data/credit.csv')

df.head()

| Index | Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance |

|---|---|---|---|---|---|---|---|---|---|---|---|

| i64 | f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 |

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | "Male" | "No" | "Yes" | "Caucasian" | 333 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | "Female" | "Yes" | "Yes" | "Asian" | 903 |

| 3 | 104.593 | 7075 | 514 | 4 | 71 | 11 | "Male" | "No" | "No" | "Asian" | 580 |

| 4 | 148.924 | 9504 | 681 | 3 | 36 | 11 | "Female" | "No" | "No" | "Asian" | 964 |

| 5 | 55.882 | 4897 | 357 | 2 | 68 | 16 | "Male" | "No" | "Yes" | "Caucasian" | 331 |

1) Visually explore the data#

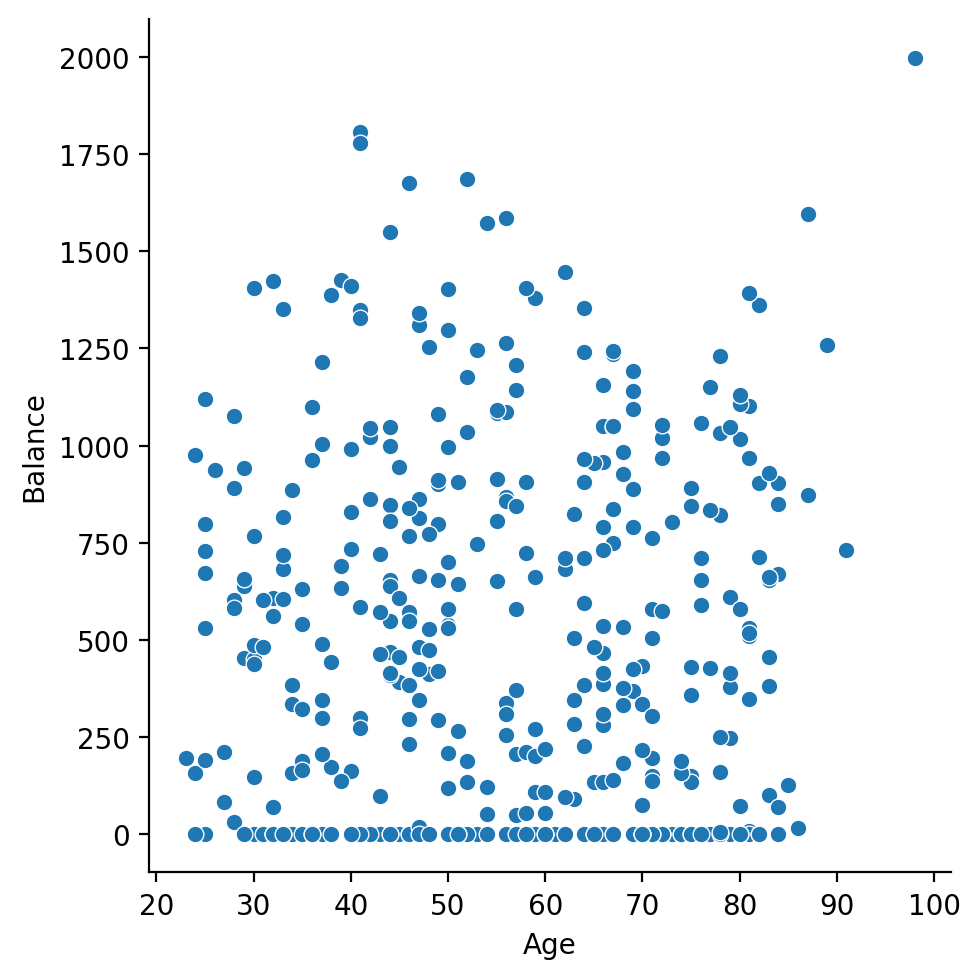

Does anything seem strange about the values?

# Your code here

sns.relplot(

data=df,

x='Age',

y='Balance'

)

<seaborn.axisgrid.FacetGrid at 0x302c08710>

2) Estimate a univariate regression#

Use the statsmodels to estimate a simple univariate regression model that captures:

# Your code here

model = ols('Balance ~ Age', data=df.to_pandas())

results = model.fit()

