Models IV: Parameter Uncertainty & Inference#

Slides for reference#

Learning Goals#

At the end of the previous notebook we had you fit the following model:

In this notebook let’s examine this model in more detail to explore the following concepts that we discussed in class:

Understanding the uncertainty of our parameter estimates and the standard-error output of

.summary()Using bootstrapping to derive this uncertainty ourselves and calculate confidence intervals

Understanding the t statistic and p value

Using permutation to derive the null distribution ourselves

Your primary goal is build an intuition for how to properly make a statistical inference about your model parameters. Previously we discussed how we can make inferences about specific parameters by framing the question as a comparison between two models: is the addition of this parameter worth it given the proportional reduction in error?

Throughout this notebook we can consider a different framing: the signal-to-noise ratio of our estimation.

Remember that we’re looking to answer a question about something we don’t have direct access to: the population. We can only collect a sample and then try to reason about the population from an estimate we make using our sample. How do we do that reasoning? By quantifying our estimation uncertainty.

Conceptually, the “noise” or standard error, is a measure of the expected average deviation of the model’s parameter estimates \(\hat{\beta}\) from the “true value” of the parameter \(\beta\) in the population - the value we don’t have direct access to and want to make an inference about. We can do this by quantifying our (un)-certainty in that estimate given our sampling error \(var(e)\).

Data#

We’ll start by loading the same dataset as before and estimating the model using ols.

Variable |

Description |

|---|---|

tv |

TV ad spending in $1000 of dollars |

radio |

Radio ad spending in $1000 of dollars |

newspaper |

Newspaper ad spending in $1000 of dollars |

sales |

Sales generated in $1000 of dollars |

import numpy as np

import polars as pl

from polars import col

import seaborn as sns

import matplotlib.pyplot as plt

from statsmodels.formula.api import ols

df = pl.read_csv('./data/advertising.csv')

# Fit the model from the end of the last notebook

model = ols('sales ~ tv + radio + newspaper', data=df.to_pandas())

results = model.fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.897

Model: OLS Adj. R-squared: 0.896

Method: Least Squares F-statistic: 570.3

Date: Mon, 17 Feb 2025 Prob (F-statistic): 1.58e-96

Time: 15:51:09 Log-Likelihood: -386.18

No. Observations: 200 AIC: 780.4

Df Residuals: 196 BIC: 793.6

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 2.9389 0.312 9.422 0.000 2.324 3.554

tv 0.0458 0.001 32.809 0.000 0.043 0.049

radio 0.1885 0.009 21.893 0.000 0.172 0.206

newspaper -0.0010 0.006 -0.177 0.860 -0.013 0.011

==============================================================================

Omnibus: 60.414 Durbin-Watson: 2.084

Prob(Omnibus): 0.000 Jarque-Bera (JB): 151.241

Skew: -1.327 Prob(JB): 1.44e-33

Kurtosis: 6.332 Cond. No. 454.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Let’s explore the uncertainty associated with each parameter estimate.

In the summary output above these are called std err. We can get them like this:

# bse = "beta standard error"

results.bse

Intercept 0.311908

tv 0.001395

radio 0.008611

newspaper 0.005871

dtype: float64

Parametric Inference using analytic uncertainty estimation#

In class we discussed calculating an estimate of uncertainty based upon an analytic formula for the standard-error of our parameter estimates - this is what lm() in R or ols in Python will automatically calculate for you and what you see in the output of .summary().

In the context of the General Linear Model we represent this uncertainty as \(SE_{\hat{\beta}}\) and can calculate it using the part of the OLS formula that reflects the variance of each predictor, scaled by how wrong our model was overall:

Our uncertainty in \(\hat{\beta}\) is based on the variance of a predictor and the average error of the model:

This formula let’s us see exactly why “more data is better” - because it affects the precision of how well we can estimate our parameters! In general, our precision is approximately

The Central Limit Theorem tells us that we can assume the error of an estimate is inversely proportional to \(\sqrt{n}\). In other words, the larger \(n\), the more precisely we can estimate \(\hat{\beta}\), so the lower we expect \(SE_{\hat{\beta}}\) to be.

However, the process of estimation requires us to “fix” some of our parameters at certain values in order to estimate other parameters. For example, you can’t calculate a standard-deviation without first estimating the mean.

To take this into a account we use \(DF_{error}\) in the formula - how many data point are “left-over” or “free to vary” after our estimated parameters, e.g. mean, std, intercept, slopes, etc.

The more parameters we estimate, the fewer data points are left to freely vary, and the worse our precision is.

This is the connection to our previous approach of performing statistical inference via model comparison.

The reason why we compare models based on an accuracy-simplicity trade-off is because given the same dataset, the more parameters we estimate, the less data we have to estimate them with, and the less precise our estimates become.

It’s the bias-variance trade-off again!

Breaking it down#

Let’s understand what this formula means by calculating each piece one-at-a-time using Python.

We’ll start with \((X^TX)^{-1}\)

First, we’ll save our model’s design matrix to a new variable X.

Remember this is a matrix with the same number of columns as predictors in our model, plus an intercept

Model: \(\text{sales} \sim \text{tv + radio + newspaper}\)

Design matrix has 4 columns: \(intercept\), \(tv\), \(radio\), \(newspaper\)

X = model.exog

# print first three rows

X[:3, :]

array([[ 1. , 230.1, 37.8, 69.2],

[ 1. , 44.5, 39.3, 45.1],

[ 1. , 17.2, 45.9, 69.3]])

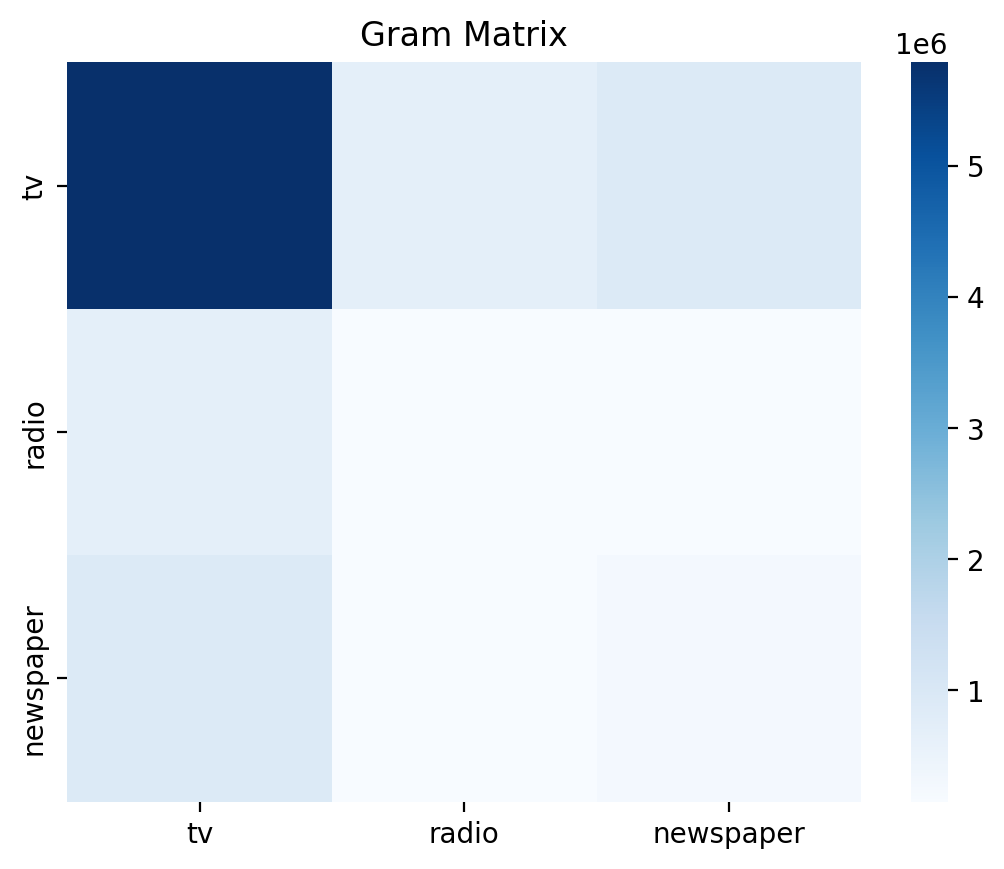

Gram Matrix \(X^TX\)#

Now let’s calculate \(X^TX\), also called the \(Gram\) matrix.

