Models V: Categorical Predictors (2-levels)#

So far we’ve been using ols to perform univariate and multiple regression with continuous predictor variables. But often you’ll also be working with categorical predictor variables. In this notebook we’ll discuss how to build models using:

a categorical variable with 2 levels

a categorical variable with 2 levels + a continuous variable

a categorical variable with 2 levels, a continuous variable, and an interaction term

Slides for reference#

Data#

Let’s return to the credit card dataset we used in Notebook 02_models

This is a smaller version of that dataset with observations from 76 different people with the following columns:

Variable |

Description |

|---|---|

Income |

in thousand dollars |

Limit |

credit limit |

Rating |

credit rating |

Cards |

number of credit cards |

Age |

in years |

Education |

years of education |

Gender |

male or female |

Student |

student or not |

Married |

married or not |

Ethnicity |

African American, Asian, Caucasian |

Balance |

average credit card debt |

import numpy as np

import polars as pl

from polars import col

import seaborn as sns

import matplotlib.pyplot as plt

from statsmodels.formula.api import ols

from statsmodels.stats.anova import anova_lm

# Load data

df = pl.read_csv('./data/credit-mini.csv')

df

| Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance |

|---|---|---|---|---|---|---|---|---|---|---|

| f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 |

| 20.918 | 1233 | 128 | 3 | 47 | 18 | "Female" | "Yes" | "Yes" | "Asian" | 16 |

| 10.842 | 4391 | 358 | 5 | 37 | 10 | "Female" | "Yes" | "Yes" | "Caucasian" | 1216 |

| 29.705 | 3351 | 262 | 5 | 71 | 14 | "Female" | "No" | "Yes" | "Asian" | 148 |

| 76.348 | 4697 | 344 | 4 | 60 | 18 | "Male" | "No" | "No" | "Asian" | 108 |

| 30.622 | 3293 | 251 | 1 | 68 | 16 | "Male" | "Yes" | "No" | "Caucasian" | 532 |

| … | … | … | … | … | … | … | … | … | … | … |

| 107.841 | 10384 | 728 | 3 | 87 | 7 | "Male" | "No" | "No" | "African American" | 1597 |

| 27.47 | 2820 | 219 | 1 | 32 | 11 | "Female" | "No" | "Yes" | "Asian" | 0 |

| 15.741 | 4788 | 360 | 1 | 39 | 14 | "Male" | "No" | "Yes" | "Asian" | 689 |

| 16.751 | 4706 | 353 | 6 | 48 | 14 | "Male" | "Yes" | "No" | "Asian" | 1255 |

| 14.084 | 855 | 120 | 5 | 46 | 17 | "Female" | "No" | "Yes" | "African American" | 0 |

Categorical Predictor w/ 2 levels#

Let’s use ols to explore the example discussed in class in more detail: do students have a different balance than non-students?

We’ll fit 2 models:

a compact model that only includes the intercept

an augmented model that includes a categorical predictor for

Studentwhich has 2 levels (YesandNo)

We can tell ols to treat a variable as categorical by wrapping it in C()

Then we’ll test whether it’s worth it to add Student as a predictor to the model by comparing them like we have before:

# Compact Model

c_model = ols('Balance ~ 1', data=df.to_pandas())

c_results = c_model.fit()

# Augmented Model

# Treat "Student" as a categorical variable

a_model = ols('Balance ~ C(Student)', data=df.to_pandas())

a_results = a_model.fit()

# Compare models - worth it?

anova_lm(c_results, a_results)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 75.0 | 2.028075e+07 | 0.0 | NaN | NaN | NaN |

| 1 | 74.0 | 1.721872e+07 | 1.0 | 3.062040e+06 | 13.159573 | 0.000523 |

It’s worth it!

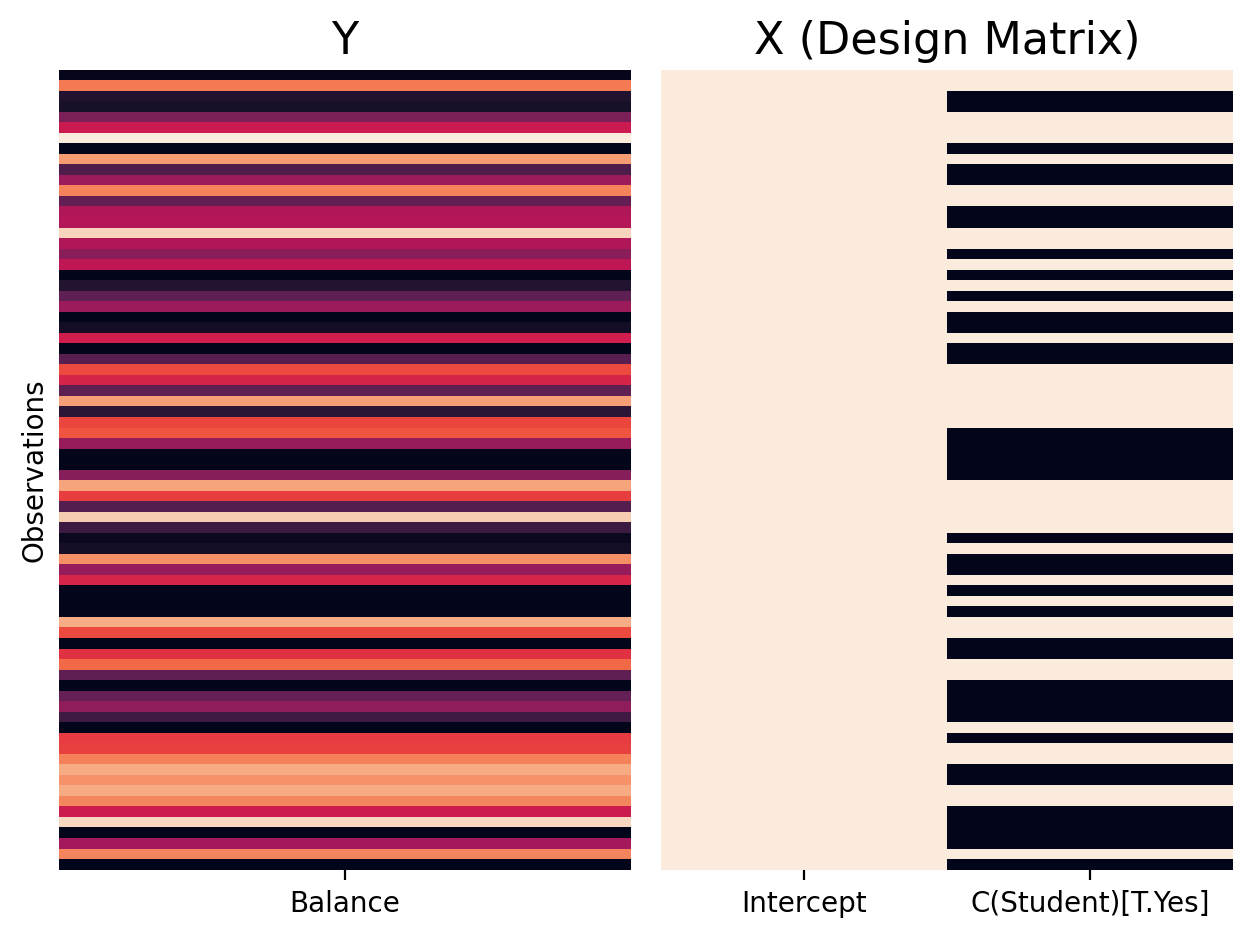

Let’s inspect our augmented model’s design matrix to try to understand how ols is representing our categorical variable Student

# First 6 rows

a_model.exog[:5, :]

array([[1., 1.],

[1., 1.],

[1., 0.],

[1., 0.],

[1., 1.]])

