Models VI: Interactions and Multicollinearity#

Revisiting the Advertising dataset#

At the end of the last notebook we provided you with a challenge using the advertising dataset.

Specifically we asked you to fit a model that included an interaction between tv and radio and then explore the correlations between predictors with and without centering.

Let’s take a further look here:

Variable |

Description |

|---|---|

tv |

TV ad spending in $1000 of dollars |

radio |

Radio ad spending in $1000 of dollars |

newspaper |

Newspaper ad spending in $1000 of dollars |

sales |

Sales generated in $1000 of dollars |

We’ll load up the data

import numpy as np

import polars as pl

from polars import col

import seaborn as sns

import matplotlib.pyplot as plt

from statsmodels.formula.api import ols

from helpers import plot_predictor_correlations

df = pl.read_csv('./data/advertising.csv')

df.head()

| tv | radio | newspaper | sales |

|---|---|---|---|

| f64 | f64 | f64 | f64 |

| 230.1 | 37.8 | 69.2 | 22.1 |

| 44.5 | 39.3 | 45.1 | 10.4 |

| 17.2 | 45.9 | 69.3 | 9.3 |

| 151.5 | 41.3 | 58.5 | 18.5 |

| 180.8 | 10.8 | 58.4 | 12.9 |

And then fit 2 models with the same parameters:

One without centering our predictors

One with centering our predictors

# Uncentered

model = ols('sales ~ tv * radio', data=df.to_pandas())

results = model.fit()

# Centered

model_centered = ols('sales ~ center(tv) * center(radio)', data=df.to_pandas())

results_centered = model_centered.fit()