Whenever you see a matrix multiplied by its own transpose you should think: some kind of similarity matrix.

In this case the similarity is the dot-product betnwee each pair of predictor variables:

\(tv \& radio\)

\(tv \& newspaper\)

\(radio \& newspaper\)

We’ll visualize it using a seaborn heatmap, where darker colors represent higher similarity and we’ll ignore the \(intercept\) column which is always 1s.

Diagonal elements represent the un-scaled variance within each column of \(X\); the un-scaled variance of a single predictor (e.g. \(tv\)).

Off-diagonal elements represent the un-scaled co-variance between each pair of columns of \(X\); the un-scaled co-variance between pairs of predictors(e.g. \(tv\) and \(radio\)):

# short-hand for np.dot(X.T, X)

G = X.T @ X

# Predictor names for tick labels

labels = ['tv', 'radio','newspaper']

# Ignore first row and column which is intercept

ax = sns.heatmap(G[1:, 1:], cmap='Blues', xticklabels=labels, yticklabels=labels)

ax.set_title('Gram Matrix');

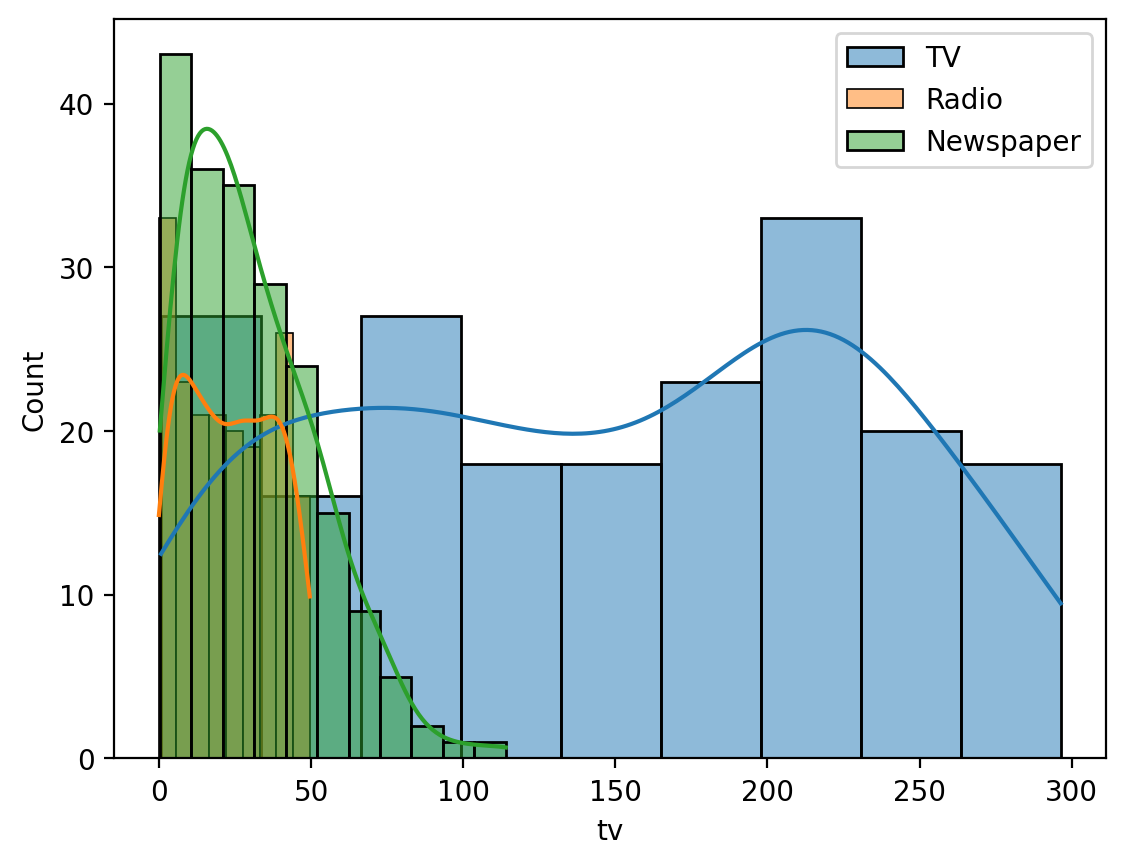

Hmm it looks like \(tv\) has a lot of variance compared to the other variables. Let’s plot them to understand what’s going on.

We’ll make a histogram of each variable just to see how spread out it is:

ax=sns.histplot(data=df, x='tv', kde=True, label='TV')

ax=sns.histplot(data=df, x='radio', kde=True, label='Radio')

ax=sns.histplot(data=df, x='newspaper', kde=True, label='Newspaper')

ax.legend();

Ah we can see that \(tv\) takes on many more values than either \(radio\) or \(newspaper\) - its distribution is much wider, hence the higher value and darker color in the heatmap above. We’ll revisit this later…

Residual variance \(\sigma^2\)#

To calculate the variance of the residuals we can use the .resid attribute of the results that ols calculates for us. Since it’s a numpy array of values we can call .var() to get the variance and use ddof=4 to account for the fact that we’re estimating 4 parameters - “consuming” 4 degrees of freedom

# Variance of the residuals accounting for 4 estimated params

results.resid.var(ddof=4)

np.float64(2.8409452188887094)

It turns out that ols already calculates this for us:

# Variance of residuals that statsmodels already stores it for us

results.scale

np.float64(2.8409452188887103)

which confirms how we calculated it above. ols also stores a .mse_resid which is the mean-squared-error of the residuals.

If you remember from class: average residual variance = average model error so it should be the same value

# Remember resid variance = average error, so MSE is the same thing!

results.mse_resid

np.float64(2.8409452188887103)

Calculating SE#

Ok we have all the pieces to lets calculate the formula:

First, we calculate what it takes to “undo” the similarity between predictors using the matrix inverse:

# Calculated above

# G = X^T * X

XTXinv = np.linalg.inv(G)

Then we grab just the diagonal values - because we specifically care about the variances of each predictor not the co-variances between predictors.

diag_inv = np.diag(XTXinv)

# 4 for 4 predictors

diag_inv.shape

(4,)

Then we multiply by our average error to get the \(\text{Var}(\beta)\)

beta_var = results.mse_resid * diag_inv

And take the square root to finally get \(SE_{\hat{\beta}} = \sqrt{\text{Var}(\hat{\beta})}\)

beta_se = np.sqrt(beta_var)

beta_se

array([0.31190824, 0.0013949 , 0.00861123, 0.00587101])

In one fell-swoop this looks like:

# Altogether

np.sqrt(np.diag(results.scale * np.linalg.inv(np.dot(X.T, X)))).round(6)

array([0.311908, 0.001395, 0.008611, 0.005871])

And we can confirm against the standard-errors that ols calculated for us:

np.allclose(

results.bse.to_numpy(), # <- ols calculation

beta_se # <- our calculation

)

True

Analytic p-value#

To make a statistical inference, we want to calculate the ratio between our signal, i.e. our estimate \(\hat{\beta}\) and our noise, i.e. our standard-error \(SE_{\hat{\beta}}\).