If we look at our DataFrame, we can see that by default C() has converted: No = 0 and Yes = 1

df.select('Balance', 'Student').head()

| Balance | Student |

|---|---|

| i64 | str |

| 16 | "Yes" |

| 1216 | "Yes" |

| 148 | "No" |

| 108 | "No" |

| 532 | "Yes" |

Sometimes it’s helpful to see the entire design matrix, especially as we move onto categorical variables with more than 2 levels in future notebooks.

We’ve provided a helper function you can use that takes a model as input. You can see each observation plotted alongside how we’ve encoded Student in the design matrix (beige = 1; black = 0):

from helpers import plot_design_matrix

plot_design_matrix(a_model)

Let’s inspect the .summary() to look at the parameter estimates for the model Intercept and C(Student)[T.Yes]

What do the intercept \(\hat{\beta}_0\) and slope \(\hat{\beta}_1\) here represent?

To answer this question we need to understand what it means to think about levels of a category in terms of the slopes of lines that we can estimate. And how the 0s and 1s in the design matrix relate to this…

# slim=True just removes some extra information we don't currently need to save space

print(a_results.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.151

Model: OLS Adj. R-squared: 0.140

No. Observations: 76 F-statistic: 13.16

Covariance Type: nonrobust Prob (F-statistic): 0.000523

=====================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------

Intercept 463.2368 78.252 5.920 0.000 307.317 619.156

C(Student)[T.Yes] 401.4474 110.664 3.628 0.001 180.944 621.951

=====================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Introduction to Categorical Coding Schemes#

Let’s think about about what it means to calculate a slope between 2 levels of a categorical variable.

We typically define the slope as the “change in y for 1-unit change in x” - this makes sense when both variables are continuous - e.g. how much a person’s Balance (y) increases for every additional year they’re alive Age (x).

But what is a “unit change in x” if x is a categorical variable like Student?

Its the difference between going from the mean of first level No to the mean of the second level Yes!

The mean difference is the regression slope \(\hat{\beta_1}\)

Treatment (Dummy) Coding#

While there are actually many ways to encode a categorical variable as columns of our design matrix, this intuitive idea is the default in both Python and R and is called treatment (dummy) coding.

It uses the intercept to estimate the mean of one of the levels of your categorical variable as a reference level, and encodes the other levels as mean differences from that reference level.

In the case of a variable with just 2 levels - this is just the mean difference between both levels, i.e. between Student=No and Student=Yes

# Get mean balance for each level separately

student_yes = df.filter(col('Student')=='Yes').select('Balance').mean()[0,0]

student_no = df.filter(col('Student')=='No').select('Balance').mean()[0,0]

print(f'Student: Yes = {student_yes:.3f}, No = {student_no:.3f}')

print(f"Mean Difference (Yes - No) = {student_yes - student_no:.5f}")

Student: Yes = 864.684, No = 463.237

Mean Difference (Yes - No) = 401.44737

# beta 0 = mean of No

# beta 1 = mean difference

a_results.params

Intercept 463.236842

C(Student)[T.Yes] 401.447368

dtype: float64

To make this more concrete, let’s add a new column to our DataFrame called Student_Dummy that represents Student just like our design matrix does:

Challenge#

Use when and lit that we’ve imported for you below to create a new column in df called Student_Dummy that encodes Yes = 1 and No = 0 for the Student variable.

Hint: You can use .alias() at the end of your when statement to give your new column a name.

from polars import when, lit

# Solution

df = df.with_columns(

when(col('Student') == 'Yes')

.then(lit(1))

.otherwise(lit(0))

.alias('Student_Dummy')

)

df.head()

| Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | Student_Dummy |

|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | i64 | i64 | i64 | i64 | i64 | str | str | str | str | i64 | i32 |

| 20.918 | 1233 | 128 | 3 | 47 | 18 | "Female" | "Yes" | "Yes" | "Asian" | 16 | 1 |

| 10.842 | 4391 | 358 | 5 | 37 | 10 | "Female" | "Yes" | "Yes" | "Caucasian" | 1216 | 1 |

| 29.705 | 3351 | 262 | 5 | 71 | 14 | "Female" | "No" | "Yes" | "Asian" | 148 | 0 |

| 76.348 | 4697 | 344 | 4 | 60 | 18 | "Male" | "No" | "No" | "Asian" | 108 | 0 |

| 30.622 | 3293 | 251 | 1 | 68 | 16 | "Male" | "Yes" | "No" | "Caucasian" | 532 | 1 |

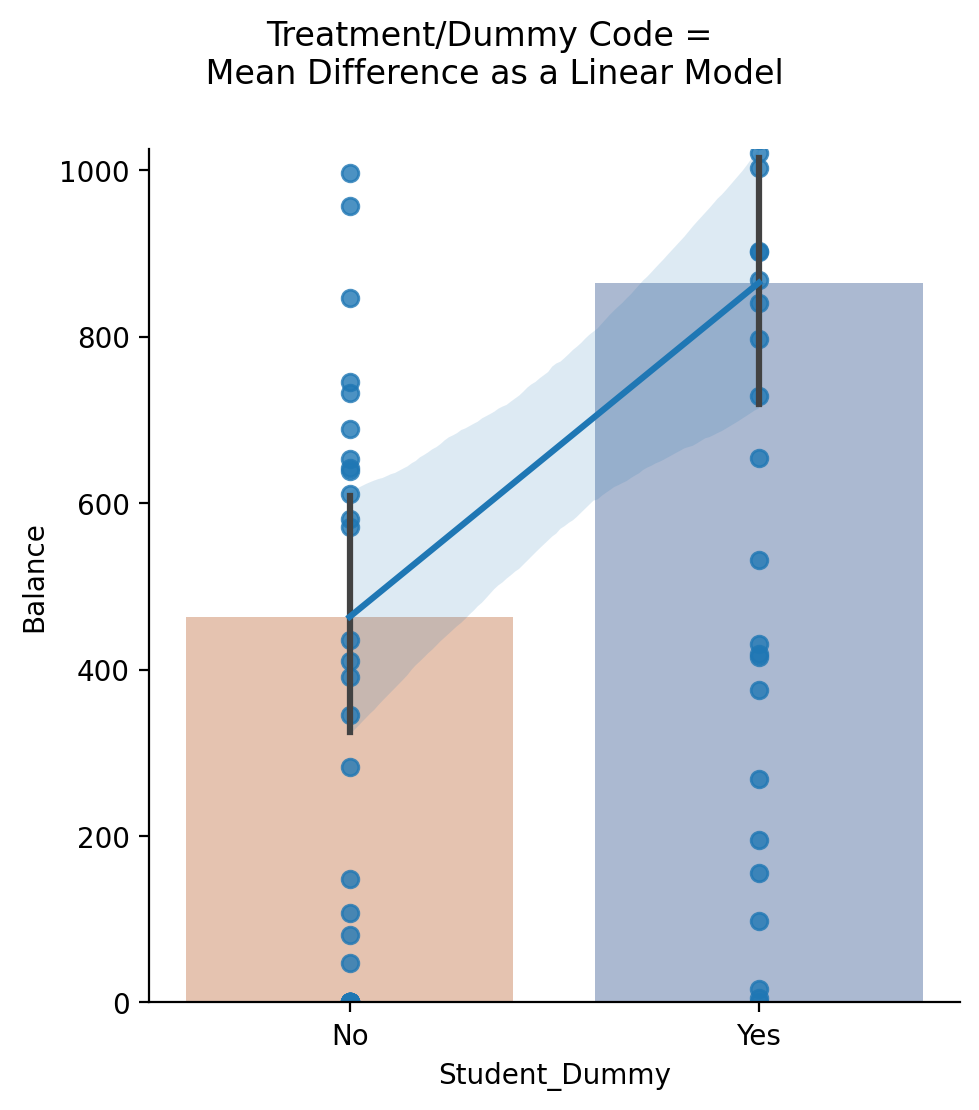

Let’s use the new column you made to create a figure and build our intuitions visually.

First, we’ll use sns.barplot to show the mean Balance of each level of Student

Then, we’ll ask sns.regplot to estimate and plot a regression line between our Student_Dummy and Balance variables; seaborn uses ols behind-the-scenes to do this!