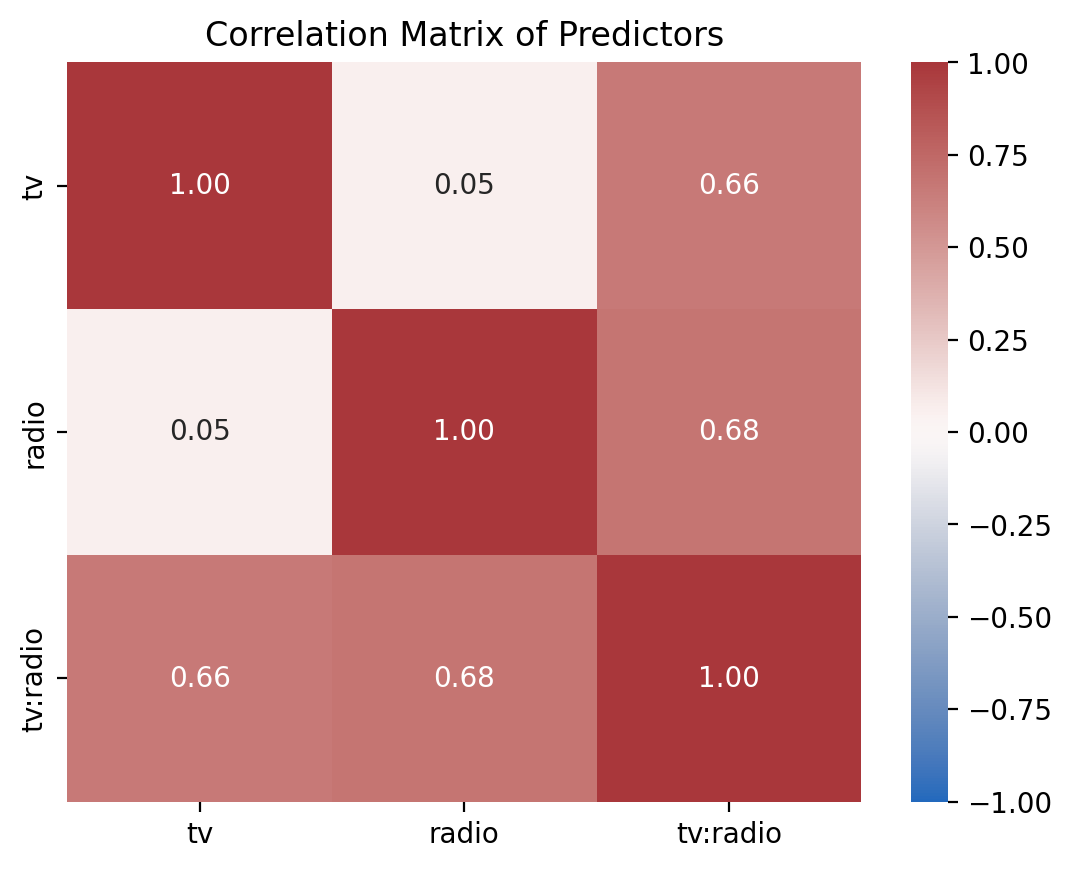

Let’s look at the correlations between the predictors in each model. The helper function we provided you plot_predictor_correlations will do this by looking at the correlations between the columns of each model’s design matrix \(X\)

When we look at the uncentered model we see that the interaction term tv:radio is highly correlated with both tv and radio - this makes sense - the product of 2 continuous variables is going to increase/decrease if either of the variables increase/decrease.

plot_predictor_correlations(model)