The larger the \(t\) the more confidence we can have in the precision of \(\hat{\beta}\).

# ols estimates

results.tvalues

Intercept 9.422288

tv 32.808624

radio 21.893496

newspaper -0.176715

dtype: float64

# t = coef / se

np.allclose(

results.tvalues,

results.params / results.bse # <- calculate them by hand

)

True

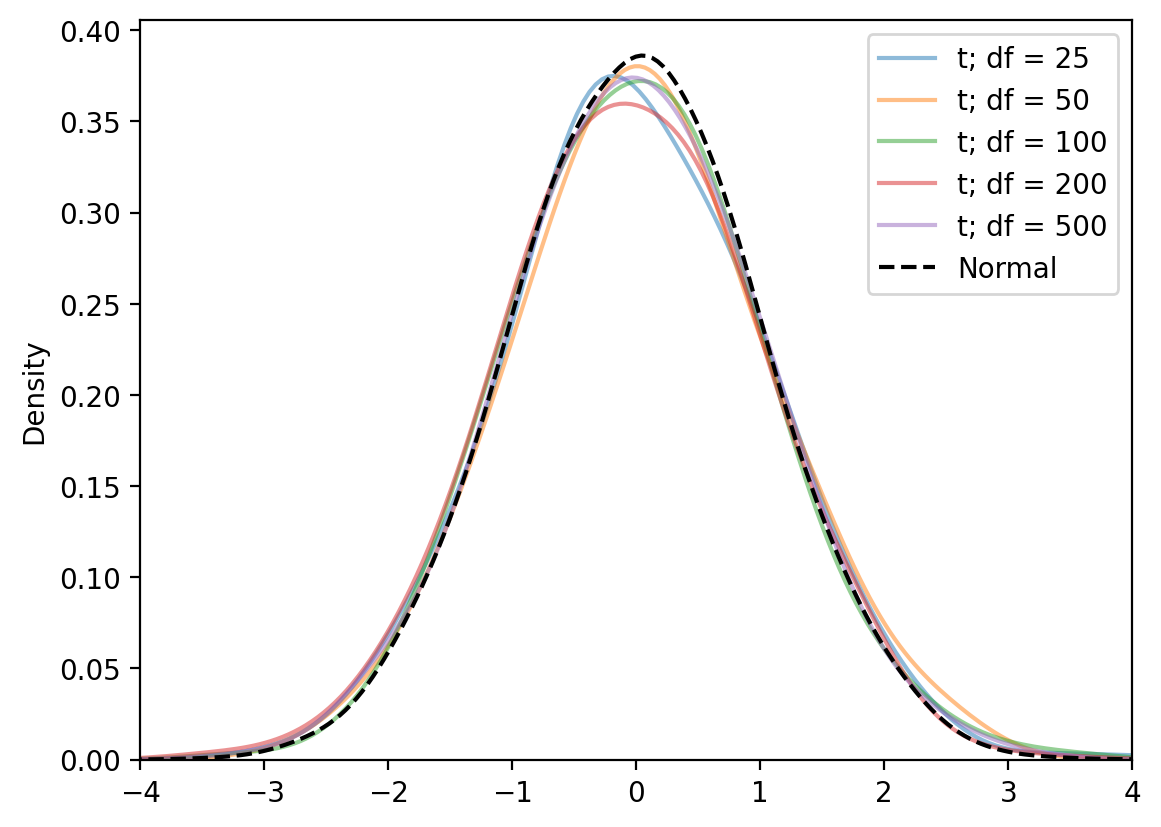

Now if we assume that the sampling distribution of this signal-to-noise-ratio \(t\) looks more and more normal as the size of our sample grows, we can use a t-distribution to look up a p-value.

Intuitively, you can think of a t-distribution as a normal distribution with fatter tails. In technical terms, it carries more probability mass in the extremes relative to a standard normal distribution. As our sample size grows, the degrees of freedom increase, and the tails thin out to look more and more normal - our t-statistic starts to look more like a z-score.

Here’s a figure demonstrating that by increasing the degrees-of-freedom of the t-distribution and comparing it to the normal distribution:

from scipy.stats import t

# Some mock sample sizes

sample_size = [25, 50, 100, 200, 500]

# KDE smoothing

bw_adjust = 1.5

# Loop over sample size and make plots

for sample in sample_size:

data = t.rvs(df=sample,size=1000);

sns.kdeplot(data, label=f"t; df = {sample}", alpha=.5, bw_adjust=bw_adjust);

# Add a normal distribution

ax = sns.kdeplot(np.random.normal(size=10000), label="Normal", alpha=1, color='black', bw_adjust=bw_adjust, ls='--');

# Customization

ax.set_xlim(-4,4)

plt.legend();

With this sampling distribution in hand, we can “look up” our p-value, which allows us to make the following inference:

assuming no true signal exists, how surprised we are to observe this signal-to-noise-ratio, given how many parameters we estimated overall, and the size of our sample?

In Python, we can use the cumulative distribution function of the t-distribution, to look-up the p-value using scipy like we did for the F-test previously:

# Two-sided p-value so use absolute values of t-stats

tstats = np.abs(results.tvalues.to_numpy())

# Remaining df is number of observations - number of parameters

dof = model.df_resid

# Look up the p-values using residual degrees of freedom from the model

pvals = 2 * (1 - t.cdf(tstats, df=dof))

pvals

array([0. , 0. , 0. , 0.85991505])

Which is what ols calculated for us:

np.allclose(

pvals,

results.pvalues.to_numpy()

)

True

Summary of parametric inference#

Parametric inference is the process of using an analytic formula to assume the shape of the sampling distribution and “look-up” a p-value

Our assumptions are only guaranteed to hold true if we have a large enough sample size

This inference process is only valid if we haven’t violated any model assumptions (e.g. no structure in our errors)

If we haven’t violated them, then the signal-to-noise ratio of an estimate \(\frac{\hat{\beta}}{SE_{\hat{\beta}}}\) will follow a t-distribution with \(n-p\) degrees of freedom

If we have, then we should not assume the shape of the sampling distribution - and either respecify our model/data or use non-parametric inference (next section)

To perform parametric inference we:

Estimate parameter \(\hat{\beta}\)

Estimate our uncertainty \(SE_{\hat{\beta}}\)

Calculate our “signal-to-noise ratio” \(t = \hat{\beta} / SE_{\hat{\beta}}\)

Look-up our p-value: assuming no true signal (i.e. \(t=0\)) what is the probability of observing a value as extreme as our \(t\)?

Non-parametric inference using bootstrap resampling#

If that was all a bit confusing or we’re not sure about violating model assumptions we can use bootstrapping to actually compute the sampling dstiributions by resampling-with-replacement from our data!

Having a large enough sample size is still important - but it makes more intuitive sense why:

If we’re building new datasets by resampling-with-replacement from our current dataset, then a smaller dataset has far few combinations of new datasets that we can generate from it! The larger our dataset, the more combinations we have to generate, which will give us a more accurate sense of the (re)-sampling distribtion that we’re building up!