You’ll see below that the slope of sns.regplot going from 0 to 1 is the same as the difference between bars

x_order = ['No', 'Yes']

# Create grid

grid = sns.FacetGrid(data=df.to_pandas(),height=5) ;

# Add a barpplot; we use map_dataframe so we can control hue separately for this layer

grid.map_dataframe(sns.barplot, 'Student', 'Balance', hue='Student',palette='deep', order=x_order, alpha=.5);

# Add a regression using our new column

grid.map_dataframe(sns.regplot, 'Student_Dummy', 'Balance')

# Aesthetics

grid.set(ylim=(0,1025));

grid.figure.suptitle("Treatment/Dummy Code =\n Mean Difference as a Linear Model", y=1.1);

We can also see this by estimating a new model using our newly created column Student_Dummy as a predictor and comparing its output to our original augmented model:

dummy_model = ols('Balance ~ Student_Dummy', data=df.to_pandas())

dummy_results = dummy_model.fit()

dummy_results.params

Intercept 463.236842

Student_Dummy 401.447368

dtype: float64

a_results.params

Intercept 463.236842

C(Student)[T.Yes] 401.447368

dtype: float64

Interpreting parameter estimates#

In our model our parameters represent:

\(\hat{\beta_0} = StudentNo_{mean}\) (reference level)

\(\hat{\beta_1} = StudentYes_{mean} - StudentNo_{mean}\)

By default ols will use alphabetically sort the levels of your categorical predictor and use the first one as the reference level. In our case this is No as as N comes before Y alphabetically.

But we can be more explicit and even control what group is the reference category. Let’s switch it to Student = Yes

We can do this by passing a second argument to C() in addition to our column name. We can use Treatment(reference='category_level') to tell ols that the reference category is Yes

# Set the reference group (intercept) to 'Yes'

ref_yes = ols("Balance ~ C(Student, Treatment(reference='Yes'))", data=df.to_pandas())

print(ref_yes.fit().summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.151

Model: OLS Adj. R-squared: 0.140

No. Observations: 76 F-statistic: 13.16

Covariance Type: nonrobust Prob (F-statistic): 0.000523

================================================================================================================

coef std err t P>|t| [0.025 0.975]

----------------------------------------------------------------------------------------------------------------

Intercept 864.6842 78.252 11.050 0.000 708.765 1020.604

C(Student, Treatment(reference='Yes'))[T.No] -401.4474 110.664 -3.628 0.001 -621.951 -180.944

================================================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Now the intercept is the mean of Student = Yes and the slope is No - Yes

student_yes

864.6842105263158

student_no - student_yes

-401.44736842105266

Inspecting the design matrix we can see that the coding has simply been flipped from our augmented model above:

# No = 1

# Yes = 0

ref_yes.exog[:5, :]

array([[1., 0.],

[1., 0.],

[1., 1.],

[1., 1.],

[1., 0.]])

# Originally we had

# No = 0

# Yes = 1

a_model.exog[:5, :]

array([[1., 1.],

[1., 1.],

[1., 0.],

[1., 0.],

[1., 1.]])

And just to confirm, we can see that the t-statistic and p-value that ols gives us is that same as running an independent t-test using scipy:

from scipy.stats import ttest_ind

results = ttest_ind(

df.filter(col('Student') == 'No').select('Balance').to_numpy(),

df.filter(col('Student') == 'Yes').select('Balance').to_numpy())

print(f"Independent samples t-test t({results.df[0]}) = {results.statistic[0]:.3f}, p = {results.pvalue[0]:.5f}")

Independent samples t-test t(74.0) = -3.628, p = 0.00052

Or in APA style:

print(f"Independent samples t-test t({results.df[0]}) = {results.statistic[0]:.3f}, p < .001")

Independent samples t-test t(74.0) = -3.628, p < .001

Categorical (2-level) and Continuous Predictors#

In the previous notebook 02_models we saw that Income was also a meaningful predictor of Balance:

grid = sns.lmplot(data=df, x='Income', y='Balance')

Let’s expand our model to account for this relationship when looking at the difference between Students and non-Students.

Specifically let’s estimate a multiple regression that asks: do students have difference Balances than non-students when accounting for Income?

We’ll also estimate another univariate regression that only looks at the relationship between Balance and Income:

Challenge#

Estimate the two models above

Use

anova_lmto compare both models. Is the multiple regression worth it?Use

anova_lmto compare the multiple regression toa_results, your original augmented model (univariate with onlyStudentas a predictor). Is the multiple regression worth it?Create a new dataframe called

df_modelsthat includes the following columns:

Balancethe original balance variableStudentthe original student variableIncomethe original income variablebalance_pred_sithe.fittedvaluesattribute of the multiple regressionresid_sithe.residattribute of the multiple regressionbalance_pred_ithe.fittedvaluesattribute of the univariate regressionresid_ithe.residattribute of the univariate regressionbalance_pred_sthe.fittedvaluesfrom the univariatea_resultswe estimated aboveresid_sthe.residfrom the univariatea_resultswe estimated above

# Solution

# Student only

s_model = ols('Balance ~ C(Student)', data=df.to_pandas())

s_results = s_model.fit()

# Income only

i_model = ols('Balance ~ Income', data=df.to_pandas())

i_results = i_model.fit()

# Student + Income

si_model = ols('Balance ~ C(Student) + Income', data=df.to_pandas())

si_results = si_model.fit()

# S+I vs S

anova_lm(s_results, si_results)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 74.0 | 1.721872e+07 | 0.0 | NaN | NaN | NaN |

| 1 | 73.0 | 1.374135e+07 | 1.0 | 3.477369e+06 | 18.473293 | 0.000052 |

# S+I vs I

anova_lm(i_results, si_results)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 74.0 | 1.685200e+07 | 0.0 | NaN | NaN | NaN |

| 1 | 73.0 | 1.374135e+07 | 1.0 | 3.110658e+06 | 16.525165 | 0.00012 |

# Solution

df_models = df.select(

col('Balance'),

col('Student'),

col('Income'),

balance_pred_si = si_results.fittedvalues.to_numpy(),

resid_si = si_results.resid.to_numpy(),

balance_pred_i = i_results.fittedvalues.to_numpy(),

resid_i = i_results.resid.to_numpy(),

balance_pred_s = a_results.fittedvalues.to_numpy(),

resid_s = a_results.resid.to_numpy(),

)

df_models.head()

| Balance | Student | Income | balance_pred_si | resid_si | balance_pred_i | resid_i | balance_pred_s | resid_s |

|---|---|---|---|---|---|---|---|---|

| i64 | str | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 16 | "Yes" | 20.918 | 727.826282 | -711.826282 | 526.484832 | -510.484832 | 864.684211 | -848.684211 |

| 1216 | "Yes" | 10.842 | 672.269098 | 543.730902 | 471.318923 | 744.681077 | 864.684211 | 351.315789 |

| 148 | "No" | 29.705 | 371.643114 | -223.643114 | 574.593491 | -426.593491 | 463.236842 | -315.236842 |

| 108 | "No" | 76.348 | 628.823915 | -520.823915 | 829.963033 | -721.963033 | 463.236842 | -355.236842 |

| 532 | "Yes" | 30.622 | 781.332328 | -249.332328 | 579.614049 | -47.614049 | 864.684211 | -332.684211 |