<Axes: title={'center': 'Correlation Matrix of Predictors'}>

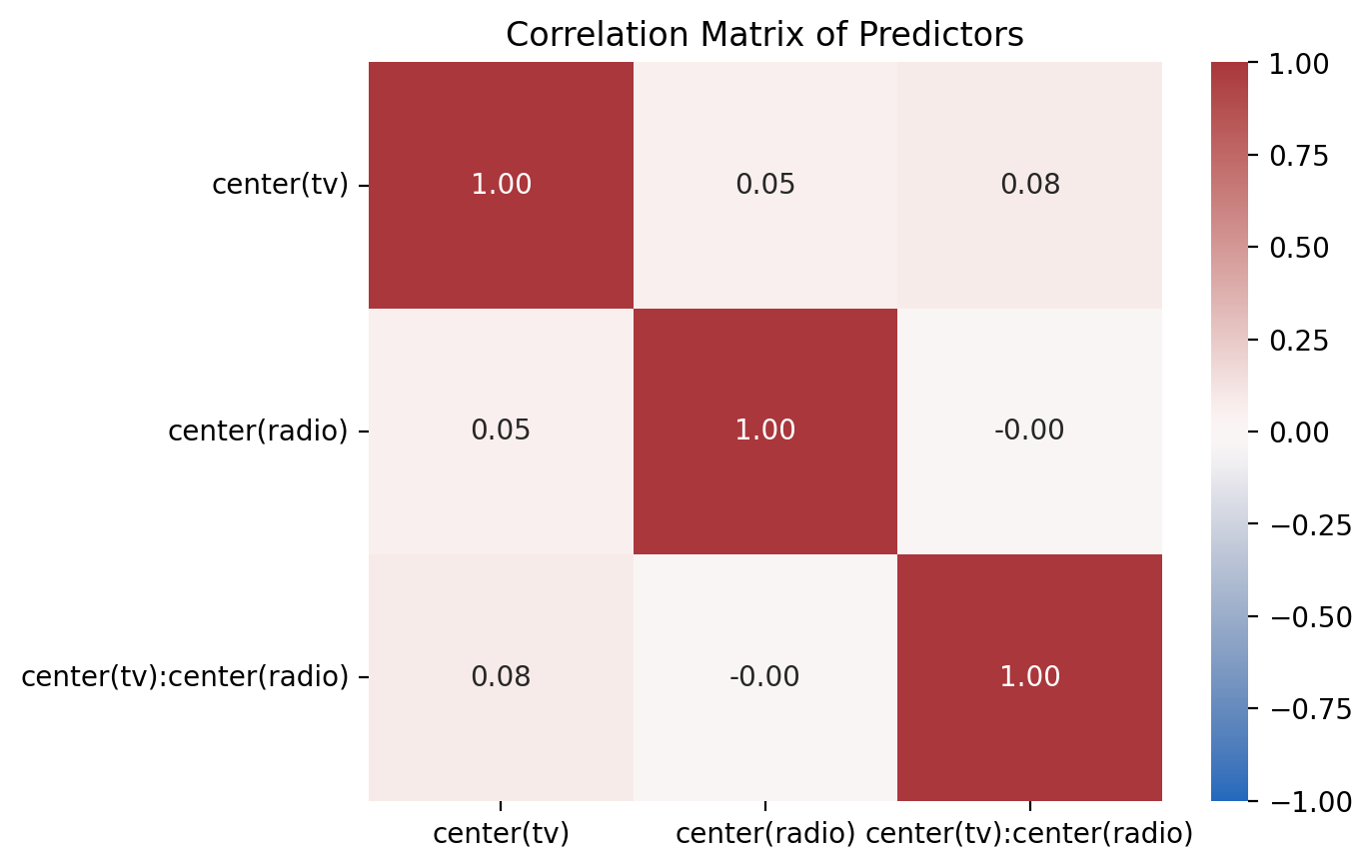

But when we look at the uncentered model we see that the correlations have now been reduced!

plot_predictor_correlations(model_centered)

<Axes: title={'center': 'Correlation Matrix of Predictors'}>

Let’s try to understand why this matters by revisiting one of the assumptions of the GLM we haven’t discussed yet: multicollinearity.

Multicollinearity - the other assumption#

Previously we discussed the fundamental assumptions of GLMs that can be summarized as independent & iidentically distributed errors (iid):

errors should be independent of each other

errors should be independent of predictors

errors should be approximately normal

Now let’s explore multicollinearity - a situation in which the predictors of a GLM are correlated with each other. How correlated? There isn’t actually a principled answer for this because it depends on the goals of your analysis!

Instead in this notebook we’ll explore the key points you should understand about this assumption:

Why it matters

How it affects parameter estimates

How it affects estimate uncertainty (standard-errors & confidence intervals)

How to check for it

How to deal with it

We’ll also ask you to skim the following paper which provides a more detailed discussion of what (and what not to) worry about when it comes to multicollinearity:

Vanhove, J. (2021). Collinearity isn’t a disease that needs curing. Meta-Psychology, 5.

Why it matters#

Intuitively, collinearity matters because in the worst case, when 2 or more predictors are perfectly correlated, we can’t tell the difference between how much 2 or more variables uniquely predict \(y\)!

In the figures above, the overlap in circles shows how much \(X1\) and \(X2\) predict \(y\) and how much overlap (corelation) exists between \(X1\) and \(X2\). In the right most figure, we see that \(X1\) and \(X2\) are so overlapping that it doesn’t even make sense to use both of them in the same model!

In linear algebra terms:

If any of the predictors in \(X\) is a perfect linear combination of the other predictors, we say that \(X\) is rank-deficient - it doesn’t need as many columns as it has to reflect the overall variance that it does

In this case, there is no unique solution for \(\hat{\beta}\), because the matrix \( (X^TX)^{-1} \) is not invertible.

Let’s see this with some 3d plots of a multiple regression with 2 predictors X1 and X2

Remember that graphically, fitting a multiple regression with 2 predictors is extending the idea of a line of best fit to a plane or sheet of best fit.

In this first movie X1 and X2 are uncorrelated and we can see that the regression plane is stable across repeated samples

In the second, the two predictors are correlated. The regression plane tips on a ridge defined by the correlated predictors, and is unstable across repeated samples:

Key Takeaways#

In general we want to avoid multi-collinearity because it makes it harder to identify the unique contribution of each predictor in our GLM. Concretely we’ll see this reflected in our calculations in the following ways:

Our parameter estimates can become very large and even flip sign from negative to positive

Our uncertainty in those estimates becomes larger so our standard errors always increase

As a result our confidence intervals become wider

So our statistical power decreases - we’re less certain of our estimates so our ability to make reliable conclusions given the same sample size decreases

Our overall model fit does not change - in other words our error in predicting our dependent variable does not increase as a result of collinearity - but our model does get less interpretable - we can’t pinpoint the unique contribution of each predictor!