Remember, what we want to know is how much \(\hat{\beta}\) will change, had we collected a different sample. So we’ll generate a new dataset, re-estimate \(\hat{\beta}\), hold on to it, create another bootstrap sample, and repeat the process. Each time \(\hat{\beta}\) will change a little bit. With enough bootstrap sample we can build-up a distribution of this variability - this is our sampling distribution - and the width of it is the uncertainty in our estimate!

Let’s write a function to do this so that we can re-use it in the future. We want our function to take in 3 arguments:

results: the output of callingmodel.fit()when we useolsnboot: the number of bootstraps to runrandom_seed: a number we can use to reproduce our random sampling

In the body of the function we want to implement a for loop logic to do the following:

Resample from

dfwith replacement using the polars.sample()methodFit a new

olsmodel to the resampled data and store it’sparams(betas)Repeat

nboottimesAt the end, use

np.stdandnp.percentileto calculate the width of this distribution and the 95% confidence intervals

Finally we’ll combine all the results into a new Dataframe called boot_results, attach it to the original results object that was input, and return it along with our boostrapped estimates:

def boot_ols(results, nboot=5000, random_seed=0):

# A neat progress bar that replaces range()

from tqdm import trange

params = [] # to store the betas we estimate from each re-sampled dataset

original_params = results.params.to_numpy() # the original betas for reference

# For reproducibility

np.random.seed(random_seed)

# Start bootstrapping

for _ in trange(nboot):

# First generate a new dataset using the original dataframe in the results object

# the .sample() method takes:

# a fraction of the original data - in this case 1.0 aka 100%

# replace - whether to sample with replacement or not

new_data = results.model.data.frame.sample(frac=1., replace=True)

# Fit a new regression using this data and the original model formula

boot_model = ols(results.model.formula, new_data).fit()

# Save the estimated betas

params.append(boot_model.params.to_numpy())

# Convert the list to a numpy array for convenience

params = np.array(params)

# Calculate the width aka the standard-deviation across bootstraps

std_devs = np.std(params, axis=0, ddof=results.df_model)

# Calculate the signal-to-noise aka t-statistic using the bootstrapped SD

tstats = original_params / std_devs

# Get the 95% CI limits using the bootstrapped estimates

CI_limits = np.percentile(params, [2.5, 97.5], axis=0)

# Combine into a DataFrame with original beta estimates

boot_results = pl.DataFrame(CI_limits).transpose().with_columns(

# Predictor names

names = np.array(results.model.exog_names),

# Bootstrapped SDs

se=std_devs,

# T-stats using boostrapped SDs

tstats=tstats,

# Original beta estimates

estimate=original_params

).select(

col('names').alias('variable'),

col('estimate').alias('coef'),

col('se').alias('boot-std'),

col('tstats').alias('t'),

col('column_0').alias('[0.025'),

col('column_1').alias('0.975]'),

)

# Round to 5 decimal places

boot_results = boot_results.select(

col('variable'),

pl.exclude("variable").round(5)

)

# Attach them to the result object that was passed as input

results.boot_summary = boot_results

# Return the results object and the bootstrapped betas

return results, params

Let’s give our function a try by passing in the results from our estimated model

results, boot_betas = boot_ols(results, nboot=1000, random_seed=1)

100%|██████████| 1000/1000 [00:01<00:00, 572.29it/s]

We now have a new .boot_summary attribute that contains a DataFrame with the original estimates in the coef column, and boostrapped standard-deviations which were used to compute the t-statistics and confidence intervals:

results.boot_summary

| variable | coef | boot-std | t | [0.025 | 0.975] |

|---|---|---|---|---|---|

| str | f64 | f64 | f64 | f64 | f64 |

| "Intercept" | 2.93889 | 0.33699 | 8.7209 | 2.25649 | 3.57293 |

| "tv" | 0.04576 | 0.00183 | 24.98447 | 0.04215 | 0.04918 |

| "radio" | 0.18853 | 0.01104 | 17.06964 | 0.16665 | 0.20919 |

| "newspaper" | -0.00104 | 0.00675 | -0.15363 | -0.01366 | 0.01226 |

When we compare this to the analytic standard-error, t-stats, and confidence intervals from the ols model you’ll notice a few things that tend to be true in practice about bootstrapping:

t-stats will be lower

standard errors will be higher

confidence intervals will be wider

# slim=True simplifies the printed output a bit

print(results.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.897

Model: OLS Adj. R-squared: 0.896

No. Observations: 200 F-statistic: 570.3

Covariance Type: nonrobust Prob (F-statistic): 1.58e-96

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 2.9389 0.312 9.422 0.000 2.324 3.554

tv 0.0458 0.001 32.809 0.000 0.043 0.049

radio 0.1885 0.009 21.893 0.000 0.172 0.206

newspaper -0.0010 0.006 -0.177 0.860 -0.013 0.011

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

This is because boostrapping allows us to make fewer assumptions about the underlying shape of the sampling distribution of our parameter estimates - we’re directly generating them.