Interpreting Parameter Estimates#

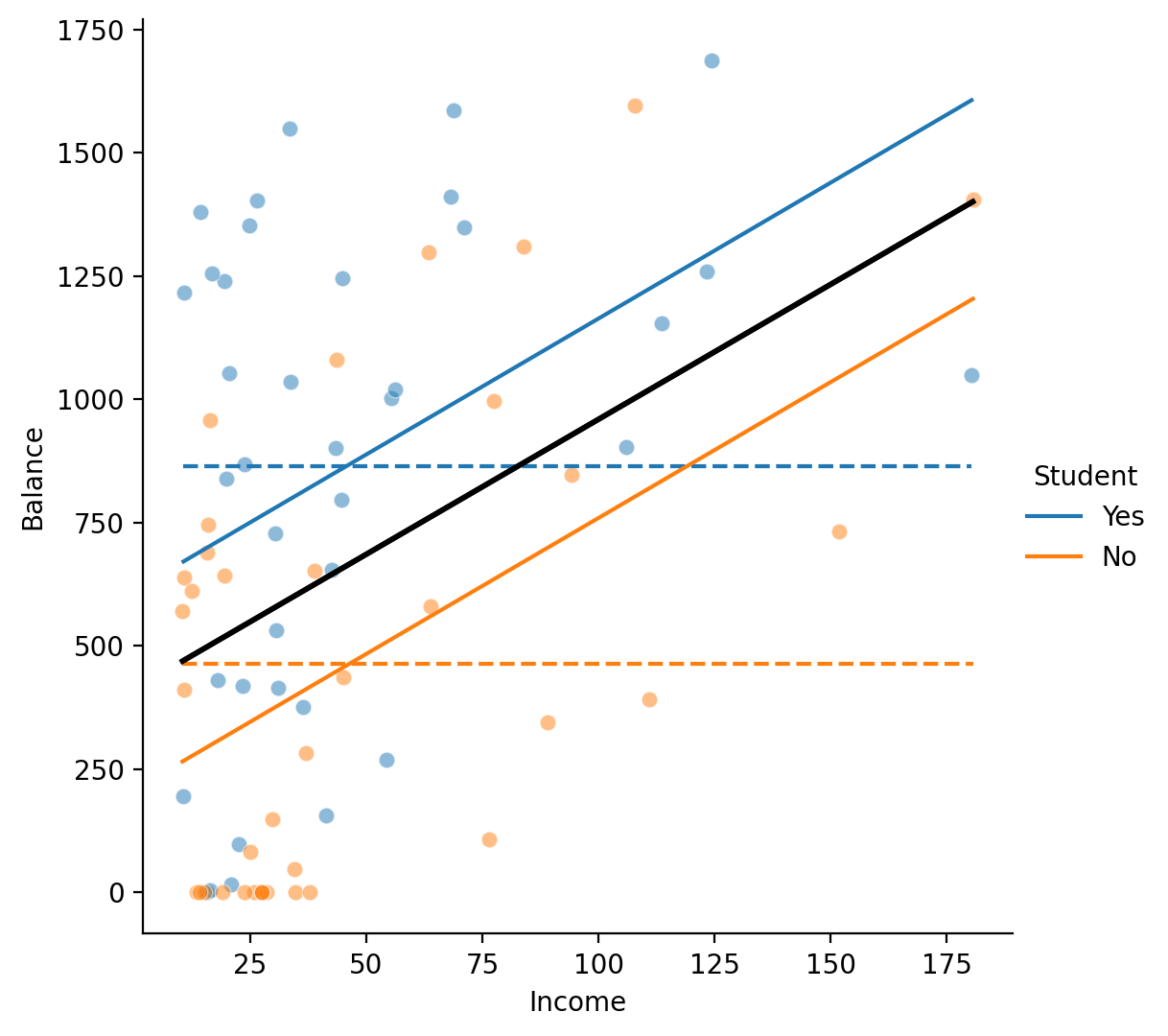

Now that we know the multiple regression is worth it, let’s interpret the parameter estimates.

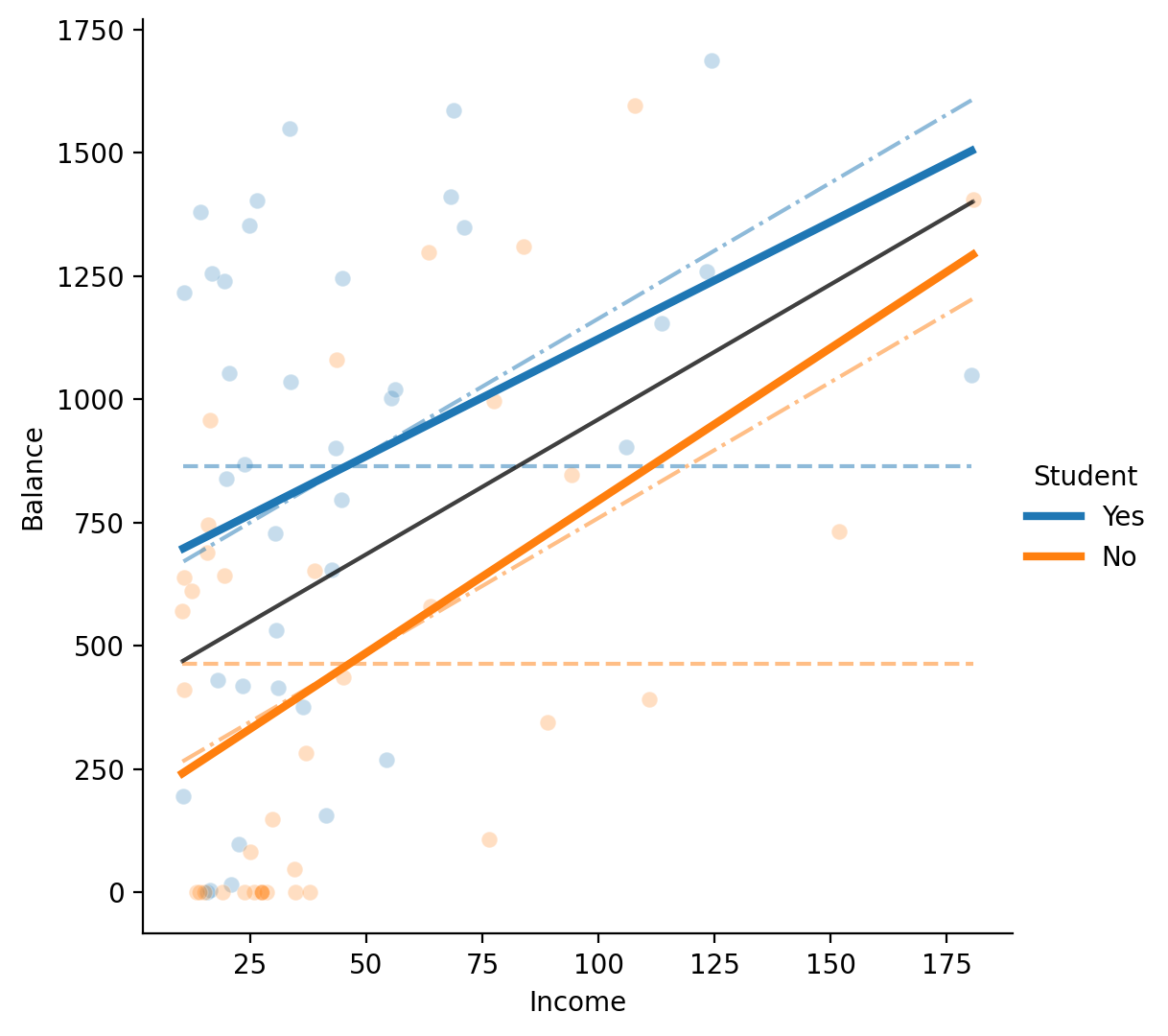

Let’s build some visual intuitions by plotting the predictions from the multiple regression and each separate univariate regression to see what’s changing. In the figure below:

The scatterplot points represent the raw data separated by the levels of

StudentIn solid black line is the relationshion between

IncomeandBalanceif we ignoreStudentThe dashed colored lines represent the relationship between

BalanceandStudentif we ignoreIncomeThe solid colored lines represent the relationship between

BalanceandIncomeif we account for difference in the intercepts for each level ofStudent

# Create grid

grid = sns.FacetGrid(data=df_models.to_pandas(), hue="Student", height=5.5, aspect=1);

# Plot data

grid.map(sns.scatterplot, "Income", "Balance",alpha=.5);

# Plot our predictions from student only model

grid.map(sns.lineplot, "Income", "balance_pred_s", ls='--');

# Plot our predictions from income only model

grid.map(sns.lineplot, "Income", "balance_pred_i", ls='-', color='black', lw=2);

# Plot our predictions student + income

grid.map(sns.lineplot, "Income", "balance_pred_si");

# Aesthetics

grid.set(ylabel='Balance');

grid.add_legend();

Let’s take a look at the parameter estimates…

si_results.params

Intercept 207.855285

C(Student)[T.Yes] 404.633047

Income 5.513813

dtype: float64

\(\hat{\beta_0}\) is supposed to be the mean of Student = No…but its not

\(\hat{\beta_1}\) is supposed to be the mean difference between Student = Yes and Student = No…but its not

\(\hat{\beta_2}\) is supposed to be the slope of Income…but it doesn’t match our univariate regression i_results

Our model with just Student shows that the \(\hat{\beta}_0\) was the mean of Student = No

a_results.params

Intercept 463.236842

C(Student)[T.Yes] 401.447368

dtype: float64

And our model with just Income shows that the \(\hat{\beta}_1\) was the slope of Income

i_results.params

Intercept 411.959178

Income 5.474981

dtype: float64

What’s going on?