You can see this reflected in the following figure just plotting the estimates and 95% confidence intervals for two predictors with varying levels of collinearity:

Inspecting collinearity: VIF#

We already saw one way of checking for collinearity: visual inspection of predictor correlations

We can also generalize this idea to calculate what’s called a variance inflation factor (VIF) for each predictor in our model:

where \(R^2_{(-k)}\) refers to \(R\)-squared value you would get if you ran a regression using \(X_k\) as the outcome variable, and all the other \(X\) variables as the predictors. The idea here is that \(R^2_{(-k)}\) is a very good measure of the extent to which \(X_k\) is correlated with all the other variables in the model. Better yet, the square root of the VIF is pretty interpretable: it tells you how much wider the confidence interval for the corresponding coefficient \(b_k\) is, relative to what you would have expected if the predictors are all nice and uncorrelated with one another. If you’ve only got two predictors, the VIF values are always going to be the same.

To calculate VIF we can use the variance_inflation_factor() function from statsmodels. However, this function only calculated VIF for a single predictor, so we’ll write our own function (we’ve also provided it in helpers.py which you can import using: from helpers import vif) to calculate the VIFs for all of our predictors at once. We’ll also return the square-root of the VIF to get a sense of how much wider our CIs would be:

# Import statsmodels function

from statsmodels.stats.outliers_influence import variance_inflation_factor

# Just showing you the code here

# For future just do:

# from helpers import vif

def vif(model):

"""Calculate VIFs for all predictors in a model"""

vifs = []

for i in range(model.exog.shape[1]):

this_vif = variance_inflation_factor(model.exog,i)

vifs.append(this_vif)

return pl.DataFrame({

'variable': model.exog_names,

'VIF': vifs,

'CI_increase': np.sqrt(vifs)

})

Let’s use this to calculate the VIFs for our uncentered and centered models:

# Uncentered

vif(model)

| variable | VIF | CI_increase |

|---|---|---|

| str | f64 | f64 |

| "Intercept" | 13.803357 | 3.715287 |

| "tv" | 3.727848 | 1.930764 |

| "radio" | 3.907651 | 1.976778 |

| "tv:radio" | 6.93786 | 2.633982 |

vif(model_centered)

| variable | VIF | CI_increase |

|---|---|---|

| str | f64 | f64 |

| "Intercept" | 1.002983 | 1.00149 |

| "center(tv)" | 1.010291 | 1.005132 |

| "center(radio)" | 1.003058 | 1.001528 |

| "center(tv):center(radio)" | 1.007261 | 1.003624 |

VIF rule-of-thumb#

So how should we interpret these? A decent rule-of-thumb is to be concerned about VIFs that are 5 or greater - but this is not a hard-and-fast rule.

Why 5? Because it means our estimates are going to be 2.5x as uncertain as they would have been with no collinearity. Is 2.5x the right number? It depends on how much certainty you need in your specific estimates and what kind of statistical inference you want to make.

We can see that when we don’t center our predictors - the widths of our confidence intervals are larger by a factor of about np.sqrt(VIF) for each predictor relative to our centered predictors:

# Uncentered CIs

results.conf_int()

| 0 | 1 | |

|---|---|---|

| Intercept | 6.261383 | 7.239058 |

| tv | 0.016135 | 0.022067 |

| radio | 0.011298 | 0.046423 |

| tv:radio | 0.000983 | 0.001190 |

# Uncentered widths

widths = results.conf_int()[1] - results.conf_int()[0]

widths

Intercept 0.977675

tv 0.005933

radio 0.035125

tv:radio 0.000207

dtype: float64

# Centered CIs

results_centered.conf_int()

| 0 | 1 | |

|---|---|---|

| Intercept | 13.815204 | 14.078745 |

| center(tv) | 0.042833 | 0.045922 |

| center(radio) | 0.179723 | 0.197519 |

| center(tv):center(radio) | 0.000983 | 0.001190 |

# Centered Widths

widths_centered = results_centered.conf_int()[1] - results_centered.conf_int()[0]

widths_centered

Intercept 0.263541

center(tv) 0.003089

center(radio) 0.017796

center(tv):center(radio) 0.000207

dtype: float64

# These look as wide as our uncentered predictors' CIs!

# Centered widths * sqrt(VIF)

widths_centered * vif(model).select('CI_increase').to_numpy().flatten()

Intercept 0.979132

center(tv) 0.005963

center(radio) 0.035179

center(tv):center(radio) 0.000545

dtype: float64

Handling multi-collinearity#

Aside from visual inspection or VIF calculations the most direct way you can handle multi-collinearity is to simply removing one or more variables from your model that are redundant with other variables!