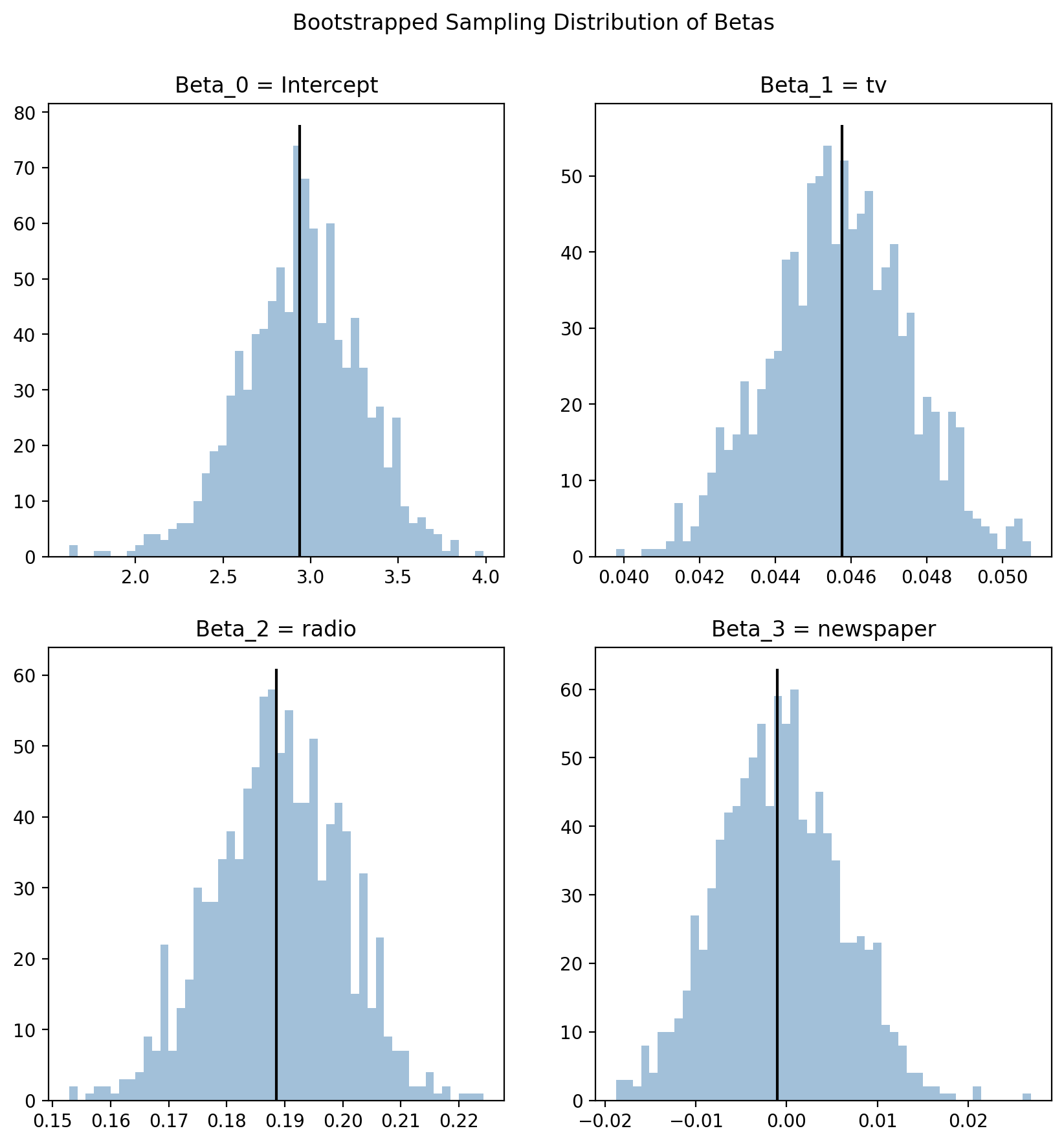

The larger and more normally distributed your your original dataset, the less of a difference you’ll observe between bootstrapped and analytic estimates. Here’s what ours look like from the function we wrote. You’ll notice that the distributions aren’t perfectly symmetrical and have some additional density in the tails.

f, axs =plt.subplots(2,2, figsize=(10,10))

labels = ['Intercept', 'tv', 'radio', 'newspaper']

for i, ax in enumerate(axs.flat):

_ = ax.hist(boot_betas[:,i], bins=50, color='steelblue', alpha=0.5);

_ = ax.set_title(f"Beta_{i} = {labels[i]}");

_ = ax.vlines(results.params.to_numpy()[i], 0, ax.get_ylim()[-1], color='black', linestyle='-');

f.suptitle("Bootstrapped Sampling Distribution of Betas", y=.95);

With these data, boostrapping happens to affords us the same statistical inference as the analytic approach.

For example, if we look at the predictor \(newspaper\), we see that the value \(0\) sits within the resampled distribution of estimate for \(\hat{\beta}_{newspaper}\).

And in the summary tables above, the 95% confidence intervals contain this value.

This leads us to the same inference as analytic p-value:

Factoring in the uncertainty of our estimate - the value \(0\) is not that surprising an estimate for \(\hat{\beta}_{newspaper}\) - “not statistically significant”

Non-parametric inference using permutation (shuffling)#

In addition to the uncertainty of our estimates we have one more tool to perform statistical inference: we can also use resampling to build up a null distribution.

Remember what a p-value fundamentally represents: the probability of observing our estimate like ours assuming the null hypothesis is true.

So just like we replaced our assumption about the shape of a sampling distribution with bootstrapping, we can replace our assumption about the shape of a null distribution with permutation

Let’s write another function to do this so that we can re-use it in the future. We want our function to take in 3 arguments:

results: the output of callingmodel.fit()when we useolsnperm: the number of times to shuffle the datasetrandom_seed: a number we can use to reproduce our shuffling

In the body of the function we want to implement a for loop logic to do the following:

Shuffle the rows of our dependent variable column in

dfusing the polars.sample()method which breaks its relationship to the independent variablesFit a new

olsmodel to the shuffled data and store it’stvaluesRepeat

npermtimesCalculate how often the permuted t-values were greater than our original t-value

def perm_ols(results, nperm=5000, random_seed=0):

# A neat progress bar that replaces range()

from tqdm import trange

perm_ts = [] # to store the t-stats we estimate from each shuffled dataset

original_ts = results.tvalues.to_numpy() # the original ts for reference

dv_name = results.model.endog_names # name of y variable

# For reproducibility

np.random.seed(random_seed)

for _ in trange(nperm):

# Generate new dataset by shuffling rows in the DV column only

# and use .alias to deliberately *overwrite* the DV column

new_data = df.with_columns(

df[dv_name].sample(fraction=1.,with_replacement=False,shuffle=True)

.alias(dv_name)

)

# Fit model to it

pmodel = ols(results.model.formula, data=new_data.to_pandas())

presults = pmodel.fit()

# Save the t-stats

perm_ts.append(presults.tvalues.to_numpy())

perm_ts = np.array(perm_ts)

# Get the # of permuted t-stats >= observed t-stat

proportion = np.sum(

np.abs(perm_ts) >= np.abs(original_ts),

axis=0) + 1

# Divide by number of permutation to get p-value

# Add 1 to numerator and denominator to avoid divide-by-zero errors

pvals = proportion / (nperm + 1)

# Make a polars DataFrame

pvals = pl.DataFrame(dict(zip(results.model.exog_names, pvals)))

# Shuffling the data doesn't permute the intercept so ignore the p-value

pvals[0, 'Intercept'] = np.nan

# Return pvals and permuted t-stats

return pvals, perm_ts

And trying it out we can see our permuted p-values are very similar to the analytic p-values from ols:

pvals, perm_ts = perm_ols(results, nperm=1000, random_seed=1)

100%|██████████| 1000/1000 [00:01<00:00, 523.23it/s]

pvals

| Intercept | tv | radio | newspaper |

|---|---|---|---|

| f64 | f64 | f64 | f64 |

| NaN | 0.000999 | 0.000999 | 0.861139 |

# From ols

results.pvalues.round(5)