3) Evaluate the model#

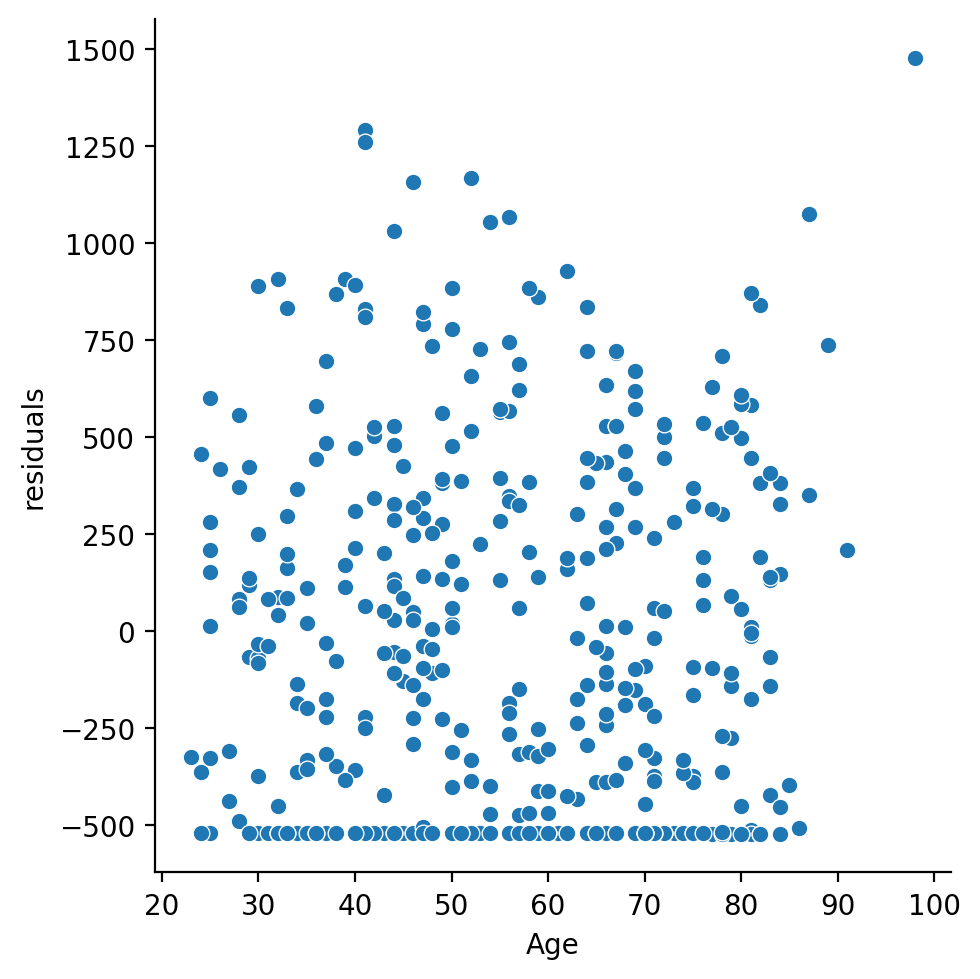

Make some figures of the residuals and write a sentence or two describing them and what concerns you have if any

# Your code here

df = df.with_columns(

residuals = results.resid.to_numpy()

)

sns.histplot(data=df, x='residuals')

<Axes: xlabel='residuals', ylabel='Count'>

sns.relplot(

data=df,

kind='scatter',

x='Age',

y='residuals'

)

<seaborn.axisgrid.FacetGrid at 0x302d66290>

4) Test the hypothesis#

Test the hypothesis that Age is statistically significant predictor of Balance using model comparison.

# Your code here

from statsmodels.stats.anova import anova_lm

compact_model = ols('Balance ~ 1', data=df.to_pandas())

compact_results = compact_model.fit()

anova_lm(compact_results, results)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 399.0 | 8.433991e+07 | 0.0 | NaN | NaN | NaN |

| 1 | 398.0 | 8.433963e+07 | 1.0 | 284.028251 | 0.00134 | 0.970814 |

5) Inspect the model summary#

Use .summary() to inspect the model summary. How does the output relate to your model comparison in the previous step?

# Your code here

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.000

Model: OLS Adj. R-squared: -0.003

Method: Least Squares F-statistic: 0.001340

Date: Wed, 12 Feb 2025 Prob (F-statistic): 0.971

Time: 16:47:39 Log-Likelihood: -3019.4

No. Observations: 400 AIC: 6043.

Df Residuals: 398 BIC: 6051.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 517.2922 77.852 6.645 0.000 364.241 670.344

Age 0.0489 1.336 0.037 0.971 -2.578 2.675

==============================================================================

Omnibus: 28.715 Durbin-Watson: 1.945

Prob(Omnibus): 0.000 Jarque-Bera (JB): 27.393

Skew: 0.582 Prob(JB): 1.13e-06

Kurtosis: 2.463 Cond. No. 197.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.