A few other approaches we won’t cover in details in this course:

Creating new un-correlated predictors using Principal Components Analysis (PCA)

Adding regularization to OLS via Ridge Regression which will force the model to keep \(\beta\) values small

Adding regularization to OLS via Lasso Regression which will force the model to set some of the \(\beta\) values to zero

If the collinearity is because of interactions between variables that you’ve created - you can center or z-score each variable before calculating the interaction like we’ve seen before.

Let’s explore this with a challenge:

Challenge#

Fit and explore a new model like the ones above (including an interaction) but this time z-score each predictor in the model:

Create new z-scored columns for

tvandradioin your DataFrame and fit a new model using those columns those witholsFit a second model using the

standardize()transformation in the model formula itself with the original columns; see how we usedcenter()above - is there any difference?Then use

plot_predictor_correlationsto visualize the correlations between predictors from either model. How does this compare to the uncentered and centered models?In notebook

04_modelsin the “Gram Matrix” section we created a histogram of 3 predictors. Recreate the histogram for the original and z-scored columns. How are they different?Inspect the parameter estimate from the z-scored model. How would you interpret these compared to the centered model?

1) Create new z-scored columns and use them to fit a new model#

# Your code here

# Solution

zscore = lambda name: (col(name) - col(name).mean()) / col(name).std()

df = df.with_columns(

tv_z = zscore('tv'),

radio_z = zscore('radio'),

)

model_z = ols('sales ~ tv_z * radio_z', data=df.to_pandas())

results_z = model_z.fit()

2) Fit another model using the original columns and standardize() in the formula#

Is there any difference?

# Your code here

# Solution

model_z_formula = ols('sales ~ standardize(tv) * standardize(radio)', data=df.to_pandas())

results_z_formula = model_z_formula.fit()

results_z.params

Intercept 13.946974

tv_z 3.809978

radio_z 2.800424

tv_z:radio_z 1.384913

dtype: float64

results_z_formula.params

Intercept 13.946974

standardize(tv) 3.800441

standardize(radio) 2.793414

standardize(tv):standardize(radio) 1.377988

dtype: float64

3) Use plot_predictor_correlations to compare correlations between either z-scored model and the centered and uncentered models#