Remember what we learned in notebooks 02_models and 03_models:

In the GLM, we interpret each parameter estimate assuming other parameter estimates = 0

Because of this:

\(\hat{\beta_0}\) is the mean of Student = No when Income = 0

\(\hat{\beta_1}\) is the mean difference between Student = Yes and Student = No when Income = 0

\(\hat{\beta_2}\) is the slope of Income when Student = 0 (No)

Challenge#

Can you make the parameter estimates more interpretable using an approach we learned in class and demonstrated in 02_models? Think about how to change what value the regression “fixes” Income to from 0 to something more useful…

Fit a new more interpretable multiple regression called

si_interp_modelusingStudentandIncomeas predictors and save the results tosi_interp_resultsCompare your parameter estimates from

.summary()or.paramsto the estimates from the original multiple regression. What do you notice?

# Solution

si_interp_model = ols('Balance ~ C(Student) + center(Income)', data=df.to_pandas())

si_interp_results = si_interp_model.fit()

print(si_interp_results.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.322

Model: OLS Adj. R-squared: 0.304

No. Observations: 76 F-statistic: 17.37

Covariance Type: nonrobust Prob (F-statistic): 6.75e-07

=====================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------

Intercept 461.6440 70.383 6.559 0.000 321.371 601.917

C(Student)[T.Yes] 404.6330 99.538 4.065 0.000 206.254 603.012

center(Income) 5.5138 1.283 4.298 0.000 2.957 8.071

=====================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Visualizing intutions#

Hopefully you remembered that you can center a predictor to change what the fixed value is when intepreting other parameters. It doesn’t change the estimate for what you’re centering (Income), but it always changes the intercept and other categorical parameters!

Let’s visualize the effect of centering a predictor - we’ll annotate the same plot as earlier illustrating the shift in coefficient interpretation:

We’ll add a vertical line for

Income = mean(Income)and a horizontal line for the mean ofStudent = No- this is our model interceptThe vertical distance between this point and where it intersect the blue line is \(\beta_1\) - mean difference between Yes and No when Income is at its mean

# Create grid

grid = sns.FacetGrid(data=df_models.to_pandas(), hue="Student", height=4)

# Plot data

grid.map(sns.scatterplot, "Income", "Balance",alpha=.5)

# Plot our predictions student + income

grid.map(sns.lineplot, "Income", "balance_pred_si")

# Plot Income mean

grid.map(plt.axvline, x=df_models['Income'].mean(), color="black", ls='--');

# Plot mean for Student = 0

grid.map(plt.axhline, y=student_no, color="black", ls='--');

# Aesthetics

grid.set(ylabel='Balance');

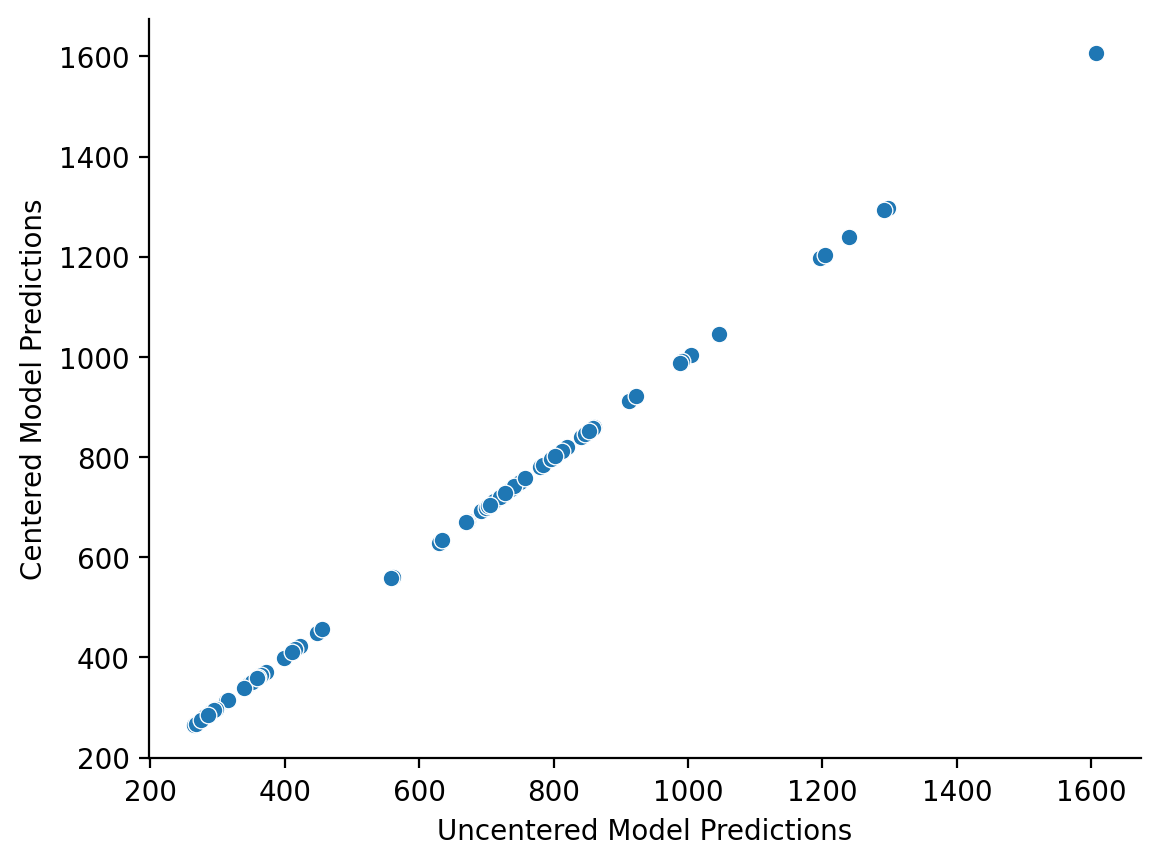

You’ll also notice that centering does not change model predictions. It only changes how we interpret the parameter estimates from our model

ax = sns.scatterplot(

x=si_results.fittedvalues, # predictions fro un-centered model

y=si_interp_results.fittedvalues, # predictions for centered model

)

ax.set(xlabel='Uncentered Model Predictions', ylabel='Centered Model Predictions');

sns.despine();

In notebook 03_models we learned that we can use .predict() to generate predictions from our model by fixing one or more of our predictors at certain values.