Intercept 0.00000

tv 0.00000

radio 0.00000

newspaper 0.85992

dtype: float64

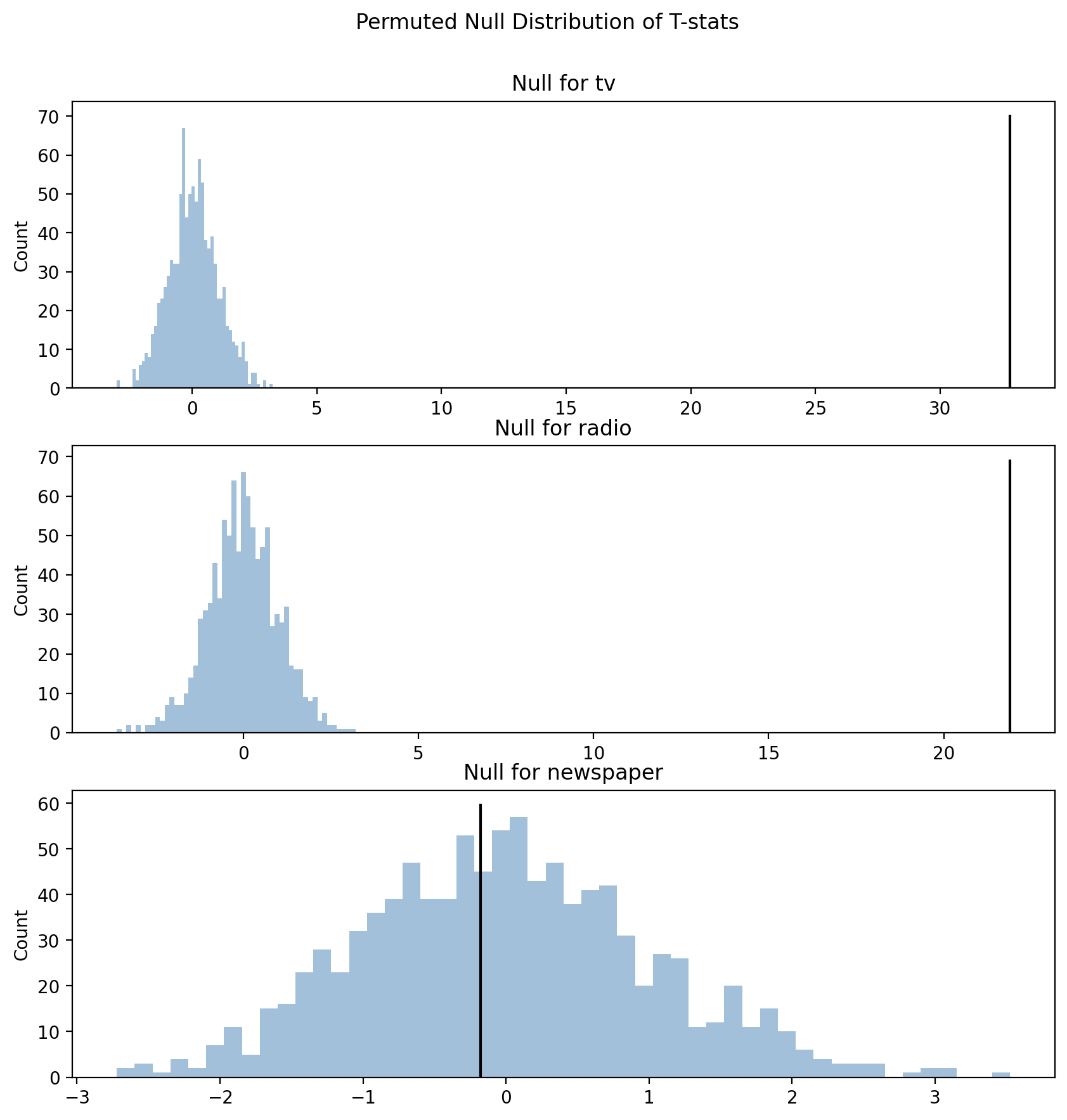

And we can visualize our null distributions which show us what t-statistics we would expect under the assumption that there is no relationship between our \(y\) (\(sales\)) and our \(X\) (\(tv\), \(radio\), \(newspaper\)) variables.

We simulated this assumption by randomizing our data via shuffling (permutation).

f, axs =plt.subplots(3,1, figsize=(10,10), sharey=False, sharex=False)

labels = ['tv', 'radio', 'newspaper']

for i, ax in enumerate(axs.flat):

_ = ax.hist(perm_ts[:,i+1], bins=50, color='steelblue', alpha=0.5);

_ = ax.set_title(f"Null for {labels[i]}");

_ = ax.set_ylabel("Count");

_ = ax.vlines(results.tvalues.to_numpy()[i+1], 0, ax.get_ylim()[-1], color='black', linestyle='-');

f.suptitle("Permuted Null Distribution of T-stats", y=.95);

It’s very clear from these plots why \(newspaper\) (bottom) is not “statistically significant” -

the signal-to-noise ratio \(t\) is well-within the range of values we would expect assuming our data were random!

Summary of non-parametric inference via permutation#

Permutation allows us to build null distributions to perform statistical inference on our parameter estimates

Based on how we choose randomize we can simulate the specific form of randomization that we what to make an inference about

In the example above we preserved the relationship between the predictors, by only permuting the response variable

To perform a permutation test with a GLM we can:

Fit our model and calculate our inferential statistic - the one we want a p-value for \(t\)

Shuffle our response variable \(y\) and re-estimate our model using the shuffled data

Repeat this process with more randomizations

Calculate the proportion of times the permuted versions of our inferential statistic \(t\) are greater-than-or-equal-to our observed value \(t\) on the original data

Challenge Q (response)#

What do you think would happen if you instead shuffled a column of one of the predictor variables?

Your response here

General summary of Non-Parametric Inference#

With these two approach to resampling we can make fewer assumptions about the structure of our model’s errors and just calculate them directly from our data. The biggest trade-off to these approaches is that they are more “expensive” to calculate - but when possible - especially with complicated datasets - they often yield more robust and verifiable inferences; when in doubt - just inspect the resampling or null distributions you created!

Regardless of whether you use parametric or non-parametric inference it’s important to understand why statistical signficance IS NOT practical or scientific significance.

The standard-error and ultimately the t-stat and p-value reflect a combination of the following:

size of the \(\beta\)

how bad the model is overall

the sample size

the variance of the \(Xn\) that \(\beta\) corresponds to

and the correlation of \(Xn\) with all other columns in \(X\)

To paraphrase from one of the assigned readings, The Truth About Linear Regression:

This means that the standard errors will shrink as the sample size grows, so more and more variables will become significant as we get more data — but how much data we collect is irrelevant to how the process we’re studying actually works! Moreover, at a fixed sample size, the coefficients with smaller standard errors will tend to be the ones whose variables have more variance, and whose variables are less correlated with the other predictors. High input variance and low correlation help us estimate the coefficient precisely, but, again, they have nothing to do with whether the input variable actually influences the response a lot!

To sum up, it is never the case that statistical significance is the same as scientific, real-world significance. The most important variables are not those with the largest-magnitude t statistics or smallest p-values. Statistical significance is always about what “signals” can be picked out clearly from background noise. In the case of linear regression coefficients, statistical significance runs together the size of the coefficients, how bad the linear regression model is, the sample size, the variance in the input variable, and the correlation of that variable with all the others. Of course, even the limited “does it help linear predictions enough to bother with?” utility of the usual t-test (and F-test) calculations goes away if the standard distributional assumptions do not hold, so that the calculated p-values are just wrong. But one can sometimes get away with using bootstrapping (Chapter 6) to get accurate p-values for standard tests under non-standard conditions

Paul Meehl noted the same dilemma if we use parametric inference as our only tool to perform Null-Hypothesis-Significance-Testing (NHST):

In the limit of an infinitely large sample size, we have the least uncertainty (highest precision) to estimate a parameter. But counter-intuitively, that means that any non-zero estimate, no matter how small will appear “statistically significant” from 0 even if it’s not practically meaningful!

Wrap-up#

Let’s wrap-up by writing a convenience function that “wraps” the 2 functions we wrote above. This will make it make this even easier to use we can tweak it so it feels like a drop-in replacement for ols:

We’ll copy the definitions of our 2 function above inside the body of our new function and add a little bit of code to combine the outputs:

def ols_nonparam(formula, data, nsim=1000, random_seed=None, return_dists=False):

"""

Non-parametric version of statsmodels OLS regression.

Is equivalent to the output of ols(formula).fit() - in other words only returns

the results not the model itself. The results also includes a .summary_resampled

attribute that contains the bootstrapped and permuted results.

Args:

formula (str): formula to fit model

data (DataFrame): pandas or polars DataFrame

nsim (int, optional): number of bootstraps and permutations to run. Defaults to 1000.

random_seed (int, optional): for reproducibility. Defaults to None.

return_dists (bool, optional): whether to return the bootstrapped and permuted results. Defaults to False.