# Your code here

# Solution

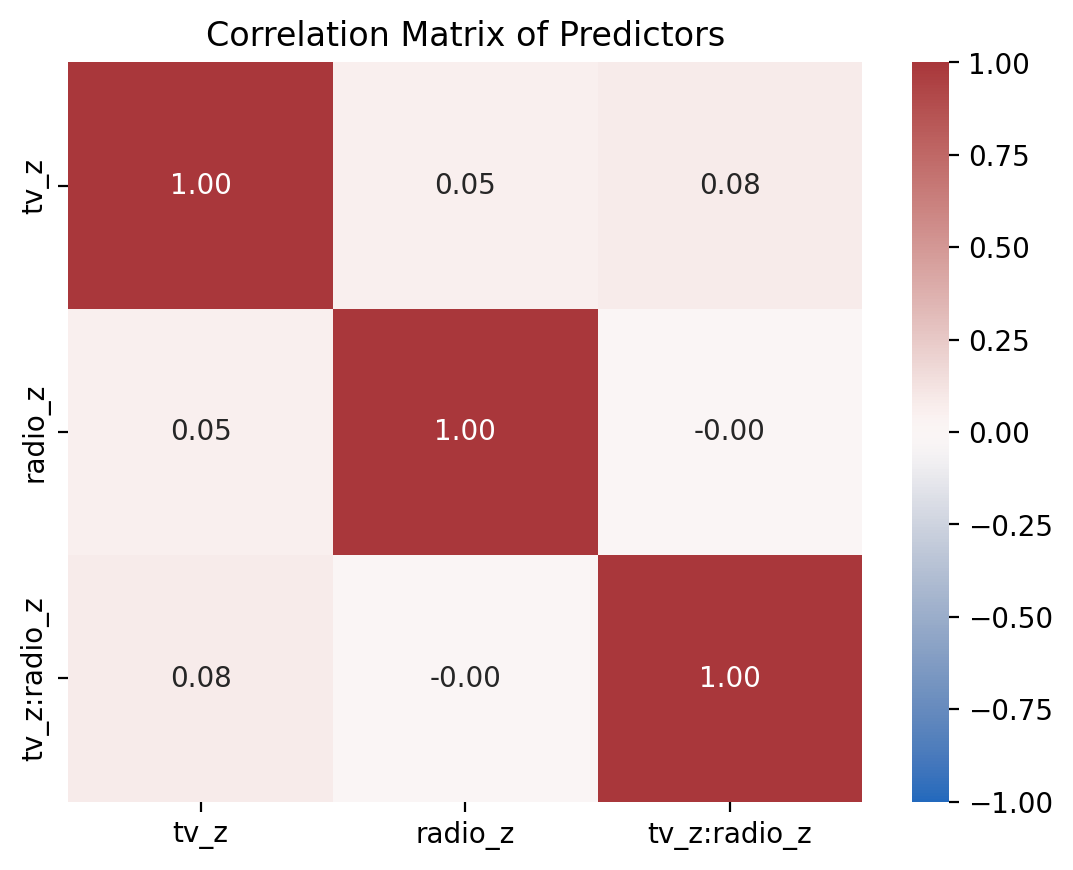

plot_predictor_correlations(model_z)

<Axes: title={'center': 'Correlation Matrix of Predictors'}>

# Solution

plot_predictor_correlations(model_centered)

<Axes: title={'center': 'Correlation Matrix of Predictors'}>

# Solution

plot_predictor_correlations(model)

<Axes: title={'center': 'Correlation Matrix of Predictors'}>

How are they different?

Your response here

4) Create a histogram of the z-scored predictors and compare it to a histogram of the original predictors#

We’ve given you starter code below…

# Plot from 04_models using raw data

ax=sns.histplot(data=df, x='tv', kde=False, label='TV')

ax=sns.histplot(data=df, x='radio', kde=False, label='Radio')

ax.legend();

# Your code here

# Solution

ax=sns.histplot(data=df, x='tv_z', kde=False, label='TV')

ax=sns.histplot(data=df, x='radio_z', kde=False, label='Radio')

ax.legend();

How are they different?

Your response here

5) Compare parameter estimates from z-scored and centered models#

# Your code here

# Solution

print(results_centered.summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.968

Model: OLS Adj. R-squared: 0.967

No. Observations: 200 F-statistic: 1963.

Covariance Type: nonrobust Prob (F-statistic): 6.68e-146

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

Intercept 13.9470 0.067 208.737 0.000 13.815 14.079

center(tv) 0.0444 0.001 56.673 0.000 0.043 0.046

center(radio) 0.1886 0.005 41.806 0.000 0.180 0.198

center(tv):center(radio) 0.0011 5.24e-05 20.727 0.000 0.001 0.001

============================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.28e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

# Solution

print(model_scaled.fit().summary(slim=True))

OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.968

Model: OLS Adj. R-squared: 0.967

No. Observations: 200 F-statistic: 1963.

Covariance Type: nonrobust Prob (F-statistic): 6.68e-146

======================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------------

Intercept 13.9470 0.067 208.737 0.000 13.815 14.079

standardize(tv) 3.8004 0.067 56.673 0.000 3.668 3.933

standardize(radio) 2.7934 0.067 41.806 0.000 2.662 2.925

standardize(tv):standardize(radio) 1.3780 0.066 20.727 0.000 1.247 1.509

======================================================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

How would you interpret them in natural language?

Your response here