Let’s do that now to get our predicted estimates of the average Balance for each level of Student when Income is fixed at it’s mean of 46.03 - this is what our parameter estimate for Student is

# Create 1-row dataframes to pass into .predict()

student_no_x =pl.DataFrame({

'Income': df['Income'].mean(),

'Student': 'No'

})

student_yes_x =pl.DataFrame({

'Income': df['Income'].mean(),

'Student': 'Yes'

})

# Generate predictions

student_no_prediction = si_interp_results.predict(student_no_x.to_pandas())

student_yes_prediction = si_interp_results.predict(student_yes_x.to_pandas())

print(f"Student (No): {student_no:.3f}")

print(f"Student (Yes): {student_yes:.3f}")

print(f"Student (No prediction): {student_no_prediction[0]:.3f}")

print(f"Student (Yes prediction): {student_yes_prediction[0]:.3f}")

print(f"Student (Yes prediction - No prediction): {student_yes_prediction[0] - student_no_prediction[0]:.3f}")

Student (No): 463.237

Student (Yes): 864.684

Student (No prediction): 461.644

Student (Yes prediction): 866.277

Student (Yes prediction - No prediction): 404.633

And we can verify that:

\(\beta_0\) = \(\hat{balance}_{\text{student\_no}}\) when \(Income = Income_{mean}\)

\(\beta_1\) = \(\hat{balance}_{\text{student\_yes}}\) - \(\hat{balance}_{\text{student\_no}}\) when \(Income = Income_{mean}\)

si_interp_results.params

Intercept 461.644003

C(Student)[T.Yes] 404.633047

center(Income) 5.513813

dtype: float64

Summary#

When we add a categorical predictor to a model with a continuous predictor, we estimate different intercepts but the same slope for each level of the categorical variable.

Intuitively, this is like accounting for differences in the means of each group when considering the continuous relationship between two predictors.

Alternatively, we can think about it like accounting for the continuous relationship between another variable when considering the mean difference between groups.

Centering our continuous predictor makes our estimates more interpretable. It also makes sure we compare levels of our categorical predictor along a meaningful value of our continuous predictor!

Interactions (2-levels and Continuous Predictor)#

Our previous multiple regression tested whether students and non-students have a different Balance when accounting for the relationship between Balance and Income.

However, we did not test whether the relationship between Balance and Income was different for students and non-students

We can extend our previous model to test this by adding an interaction term to capture this relationship

Specifically we add Student x Income to our model to estimate separate slopes for students and non-students

Challenge#

Estimate the model above and call it

six_modeland save the results tosix_results.Compare it to

si_resultsfrom earlier usinganova_lm(). Is the addition of the interaction term worth it?Create 2 new columns in

df_modelscalledbalance_pred_sixandresid_sixthat include the.fittedvaluesand.residfrom this model

# Your code here

# Solution

six_model = ols('Balance ~ C(Student) * Income', data=df.to_pandas())

six_results = six_model.fit()

anova_lm(si_results, six_results)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 73.0 | 1.374135e+07 | 0.0 | NaN | NaN | NaN |

| 1 | 72.0 | 1.368314e+07 | 1.0 | 58201.972255 | 0.306256 | 0.581701 |

# Solution

df_models = df_models.with_columns(

balance_pred_six = six_results.fittedvalues.to_numpy(),

resid_six = six_results.resid.to_numpy(),

)

df_models.head()

| Balance | Student | Income | balance_pred_si | resid_si | balance_pred_i | resid_i | balance_pred_s | resid_s | balance_pred_six | resid_six |

|---|---|---|---|---|---|---|---|---|---|---|

| i64 | str | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 16 | "Yes" | 20.918 | 727.826282 | -711.826282 | 526.484832 | -510.484832 | 864.684211 | -848.684211 | 746.752889 | -730.752889 |

| 1216 | "Yes" | 10.842 | 672.269098 | 543.730902 | 471.318923 | 744.681077 | 864.684211 | 351.315789 | 698.87892 | 517.12108 |

| 148 | "No" | 29.705 | 371.643114 | -223.643114 | 574.593491 | -426.593491 | 463.236842 | -315.236842 | 360.557752 | -212.557752 |

| 108 | "No" | 76.348 | 628.823915 | -520.823915 | 829.963033 | -721.963033 | 463.236842 | -355.236842 | 648.864509 | -540.864509 |

| 532 | "Yes" | 30.622 | 781.332328 | -249.332328 | 579.614049 | -47.614049 | 864.684211 | -332.684211 | 792.859379 | -260.859379 |

Interpreting Parameter Estimates#

Let’s use the df_models you updated to update our previous figure to see what’s happening visually:

We’ve reduced the opacity of the previous models’ predictions and overlayed the interaction model’s predictions using solid colored lines.

As you can tell, now not only the intercepts are different for each level of Student, but the slopes are also different

# Create grid

grid = sns.FacetGrid(data=df_models.to_pandas(), hue="Student", height=5.5, aspect=1);

# Plot data

grid.map(sns.scatterplot, "Income", "Balance",alpha=.25);

# Plot our predictions from student only model

grid.map(sns.lineplot, "Income", "balance_pred_s", ls='--', alpha=.5);

# Plot our predictions from income only model

grid.map(sns.lineplot, "Income", "balance_pred_i", ls='-', color='black', lw=1.5, alpha=0.5);

# Plot our predictions student + income

grid.map(sns.lineplot, "Income", "balance_pred_si", ls='-.', alpha=.5);

# Plot our predictions student x income

grid.map(sns.lineplot, "Income", "balance_pred_six", lw=3);

# Aesthetics

grid.set(ylabel='Balance');

grid.add_legend();

Let’s inspect the parameter estimates

print(six_results.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.325

Model: OLS Adj. R-squared: 0.297

No. Observations: 76 F-statistic: 11.57

Covariance Type: nonrobust Prob (F-statistic): 2.82e-06

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

Intercept 176.9471 108.096 1.637 0.106 -38.539 392.434

C(Student)[T.Yes] 470.4184 155.351 3.028 0.003 160.732 780.105

Income 6.1811 1.765 3.502 0.001 2.662 9.700

C(Student)[T.Yes]:Income -1.4298 2.584 -0.553 0.582 -6.580 3.721

============================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Wait we forgot to center! Let’s do that now to make these estimates more interpretable:

six_model_cent = ols('Balance ~ C(Student) * center(Income)', data=df.to_pandas())

six_results_cent = six_model_cent.fit()

print(six_results_cent.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: Balance R-squared: 0.325

Model: OLS Adj. R-squared: 0.297

No. Observations: 76 F-statistic: 11.57

Covariance Type: nonrobust Prob (F-statistic): 2.82e-06

====================================================================================================

coef std err t P>|t| [0.025 0.975]

----------------------------------------------------------------------------------------------------

Intercept 461.4512 70.721 6.525 0.000 320.472 602.430

C(Student)[T.Yes] 404.6055 100.014 4.045 0.000 205.231 603.980

center(Income) 6.1811 1.765 3.502 0.001 2.662 9.700

C(Student)[T.Yes]:center(Income) -1.4298 2.584 -0.553 0.582 -6.580 3.721

====================================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Let’s verify that:

\(\beta_0\) = \(\hat{balance}_{\text{student\_no}}\) when \(Income = Income_{mean}\)

\(\beta_1\) = \(\hat{balance}_{\text{student\_yes}}\) - \(\hat{balance}_{\text{student\_no}}\) when \(Income = Income_{mean}\)

just like we did before by generating a single marginal prediction

# Create 1-row dataframes to pass into .predict()

student_no_x =pl.DataFrame({

'Income': df['Income'].mean(),

'Student': 'No'

})

student_yes_x =pl.DataFrame({

'Income': df['Income'].mean(),

'Student': 'Yes'

})

# Generate predictions

student_no_prediction = six_results.predict(student_no_x.to_pandas())

student_yes_prediction = six_results.predict(student_yes_x.to_pandas())

print(f"Student (No): {student_no:.3f}")

print(f"Student (Yes): {student_yes:.3f}")

print(f"Student (No prediction): {student_no_prediction[0]:.3f}")

print(f"Student (Yes prediction): {student_yes_prediction[0]:.3f}")

print(f"Student (Yes prediction - No prediction): {student_yes_prediction[0] - student_no_prediction[0]:.3f}")

Student (No): 463.237

Student (Yes): 864.684

Student (No prediction): 461.451

Student (Yes prediction): 866.057

Student (Yes prediction - No prediction): 404.606

six_results_cent.params

Intercept 461.451226

C(Student)[T.Yes] 404.605544

center(Income) 6.181137

C(Student)[T.Yes]:center(Income) -1.429850

dtype: float64

To verify that:

\(\beta_2\) = \(Balance \sim Income\) when \(Student =0\)

\(\beta_3\) = the difference between \(Balance \sim Income\) when \(Student =0\) vs \(Student = 1\)

we’ll use the same approach we did in 03_models - we’ll set Student = 0 and Student = 1 and provide the original values for Income to generate marginal predictions for Balance.