Returns:

results: statsmodels OLS regression results

"""

from statsmodels.formula.api import ols

# Create and fit the original model on the original data

model = ols(formula, data)

results = model.fit()

# Define bootstrap function

def boot_ols(results, nboot, random_seed):

# A neat progress bar that replaces range()

from tqdm import trange

params = [] # to store the betas we estimate from each re-sampled dataset

original_params = results.params.to_numpy() # the original betas for reference

# For reproducibility

np.random.seed(random_seed)

# Start bootstrapping

for _ in trange(nboot):

# Resample with replacement - using pandas here instead of polars

new_data = results.model.data.frame.sample(frac=1., replace=True)

# Fit a new regression using this data and the original model formula

boot_model = ols(results.model.formula, new_data).fit()

# Save the estimated betas

params.append(boot_model.params.to_numpy())

# Convert the list to a numpy array for convenience

params = np.array(params)

# Calculate the width aka the standard-deviation across bootstraps

std_devs = np.std(params, axis=0, ddof=results.df_model)

# Calculate the signal-to-noise aka t-statistic using the bootstrapped SD

tstats = original_params / std_devs

# Get the 95% CI limits using the bootstrapped estimates

CI_limits = np.percentile(params, [2.5, 97.5], axis=0)

# Combine into a DataFrame with original beta estimates

boot_results = pl.DataFrame(CI_limits).transpose().with_columns(

# Predictor names

names = np.array(results.model.exog_names),

# Bootstrapped SDs

se=std_devs,

# T-stats using boostrapped SDs

tstats=tstats,

# Original beta estimates

estimate=original_params

).select(

col('names').alias('variable'),

col('estimate').alias('coef'),

col('se').alias('boot-std'),

col('tstats').alias('t'),

col('column_0').alias('[0.025'),

col('column_1').alias('0.975]'),

)

# Round to 5 decimal places

boot_results = boot_results.select(

col('variable'),

pl.exclude("variable").round(5)

)

return boot_results, params

# Define permutation function

def perm_ols(results, nperm, random_seed):

# A neat progress bar that replaces range()

from tqdm import trange

perm_ts = [] # to store the t-stats we estimate from each shuffled dataset

original_ts = results.tvalues.to_numpy() # the original ts for reference

dv_name = results.model.endog_names # name of y variable

# For reproducibility

np.random.seed(random_seed)

for _ in trange(nperm):

# Convert to polars for easier shuffling

new_data = pl.DataFrame(data)

new_data = new_data.with_columns(

new_data[dv_name].sample(fraction=1.,with_replacement=False,shuffle=True)

.alias(dv_name)

)

# Fit model to it; and convert back to pandas

pmodel = ols(results.model.formula, data=new_data.to_pandas())

presults = pmodel.fit()

# Save the t-stats

perm_ts.append(presults.tvalues.to_numpy())

perm_ts = np.array(perm_ts)

# Get the # of permuted t-stats >= observed t-stat

proportion = np.sum(

np.abs(perm_ts) >= np.abs(original_ts),

axis=0) + 1

# Divide by number of permutation to get p-value

# Add 1 to numerator and denominator to avoid divide-by-zero errors

pvals = proportion / (nperm + 1)

# Make a polars DataFrame

pvals = pl.DataFrame(dict(zip(results.model.exog_names, pvals)))

# Shuffling the data doesn't permute the intercept so ignore the p-value

pvals[0, 'Intercept'] = np.nan

# Return pvals and permuted t-stats

return pvals, perm_ts

# Run boostrapping and permuting

boot_results, boot_betas = boot_ols(results, nsim, random_seed)

pvals, perm_ts = perm_ols(results, nsim, random_seed)

# Combine bootstrapped and permutation estimates into 1 DataFrame

full_results = boot_results.with_columns(

perm_p = pvals.to_numpy().flatten()

)

# Reorder columns to match ols output

full_results = full_results.select(

col('variable'),

col('coef'),

col('boot-std'),

col('t'),

col('perm_p').alias('P_perm>|t|'),

col('[0.025'),

col('0.975]')

)

# Attach to results object from ols

results.summary_resampled = full_results

# Return distributions of boostraps and permutation if requested

if return_dists:

return results, boot_betas, perm_ts

else:

return results

Let’s try our function out! We can check-out the help we wrote:

ols_nonparam?

Signature:

ols_nonparam(

formula,

data,

nsim=1000,

random_seed=None,

return_dists=False,

)

Docstring:

Non-parametric version of statsmodels OLS regression.

Is equivalent to the output of ols(formula).fit() - in other words only returns

the results not the model itself. The results also includes a .summary_resampled

attribute that contains the bootstrapped and permuted results.

Args:

formula (str): formula to fit model

data (DataFrame): pandas or polars DataFrame

nsim (int, optional): number of bootstraps and permutations to run. Defaults to 1000.

random_seed (int, optional): for reproducibility. Defaults to None.

return_dists (bool, optional): whether to return the bootstrapped and permuted results. Defaults to False.

Returns:

results: statsmodels OLS regression results

File: /var/folders/4y/y26_jdm57m90f4s1td24ls040000gn/T/ipykernel_33472/992760803.py

Type: function

And run it on our data:

results = ols_nonparam("sales ~ tv + radio + newspaper", data=df.to_pandas(), nsim=1000, random_seed=1)

100%|██████████| 1000/1000 [00:01<00:00, 577.77it/s]

100%|██████████| 1000/1000 [00:01<00:00, 531.94it/s]

We can access the non-parametric results via the .summary_resampled attribute of the output:

results.summary_resampled

| variable | coef | boot-std | t | P_perm>|t| | [0.025 | 0.975] |

|---|---|---|---|---|---|---|

| str | f64 | f64 | f64 | f64 | f64 | f64 |

| "Intercept" | 2.93889 | 0.33699 | 8.7209 | NaN | 2.25649 | 3.57293 |

| "tv" | 0.04576 | 0.00183 | 24.98447 | 0.000999 | 0.04215 | 0.04918 |

| "radio" | 0.18853 | 0.01104 | 17.06964 | 0.000999 | 0.16665 | 0.20919 |

| "newspaper" | -0.00104 | 0.00675 | -0.15363 | 0.87013 | -0.01366 | 0.01226 |

And compare them to the parametric results that ols calculates for us:

results.summary(slim=True)

| Dep. Variable: | sales | R-squared: | 0.897 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.896 |

| No. Observations: | 200 | F-statistic: | 570.3 |

| Covariance Type: | nonrobust | Prob (F-statistic): | 1.58e-96 |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 2.9389 | 0.312 | 9.422 | 0.000 | 2.324 | 3.554 |

| tv | 0.0458 | 0.001 | 32.809 | 0.000 | 0.043 | 0.049 |

| radio | 0.1885 | 0.009 | 21.893 | 0.000 | 0.172 | 0.206 |

| newspaper | -0.0010 | 0.006 | -0.177 | 0.860 | -0.013 | 0.011 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Now we have a quick way to checkout our non-parametric estimates alongside our parametric ones! For future assignments we’ll try to include this function in a file that you can import. But it might be handy to refer to this notebook if you ever need to write it again.

Challege: Non-Parametric Inference#

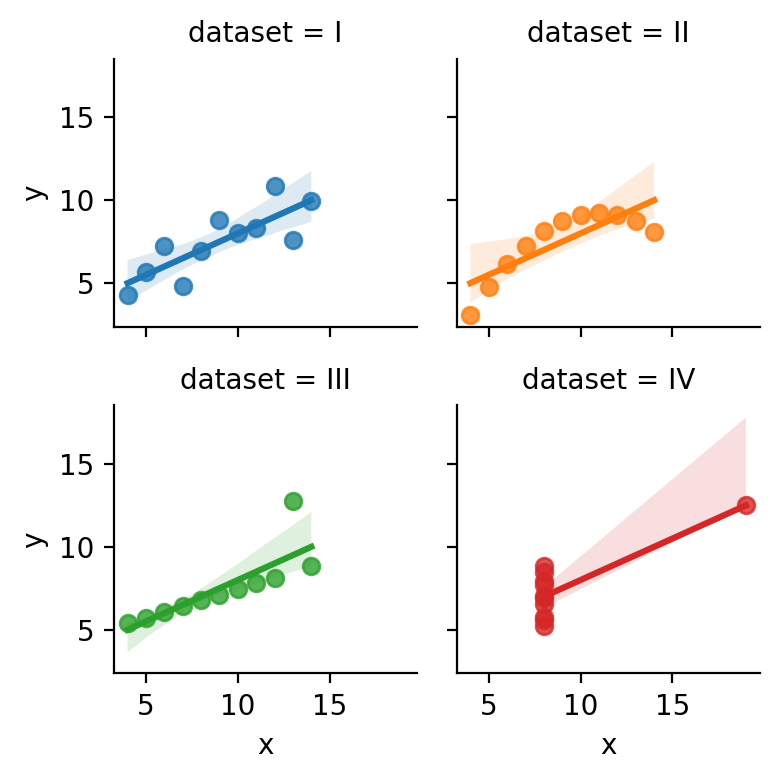

Below we’ve loaded up Anscombe’s Quartet again and plotted a simple univariate regression using sns.lmplot, which uses ols behind-the-scenes.

When you run the cell you’ll see the regression line for each dataset and 95% bootstrapped confidence intervals that seaborn automatically computed for us.

# Load and convert to polars

anscombe = pl.DataFrame(sns.load_dataset("anscombe"))

# Plot the regression for each dataset separately

sns.lmplot(x="x", y="y", data=anscombe, hue="dataset", col='dataset', col_wrap=2, height=2)

<seaborn.axisgrid.FacetGrid at 0x16c8af8d0>

Looking at each sub-plot above, it seems like the the “worst” fit is with dataset IV.

In every other dataset there seems to be some type of relationship between x and y - but in dataset IV this seems to be driven by a single observation.

Your task is to fit a univariate regression to dataset IV only using the new ols_nonparam function we wrote.

You’ll have to use .filter() to subset the rows in anscombe that you want.

For ols_nonparam you can use:

nsim=2000random_seed=1return_dists=True

# Solution

data_4 = anscombe.filter(col("dataset") == "IV")

# Solution

results, boots, perms = ols_nonparam('y ~ x', data=data_4.to_pandas(), nsim=2000,random_seed=1, return_dists=True)

100%|██████████| 2000/2000 [00:02<00:00, 846.91it/s]

100%|██████████| 2000/2000 [00:03<00:00, 617.38it/s]

Inspect the differences in the outputs of .summary_resampled and .summary()

What do you notice?

# Solution

results.summary_resampled

results.summary(slim=True)

| variable | coef | boot-std | t | P_perm>|t| | [0.025 | 0.975] |

|---|---|---|---|---|---|---|

| str | f64 | f64 | f64 | f64 | f64 | f64 |

| "Intercept" | 3.00173 | 1.48395 | 2.02279 | NaN | 0.10001 | 4.12477 |

| "x" | 0.49991 | 0.17794 | 2.80946 | 0.064468 | 0.4408 | 0.92688 |

/Users/esh/miniconda3/envs/201b/lib/python3.11/site-packages/scipy/stats/_axis_nan_policy.py:418: UserWarning: `kurtosistest` p-value may be inaccurate with fewer than 20 observations; only n=11 observations were given.

return hypotest_fun_in(*args, **kwds)

| Dep. Variable: | y | R-squared: | 0.667 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.630 |

| No. Observations: | 11 | F-statistic: | 18.00 |

| Covariance Type: | nonrobust | Prob (F-statistic): | 0.00216 |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 3.0017 | 1.124 | 2.671 | 0.026 | 0.459 | 5.544 |

| x | 0.4999 | 0.118 | 4.243 | 0.002 | 0.233 | 0.766 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

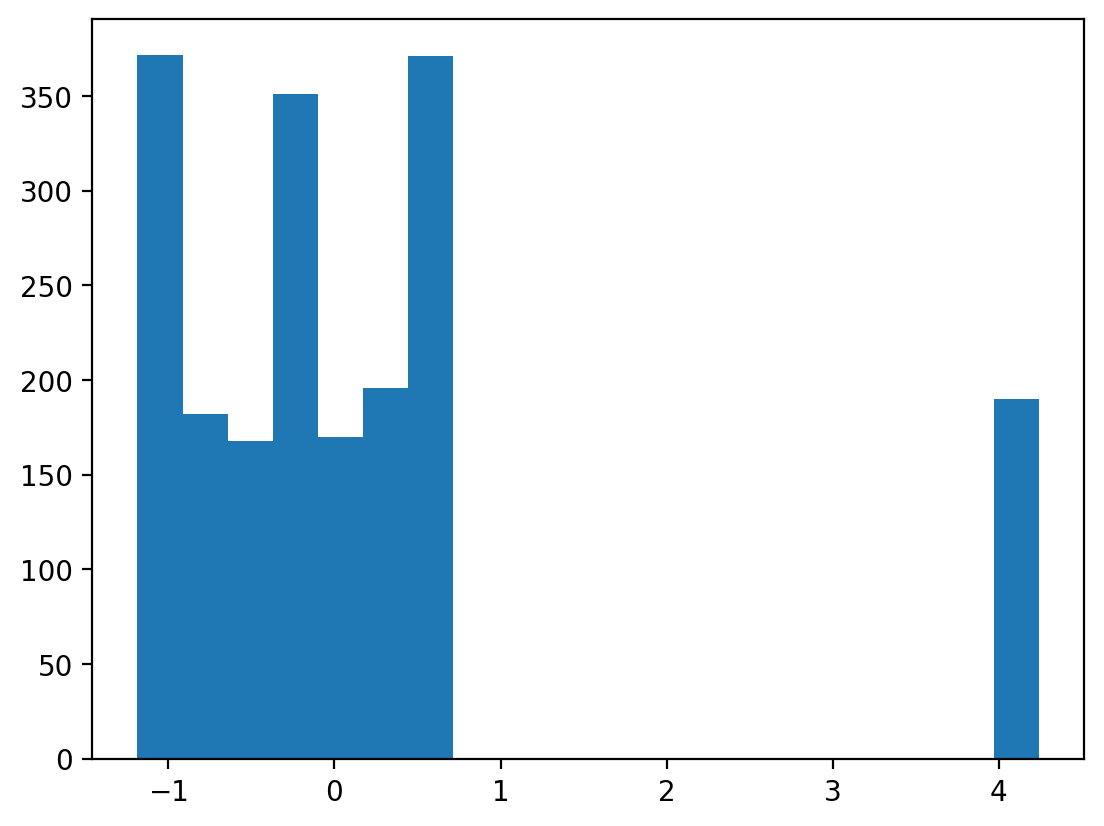

Inspect perms using a histogram.

You can use perms = perm[:, 1] before plotting to only plot the permuted values for x and ignore the model intercept

What do you notice? How does this affect the permuted p-value vs the analytic p-value in the outputs above?

# Solution

# Ignore intercept

perms = perms[:, 1]

plt.hist(perms, bins=20)

(array([372., 182., 168., 351., 170., 196., 371., 0., 0., 0., 0.,

0., 0., 0., 0., 0., 0., 0., 0., 190.]),

array([-1.18601317, -0.9145611 , -0.64310903, -0.37165696, -0.1002049 ,

0.17124717, 0.44269924, 0.71415131, 0.98560337, 1.25705544,

1.52850751, 1.79995958, 2.07141165, 2.34286371, 2.61431578,

2.88576785, 3.15721992, 3.42867199, 3.70012405, 3.97157612,

4.24302819]),

<BarContainer object of 20 artists>)