Then we’ll estimate the slope of the relationship between these marginal predictions and our original values of Income using 2 univariate regressions:

# Get only student = yes or student = No

student_0_data = df.filter(col('Student') == 'No').select(['Income', 'Student'])

student_1_data = df.filter(col('Student') == 'Yes').select(['Income', 'Student'])

# Use values to get model predictions for Balance separately for students and non-students

student_0_predictions = six_results.predict(student_0_data.to_pandas())

student_1_predictions = six_results.predict(student_1_data.to_pandas())

# Create a new dataframe of Predicted_Balance ~ Income when Student = No

marginal_data_student_0 = pl.DataFrame({

'Income': student_0_data['Income'].to_numpy(),

'Predicted_Balance': student_0_predictions.to_numpy()

})

# Run univariate OLS to slope

marginal_student_0_params = ols('Predicted_Balance ~ Income',

marginal_data_student_0.to_pandas()).fit().params

# Same for student = Yes

marginal_data_student_1 = pl.DataFrame({

'Income': student_1_data['Income'].to_numpy(),

'Predicted_Balance': student_1_predictions.to_numpy()

})

marginal_student_1_params = ols('Predicted_Balance ~ Income',

marginal_data_student_1.to_pandas()).fit().params

print(f"Income slope for Student = No (0): {marginal_student_0_params['Income']:.4f}")

print(f"Income slope for Student = Yes (1): {marginal_student_1_params['Income']:.4f}")

print(f"Difference in slopes: {marginal_student_1_params['Income'] - marginal_student_0_params['Income']:.4f}")

Income slope for Student = No (0): 6.1811

Income slope for Student = Yes (1): 4.7513

Difference in slopes: -1.4298

And we can see the interaction term reflects this difference-in-slopes while center(Income) reflects the slope of Student = No

six_results_cent.params

Intercept 461.451226

C(Student)[T.Yes] 404.605544

center(Income) 6.181137

C(Student)[T.Yes]:center(Income) -1.429850

dtype: float64

Summary#

When we multiply a categorical predictor in a model with a continuous predictor, we estimate different intercepts and different slopes for each level of the categorical variable.

Intuitively, this is like fitting a separate univariate regression to each level of the categorical variable and comparing the difference-in-slopes of both regressions.

Alternatively, we can think about it testing whether the mean difference between levels of our categorical variable increase or decrease as we move along the continuous predictor.

Centering our continuous predictor makes our estimates more interpretable. It also makes sure we compare levels of our categorical predictor along a meaningful value of our continuous predictor!

Challenge#

In the Parameter Interpretation section of 03_models we had you answer a response challenge about a model you built using the advertising dataset:

Specifically we said:

Notice in the plot above that the slopes of the predicted lines are not changing - it looks like only the intercept is shifting up or down. Can you provide an explanation why? What is our model failing to capture and how might we fix this?

Your tasks#

Using what you learned about interactions in multiple regression:

Estimate the model using the formula above (same as in

03_models)Estimate a new model that captures what this model is missing

Compare this new model to the original model to see if it’s worth it

Make a new figure like the one above that visualizes the predictions from your new model

Interpret the parameter estimates from

.summary()and provide a natural-language explanation of what they meanFit another like you just did, but this time center each predictor

How are the parameter estimates from this model different to the uncentered one?

Compare the correlations between predictors in the centered and uncentered models using the provided function

Variable |

Description |

|---|---|

tv |

TV ad spending in $1000 of dollars |

radio |

Radio ad spending in $1000 of dollars |

newspaper |

Newspaper ad spending in $1000 of dollars |

sales |

Sales generated in $1000 of dollars |

import numpy as np

import polars as pl

from polars import col

import seaborn as sns

import matplotlib.pyplot as plt

from statsmodels.formula.api import ols

df = pl.read_csv('./data/advertising.csv')

df.head()

| tv | radio | newspaper | sales |

|---|---|---|---|

| f64 | f64 | f64 | f64 |

| 230.1 | 37.8 | 69.2 | 22.1 |

| 44.5 | 39.3 | 45.1 | 10.4 |

| 17.2 | 45.9 | 69.3 | 9.3 |

| 151.5 | 41.3 | 58.5 | 18.5 |

| 180.8 | 10.8 | 58.4 | 12.9 |

1) Estimate model from previous notebook#

# Solution

model_c = ols('sales ~ tv + radio', data=df.to_pandas())

results_c = model_c.fit()

2) Estimate new model#

# Solution

model_a = ols('sales ~ tv + radio + tv:radio', data=df.to_pandas())

results_a = model_a.fit()

3) Compare both models#

# Solution

anova_lm(results_c, results_a)

| df_resid | ssr | df_diff | ss_diff | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| 0 | 197.0 | 556.913980 | 0.0 | NaN | NaN | NaN |

| 1 | 196.0 | 174.483383 | 1.0 | 382.430597 | 429.590463 | 2.757681e-51 |

4) Figure of model predictions#

# Solution

# Save to variable just to make coding easier

tv = df['tv'].to_numpy()

zeros = np.repeat(0, len(tv))

twenty = np.repeat(20, len(tv))

forty = np.repeat(40, len(tv))

# We use all values in the TV column

# And just a bunch of 0s for radio

y_radio_0 = results_a.predict({'tv': tv, 'radio': zeros, 'tv:radio':tv * zeros})

y_radio_20 = results_a.predict({'tv': tv, 'radio': twenty, 'tv:radio':tv * twenty})

y_radio_40 = results_a.predict({'tv': tv, 'radio': forty, 'tv:radio':tv * forty})

grid = sns.relplot(

data=df,

kind='scatter',

x='tv',

y='sales',

hue='radio',

size='radio',

)

grid.set(xlabel='TV Spending ($1000)', ylabel='Sales ($1000)');

grid.legend.set_title('Radio Spending ($1000)');

grid.legend.set_bbox_to_anchor((.45, .8));

# Add them to the plot

grid.ax.plot(tv, y_radio_0, color='gray');

grid.ax.plot(tv, y_radio_20, color='gray');

grid.ax.plot(tv, y_radio_40, color='gray');

5) Interpret parameter estimates#

# Solution

print(results_a.summary())

OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.968

Model: OLS Adj. R-squared: 0.967

Method: Least Squares F-statistic: 1963.

Date: Tue, 18 Feb 2025 Prob (F-statistic): 6.68e-146

Time: 16:12:39 Log-Likelihood: -270.14

No. Observations: 200 AIC: 548.3

Df Residuals: 196 BIC: 561.5

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 6.7502 0.248 27.233 0.000 6.261 7.239

tv 0.0191 0.002 12.699 0.000 0.016 0.022

radio 0.0289 0.009 3.241 0.001 0.011 0.046

tv:radio 0.0011 5.24e-05 20.727 0.000 0.001 0.001

==============================================================================

Omnibus: 128.132 Durbin-Watson: 2.224

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1183.719

Skew: -2.323 Prob(JB): 9.09e-258

Kurtosis: 13.975 Cond. No. 1.80e+04

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.8e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

6) Fit a model with centered predictors#

# Solution

model_a_cent = ols('sales ~ center(tv) * center(radio)', data=df.to_pandas())

results_a_cent = model_a_cent.fit()

print(results_a_cent.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.968

Model: OLS Adj. R-squared: 0.967

No. Observations: 200 F-statistic: 1963.

Covariance Type: nonrobust Prob (F-statistic): 6.68e-146

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

Intercept 13.9470 0.067 208.737 0.000 13.815 14.079

center(tv) 0.0444 0.001 56.673 0.000 0.043 0.046

center(radio) 0.1886 0.005 41.806 0.000 0.180 0.198

center(tv):center(radio) 0.0011 5.24e-05 20.727 0.000 0.001 0.001

============================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.28e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

7) How are the parameter estimates from centered and un-centered models the same or different?#

Uncentered predictor slopes assume other predictors = 0

Centered predictor slopes assume other predictors = their respective means

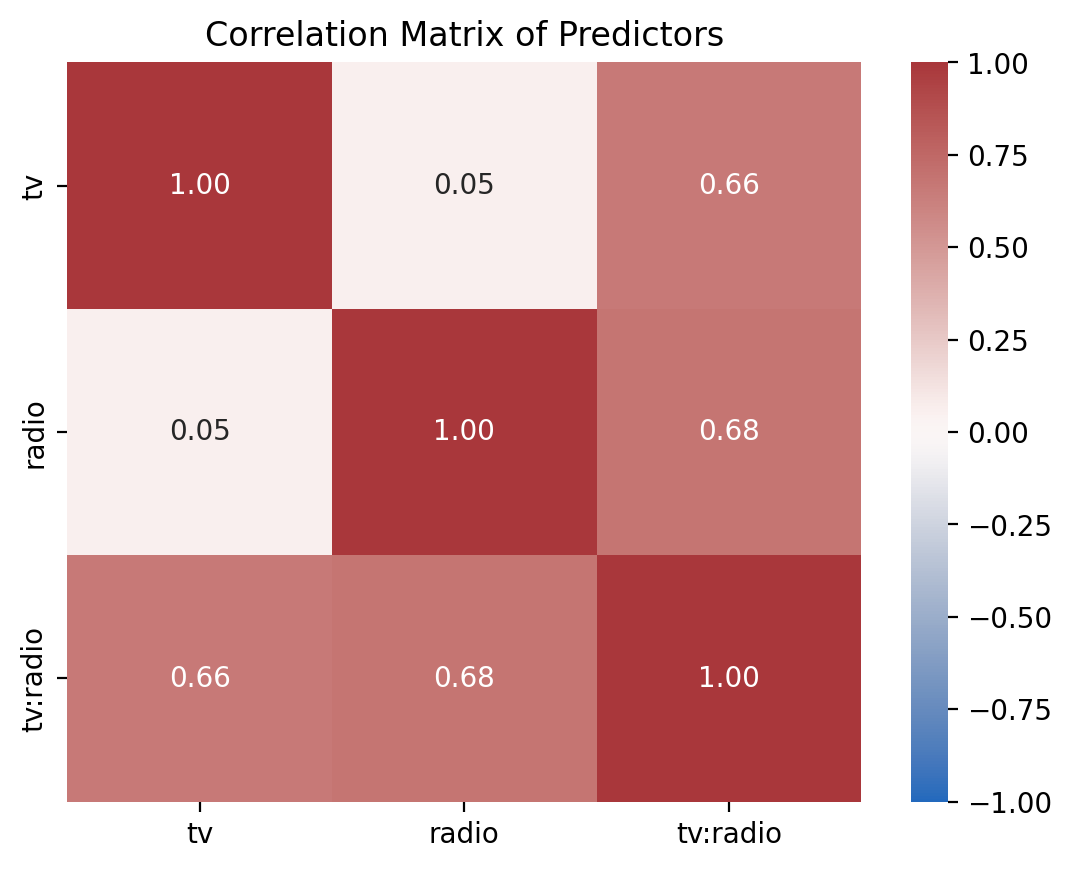

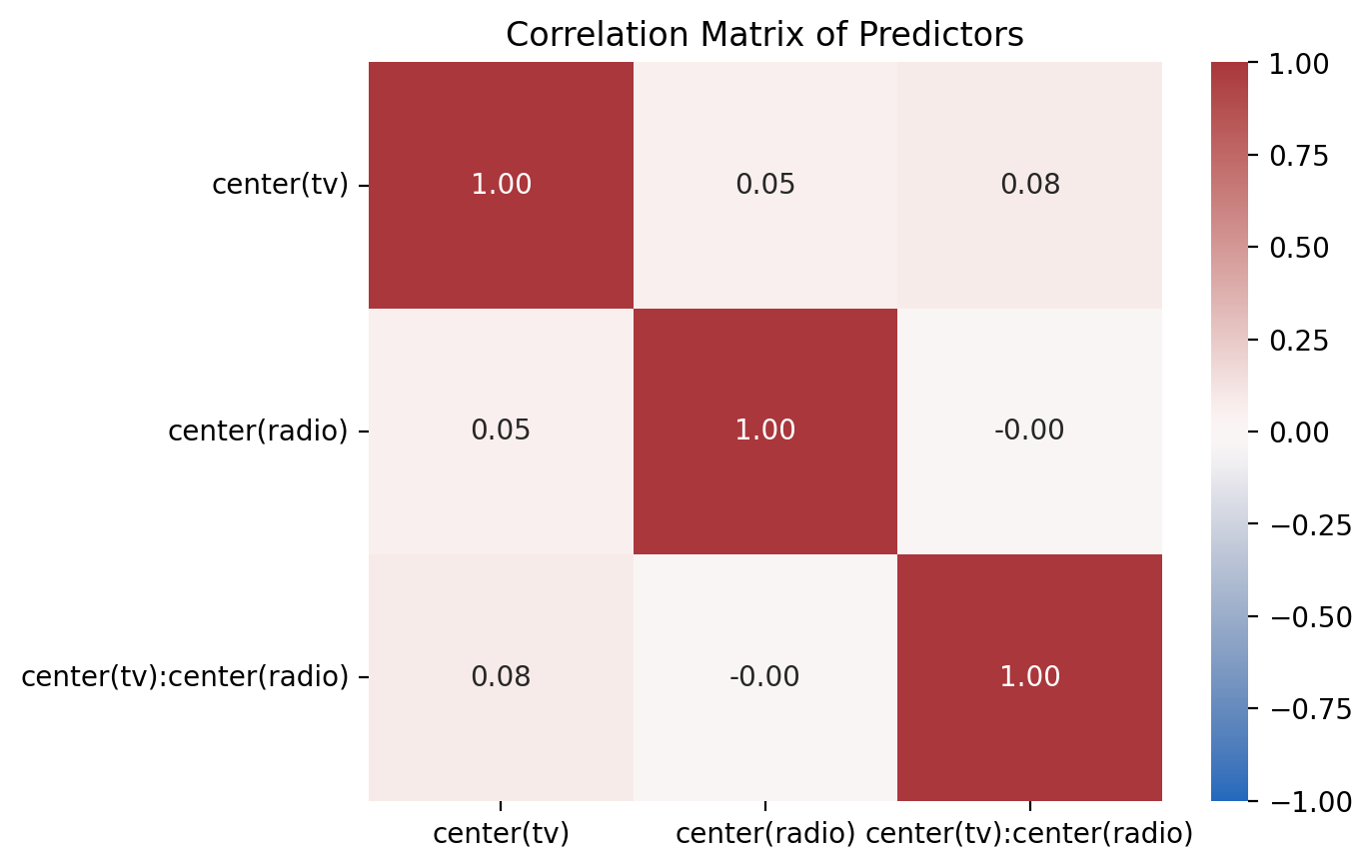

8) Compare the correlations between centered and un-centered models#

Use the provided function plot_predictor_correlations to visualize the correlation matrix of the predictors for both the centered and uncentered models.

Then answer the question below

from helpers import plot_predictor_correlations

# Example Usage

# plot_predictor_correlations(my_model)

# Solution

ax = plot_predictor_correlations(model_a)

# Solution

ax = plot_predictor_correlations(model_a_cent)

How do you think the change in correlation will affect our estimates and inferences?

Your response here